UAE Corporate Tax Losses Explained: Carry Forward Rules, Relief & Founder Planning Guide

By Filing Buddy . 10 Feb 26

1.png)

Why UAE Corporate Tax Losses Matter to Founders

Not every business year ends in profit, and for founders, that is completely normal. Startups often incur losses while investing in growth, building teams, and entering new markets. Even mature businesses can face temporary downturns due to economic conditions, seasonal demand, or capital-heavy expansion. Losses are not always a red flag; in many cases, they are part of a long-term growth strategy.

The UAE Corporate Tax system acknowledges this reality. Instead of taxing businesses in isolation year by year, it takes a broader view of profitability over time. Companies are allowed to carry forward losses and use them to reduce tax liability in future profitable years. This is where tax loss relief becomes valuable, not just as a safety net, but as a planning tool. For founders, understanding how tax losses work early can help protect cash flow, smooth future tax costs, and support sustainable business growth.

What Is a Corporate Tax Loss Under UAE Law?

A corporate tax loss arises when a business’s allowable expenses are higher than the income that is subject to corporate tax in a particular year. Simply put, if your business spends more than it earns (for tax purposes), it records a tax loss for that period.

It’s important not to confuse a tax loss with an accounting loss. Your financial statements may show a loss, but corporate tax follows its own rules. Some expenses that appear in your books may not be deductible for tax, and some types of income may be fully exempt from corporate tax.

Because of this, adjustments are required before a tax loss is calculated. Income that is exempt must be excluded, and non-deductible expenses such as fines, penalties, or personal costs added to business accounts must be removed. Only after these adjustments do you arrive at the final tax loss figure. This adjusted loss is what the UAE Corporate Tax law allows businesses to carry forward and use to reduce taxable income in future profitable years.

What Is Tax Loss Relief Under UAE Corporate Tax?

Tax loss relief is a provision under Article 37 of the UAE Corporate Tax Law that allows businesses to use losses from one year to reduce taxable profits in future years. Instead of losing the benefit of an unprofitable year, companies can carry those losses forward and apply them when the business becomes profitable.

The purpose of tax loss relief is simple:

- To ensure businesses are taxed on overall profitability, not just individual good years

- To support startups and growing companies that invest heavily in their early stages

- To prevent sudden tax pressure when profits return after a loss-making period

This approach reflects international tax best practices followed in many mature economies. Businesses are given the opportunity to recover from difficult periods without being unfairly taxed later.

At its core, tax loss relief is a fairness mechanism. It recognises that business growth is rarely linear and ensures that companies are not penalised for temporary setbacks while remaining fully compliant with the UAE Corporate Tax framework.

When Tax Loss Relief Is NOT Allowed?

While UAE Corporate Tax allows businesses to carry forward losses, not all losses qualify for tax loss relief. Knowing these exclusions upfront helps founders avoid mistakes and incorrect tax planning.

Tax loss relief is not allowed in the following situations:

- Losses incurred before the implementation of UAE Corporate Tax

Any losses generated before the corporate tax regime came into effect cannot be carried forward. - Losses incurred before becoming a taxable person

Losses from periods when the business was not subject to corporate tax are excluded. - Losses linked to exempt income or exempt assets

If the income is not taxable, the related losses cannot be used for relief. - Losses during Small Business Relief periods

Losses incurred while claiming Small Business Relief cannot be carried forward.

These restrictions exist to maintain fairness and consistency in the tax system. Understanding them early reduces compliance risks and builds confidence in your tax planning decisions.

