UAE Small Business Relief Under Corporate Tax: Eligibility, Rules, Examples & Strategic Considerations

By Filing Buddy . 13 Feb 26

1.png)

UAE Corporate Tax & Small Business Relief

The UAE Corporate Tax regime applies to tax periods starting on or after 1 June 2023. Under this system, Businesses are required to pay 9% Corporate Tax on taxable income exceeding AED 375,000.

To support smaller businesses during this transition, the government introduced Small Business Relief (SBR). This relief is designed to reduce both the tax burden and the compliance workload for eligible SMEs. If a business qualifies and elects for SBR, it may be treated as having no taxable income for that period, meaning no Corporate Tax is payable.

The relief is available for tax periods ending on or before 31 December 2026, giving businesses a limited window to benefit from it.

However, it’s important to note that Small Business Relief is not automatic. Businesses must register for Corporate Tax and actively choose this relief in their tax return after evaluating whether it suits their long-term strategy.

What is Small Business Relief (SBR)?

Small Business Relief (SBR) is a special provision under the UAE Corporate Tax regime that supports small and medium-sized businesses during the early years of tax implementation.

If a business qualifies and elects for SBR, it is treated as having no taxable income for that specific tax period.

What does this mean in practical terms?

- No Corporate Tax payable for that period

- No requirement to calculate taxable income

- Simplified tax compliance and reporting

However, it’s important to understand one key point:

SBR is relief from tax calculation and payment, not relief from registration or filing.

Businesses must still:

- Register for Corporate Tax

- Obtain a Tax Registration Number (TRN)

- File a Corporate Tax return and formally elect for SBR

In short, SBR reduces tax burden and compliance complexity — but it does not remove your obligation to stay registered and compliant with the Federal Tax Authority (FTA).

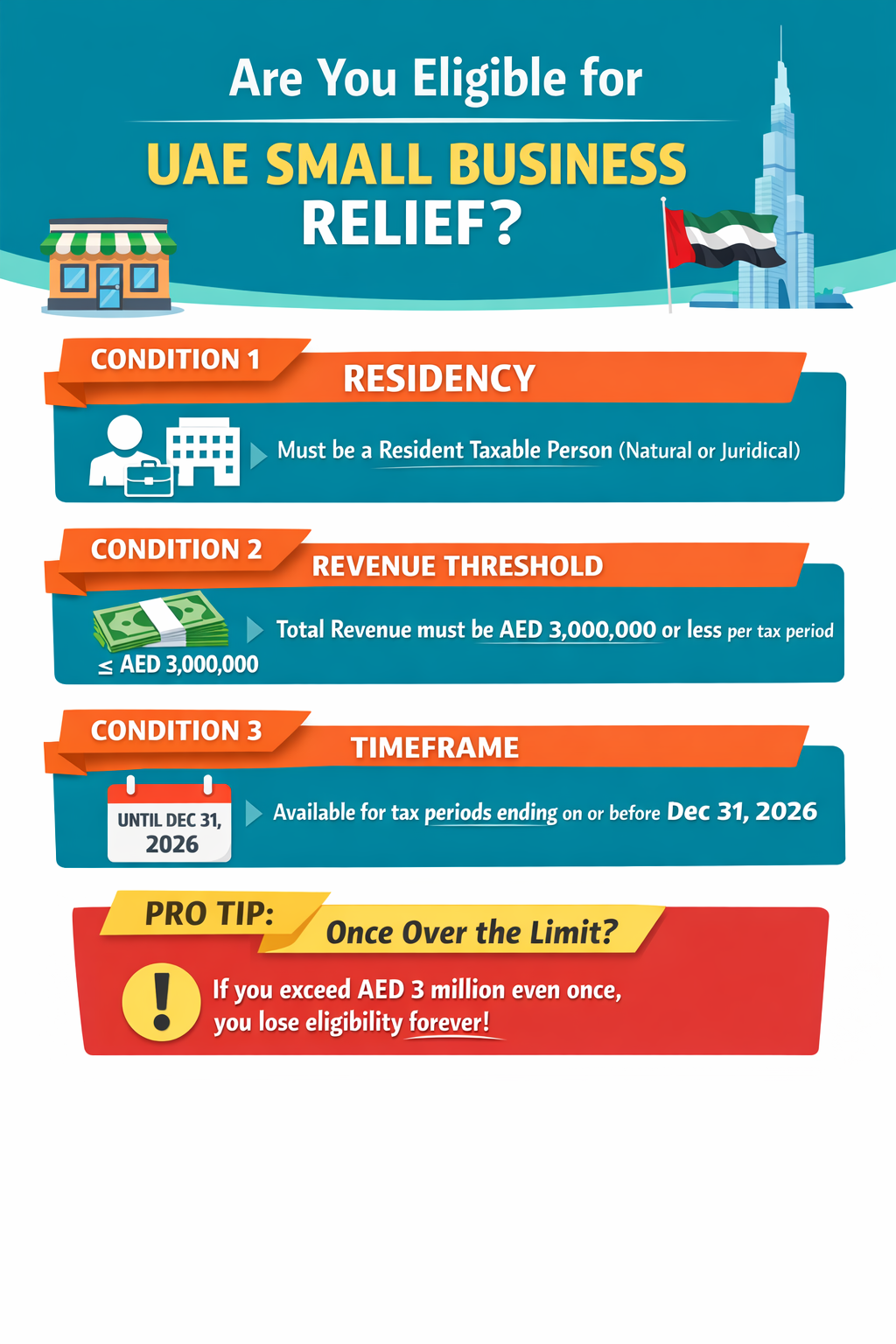

Who is Eligible for Small Business Relief?

To benefit from Small Business Relief (SBR) under UAE Corporate Tax, a business must meet specific eligibility criteria set by the Federal Tax Authority (FTA).

Basic Eligibility Conditions

1. Must Be a Resident Taxable Person

The relief is available only to UAE resident taxable persons, including:

- Natural Persons – Individual business owners conducting business in the UAE

- Juridical Persons – Legal entities such as LLCs and other registered companies

2. Revenue Must Not Exceed AED 3,000,000

The business’s total revenue must be AED 3,000,000 or less:

- For the current tax period, and

- For all previous tax periods

If revenue exceeds AED 3 million in any one period, the business becomes permanently ineligible for SBR in future years.

3. Time Limitation

Small Business Relief is available only for tax periods ending on or before 31 December 2026.

Meeting these conditions does not automatically grant relief — businesses must still formally elect for SBR in their Corporate Tax return.

Special Rule for Natural Persons

For individual business owners (Natural Persons), Corporate Tax does not apply automatically. There is a separate threshold that determines whether they fall within the Corporate Tax regime.

When Does Corporate Tax Apply?

Corporate Tax applies to a Natural Person only if:

- Their annual business turnover exceeds AED 1,000,000 in a Gregorian calendar year.

If turnover is below AED 1,000,000, Corporate Tax does not apply at all.

When Can a Natural Person Claim SBR?

Small Business Relief (SBR) becomes relevant if turnover is:

- Above AED 1,000,000, and

- Not exceeding AED 3,000,000

In this range, the individual may register for Corporate Tax and elect for SBR, provided all other conditions are satisfied.

What Is Not Considered Business Income?

The following types of income are excluded from business turnover:

- Salary or employment income

- Personal investment income

- Real estate investment income (unless conducted as a licensed business activity)

This distinction is important when calculating eligibility under the SBR revenue threshold.

Revenue vs Profit – Critical Clarification

Many businesses assume eligibility is based on profit. This is incorrect.

- Revenue = Gross income earned

- Profit = Revenue – Expenses

The AED 3 million threshold is based strictly on revenue, not profit. Even if your business makes little or no profit, exceeding the revenue cap affects eligibility.

What Is Included in Revenue?

The following must be counted toward the AED 3M limit:

- Sales income

- Service income

- Proceeds from selling business assets (e.g., equipment, property)

- Non-cash or barter transactions (valued at market price)

- Dividends and other income that form part of the business’s gross revenue (where applicable)

What Is Excluded?

- VAT collected from customers (as it is payable to the government)

The “Once You Cross, You’re Out” Rule

If your revenue exceeds AED 3 million in any single tax period:

- The business will no longer be eligible to elect Small Business Relief for subsequent tax periods.

- Even if revenue falls below AED 3 million in future years

This rule is particularly critical for fast-growing or asset-selling businesses planning expansion.