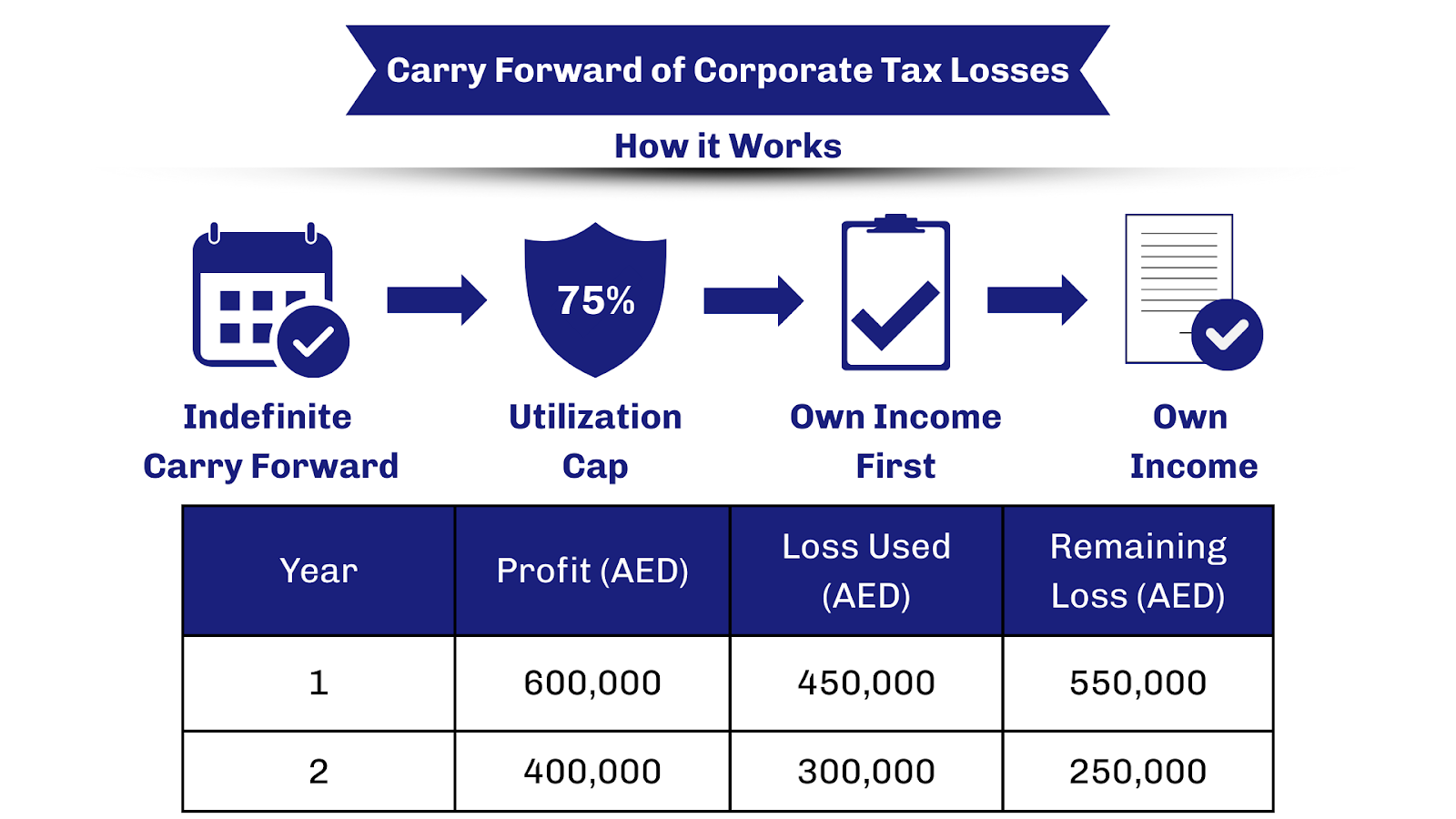

Carry Forward of Corporate Tax Losses: How It Works

One of the most valuable aspects of UAE Corporate Tax is the indefinite carry forward of tax losses. This means a loss in Year 1 can be applied against profits in Year 5 or beyond, subject to certain conditions.

There is a 75% utilization cap, which ensures companies still pay tax on a portion of their profits while benefiting from previous losses. Utilization follows a mandatory order: losses are applied first against the company’s own taxable income before any other adjustments or group considerations.

Example:

- Year 1: Company A has a tax loss of AED 1,000,000.

- Year 2: Company A makes a taxable profit of AED 600,000.

- Applying the 75% cap, the company can offset 75% of its profit (AED 450,000) using the loss.

- Remaining profit of AED 150,000 is taxed normally, and the leftover loss (AED 550,000) carries forward.

This mechanism ensures founders can balance growth and tax efficiency, smoothing the financial peaks and troughs inherent in scaling businesses.

Ownership Continuity Rule: What Founders Must Watch Out For

A critical rule for founders is the 50% ownership continuity requirement. To claim tax loss relief, the same individuals (or group) must retain at least 50% ownership of the company.

This prevents “buying losses,” where an investor might acquire a loss-making company purely to offset profits elsewhere. If ownership changes exceed the threshold, tax authorities may disallow loss claims for that year and beyond.

Example:

Imagine Founder A owns 60% of Company X and carries forward AED 500,000 in losses. If Founder A sells 30% of their stake to a new investor, ownership continuity drops below 50%, and part or all of the carried-forward losses could be invalidated.

Founders must plan equity changes carefully, especially when raising venture capital or transferring shares, to preserve the value of accumulated losses.

Business Continuity Requirement Explained Simply

Alongside ownership, the company must continue the same or a similar business to utilize carried-forward losses. Minor evolution is acceptable, like expanding a product line or moving into complementary services, but a complete pivot can disqualify loss claims.

Examples of acceptable changes:

- Adding a digital sales channel to an existing retail business

- Introducing new but related products or services

Disqualifying changes:

- Changing from a software company to a restaurant

- Switching industries entirely

The intent is simple: tax relief is designed for companies that are genuinely continuing their business, not those repurposing losses for unrelated ventures.

Special Treatment for Listed Companies

Listed companies receive slightly different rules. Certain restrictions under Article 39, like ownership continuity tests, may not apply to publicly traded entities. This acknowledges that public shareholding changes constantly, and the standard rules would be impractical.

The principle remains: listed companies can still carry forward losses, but reporting and disclosure obligations are stricter to maintain transparency.

Transfer of Tax Losses Between Group Companies

Article 38 allows tax losses to be transferred within corporate groups, provided conditions are met. This is particularly useful for holding companies or conglomerates with multiple subsidiaries.