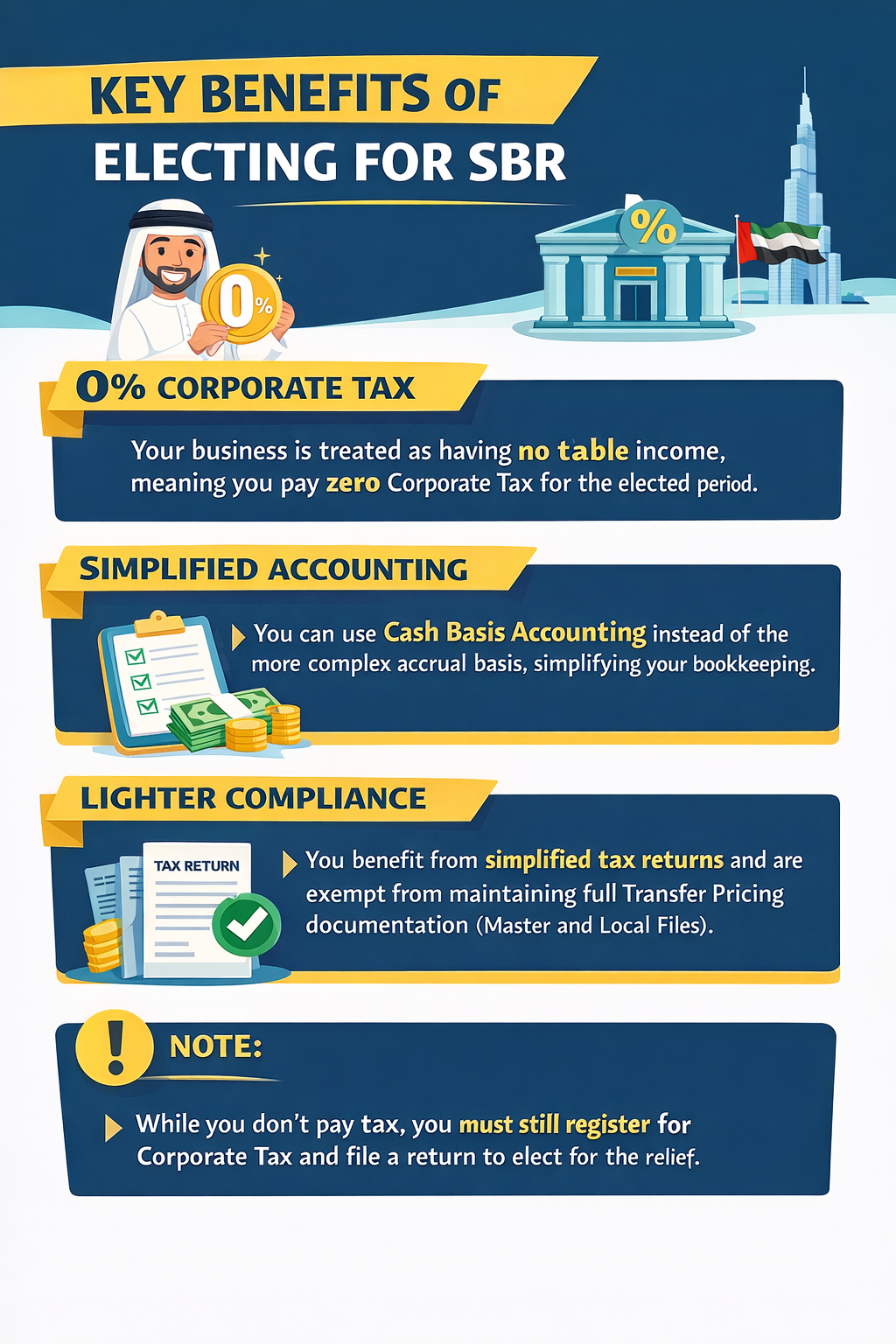

Key Benefits of Small Business Relief (SBR)

Electing for Small Business Relief provides both financial and administrative advantages for eligible businesses.

Zero Corporate Tax

- No 9% Corporate Tax payable for the elected tax period

- Business is treated as having no taxable income

This allows small businesses to preserve cash flow and reinvest in operations or growth.

Simplified Accounting

- Eligible businesses can use the cash basis of accounting

- No requirement to follow the more complex accrual basis

This reduces bookkeeping complexity and makes compliance easier for SMEs.

Reduced Transfer Pricing Requirements

- No requirement to maintain full transfer pricing documentation (Master File and Local File)

- However, transactions must still comply with the Arm’s Length Principle

In short, documentation is lighter — but pricing must still be commercially justified.

Simplified Tax Return

- Corporate Tax registration is still mandatory

- A Tax Return must still be filed

- Reporting requirements are simplified compared to standard Corporate Tax filings

Small Business Relief reduces compliance burden — but it does not eliminate filing obligations.

Who Is Not Eligible for Small Business Relief?

Even if your revenue is below AED 3 million, certain businesses cannot claim Small Business Relief.

Multinational Enterprise Groups (MNEs)

If your business is part of a multinational group with consolidated global revenue exceeding AED 3.15 billion, you are not eligible.

This rule ensures that large international groups cannot access relief designed specifically for small and medium enterprises.

Qualifying Free Zone Persons

Businesses that qualify for the 0% Corporate Tax rate on qualifying income in Free Zones are excluded from SBR.

Since they already benefit from a preferential tax regime, they cannot opt for Small Business Relief.

Artificially Separated Businesses

If the Federal Tax Authority (FTA) determines that a business has been split into multiple entities purely to keep revenue under the AED 3 million threshold, relief will be denied.

The FTA examines:

- Financial links

Economic links

Organisational links

If separation lacks a genuine commercial purpose, it may be treated as artificial fragmentation, making the entities ineligible for SBR.