Key requirements include:

- 75% common ownership between the entities

- Both companies must be resident or juridical persons under UAE law

- Accounting years must align, and accounting standards should be consistent

- Losses can only offset profits in the same group year, respecting the 75% utilization cap

This mechanism enables larger groups to optimize taxes, allocate resources efficiently, and support subsidiaries strategically, without violating compliance requirements.

Example: How Group Loss Transfer Works in Practice

Scenario:

- Company A: Loss of AED 800,000

- Company B: Profit of AED 600,000

- Companies share 75% common ownership

Step-by-step:

- Apply 75% cap: Company B can offset 75% of its profit (AED 450,000) using Company A’s loss.

- Company B pays tax on the remaining AED 150,000.

- Remaining loss from Company A: AED 350,000 carries forward for future use.

Table:

| Company | Profit/Loss | Offset | Taxable Income | Remaining Loss |

| A | -800,000 | -450,000 | 0 | 350,000 |

| B | 600,000 | 450,000 | 150,000 | 0 |

This shows how group-level planning maximizes tax efficiency while staying fully compliant.

What Income Cannot Be Reduced Using Tax Losses

Not all income qualifies for loss offsets. Founders must be cautious about:

- Exempt income: Certain foreign-sourced or specified investments

- Personal or non-business income: Income unrelated to corporate operations

- Non-deductible expenses: Penalties, fines, or non-business-related costs

- Penalties and fines: Cannot be offset against losses

Awareness of these limitations helps founders avoid compliance issues and ensures that carried-forward losses are applied correctly.

Documentation & Compliance: What the FTA Expects

The Federal Tax Authority (FTA) requires meticulous documentation to validate tax loss claims. Founders should maintain:

- Financial statements aligned with accounting standards

- Tax adjustments showing non-deductible items and exemptions

- Working papers that clearly justify calculations

- Audit-readiness mindset: everything should be defensible in case of review

Proper documentation isn’t just a legal requirement, it’s a tool to prevent disputes and protect the company’s financial credibility, ensuring founders can rely on losses for future planning.

Common Founder Mistakes That Lead to Rejected Tax Loss Claims

Some mistakes repeatedly trip up founders:

- Forgetting to declare losses: Always report even if there’s no immediate benefit

- Poor documentation: Missing invoices, adjustments, or reconciliations

- Ignoring ownership changes: Share transfers above the 50% threshold can invalidate losses

- Confusing accounting vs tax losses: Not all accounting losses are tax-deductible

Avoiding these errors saves time, preserves credibility, and ensures the company fully benefits from carried-forward losses.

Why Tax Loss Relief Is a Strategic Tool, Not Just a Benefit

Beyond compliance, tax loss relief is a strategic lever for founders:

- Cash flow smoothing: Offsets profits and reduces sudden tax burdens

- Growth-stage planning: Encourages reinvestment in expansion, R&D, and hiring

- Investor confidence: Transparent planning and predictable tax impact attract funding

- Group-level optimization: Consolidated planning across subsidiaries enhances efficiency

Viewing tax loss relief as a strategic tool shifts mindset from reactive compliance to proactive business planning.

How Founders Can Stay Fully Compliant While Maximizing Tax Losses

Founders can maximize benefits while staying compliant by:

- Proactive tax planning: Forecast profits and losses to optimize carry-forward usage

- Ongoing compliance: Keep records updated and reconcile adjustments regularly

- Advisory support: Consult tax experts for complex ownership or group structures

- Long-term savings mindset: Treat tax loss management as a multi-year strategy, not a one-time exercise

Following these principles ensures losses contribute to growth rather than creating legal or financial risks.

Conclusion: Turning Losses Into Long-Term Tax Efficiency

Losses are a natural part of business growth, not a reason to panic. UAE Corporate Tax offers founders a framework to turn setbacks into strategic advantages through carry-forward provisions, group planning, and careful compliance.

Key takeaways:

- Track losses accurately, distinguishing accounting from tax losses

- Maintain ownership and business continuity to preserve relief

- Document thoroughly to satisfy the FTA

- Leverage losses strategically to smooth cash flow and attract investment

By adopting a compliance-first mindset, founders can convert temporary setbacks into long-term financial efficiency, turning tax losses into a core part of growth planning.

Contact Us

An expert will call you within 24 hours. No payment required to get started.

Related Post

.png)

Navigating UAE VAT Compliance

Explore the key changes in UAE VAT compliance for 2024, their implications for businesses, and practical steps to ensure adherence under the latest regulations for seamless tax management.

. 5 min read.png)

UAE Corporate Tax Deadline September 30, 2025 – Filing Buddy Compliance Guide

Stay compliant with UAE corporate tax. Learn who must file, key deadlines, penalties, and how Filing Buddy ensures 100% corporate tax compliance before the September 30, 2025 deadline.

. 3 min read

UAE Scrap Metal VAT Reverse Charge Guide 2026

Learn how the UAE’s scrap metal Reverse Charge Mechanism impacts VAT, compliance, and refunds. Stay compliant and prepare your business today..

3 min