Artificial Separation – Detailed Explanation

The Federal Tax Authority (FTA) closely monitors whether businesses have been deliberately split into multiple entities to remain under the AED 3 million revenue threshold. This is known as artificial separation, and if identified, Small Business Relief (SBR) can be denied.

The FTA does not rely solely on the legal structure of the entities. Instead, it examines whether the businesses are genuinely independent in substance.

Financial Links

The FTA evaluates whether one entity financially supports or depends on another.

Red flags may include:

- One company regularly funding the expenses of another

- Inter-company loans without commercial justification

- One entity not being financially viable on its own

If a business cannot realistically operate independently, the FTA may consider it artificially separated.

Economic Links

Here, the FTA examines whether the businesses are economically connected.

Indicators include:

- Serving the same group of customers

- One entity’s activity directly supporting or relying on another

- Operations that only make sense when combined

For example, splitting a single business activity into “sales” and “operations” companies that function as one unit may raise concerns.

Organisational Links

This focuses on operational overlap between entities.

Common signs:

- Shared office premises

- Shared employees or management

- Common decision-makers

- Joint branding or marketing

If customers perceive both entities as a single business, the separation may not be considered genuine.

Legitimate Separation Example

Not all business separation is artificial.

For example:

- A franchise model

- Different owners operating under the same brand

- Independent management, finances, and operations

In such cases, even though branding may be shared, the businesses operate independently and for valid commercial reasons.

Strategic Trade-Offs Before Electing SBR

Small Business Relief (SBR) is optional.

While it offers zero corporate tax and simplified compliance, electing for it is not always the smartest decision—especially for growing or loss-making businesses.

Before choosing SBR, businesses should evaluate the long-term tax impact.

Tax Loss Restriction

If you elect for SBR:

- You cannot declare tax losses for that period

- You cannot carry forward losses to future years

- You cannot transfer losses within a group

Why this matters:

If your business is currently making a loss, filing a full corporate tax return (without SBR) may allow you to carry forward that loss and offset it against future profits.

Example:

If your company incurs a AED 1 million loss this year and expects strong profits next year, declining SBR could reduce future tax liability.

Electing SBR means you lose that opportunity.

Net Interest Expenditure Limitation

Under normal corporate tax rules:

- Businesses can carry forward disallowed net interest expenditure

However, during an SBR period:

- The General Interest Deduction Limitation Rules are not applied during an SBR period.

- Any disallowed net interest expenditure cannot be carried forward to future tax periods.

For companies with significant financing costs, this could reduce future tax efficiency.

No Group Relief or Restructuring Relief

If you elect for SBR, you cannot:

- Transfer tax losses within a qualifying group

- Use Business Restructuring Relief

- Transfer assets within a group at net book value

This restriction can affect holding structures and corporate reorganisations.

For businesses planning restructuring or internal transfers, SBR may limit flexibility.

Tax Groups & Small Business Relief

If companies form a Tax Group, they are treated as a single taxable person.

This means:

- The AED 3 million threshold applies to the combined revenue of the entire group

- Not to each company individually

Example:

- Company A earns AED 1.2 million

- Company B earns AED 1.2 million

- Company C earns AED 1.2 million

Total group revenue = AED 3.6 million

Since the combined revenue exceeds AED 3 million, the entire tax group becomes ineligible for Small Business Relief.

Strategic Insight for Growing Businesses

SBR works best for:

- Stable small businesses

- Low-growth businesses

- Businesses without major financing or restructuring plans

It may not be ideal for:

- High-growth startups

- Loss-making businesses expecting future profits

- Groups planning internal transfers

Choosing SBR should be a strategic tax decision—not just a short-term tax saving.

Accounting Options Under Small Business Relief (SBR)

One of the biggest administrative advantages of SBR is simplified accounting.

Eligible businesses (with revenue up to AED 3 million) are allowed to use:

Cash Basis Accounting

Under the cash basis:

- Revenue is recorded when cash is actually received

- Expenses are recorded when payment is made

This is much simpler than the accrual basis, where income and expenses are recorded when earned or incurred, regardless of payment.

For small businesses, this reduces bookkeeping complexity, improves cash flow visibility, and lowers compliance costs.

Compliance Requirements Under SBR

Even though no corporate tax may be payable, compliance obligations still apply.

1. Corporate Tax Registration

- Businesses must register for Corporate Tax

- A Tax Registration Number (TRN) must be obtained

SBR does not exempt you from registration.

2. Filing a Tax Return

- A Corporate Tax Return must still be filed

- The SBR election is made within the tax return for that specific period

Relief is not automatic — it must be actively selected.

3. Record Keeping for 7 Years

Businesses must maintain proper documentation for seven years, including:

- Bank statements

- Sales invoices

- Purchase invoices

- Sales ledgers

- Asset sale documents

- Till rolls and POS records

The Federal Tax Authority (FTA) has the right to audit and request supporting documents to verify revenue eligibility.

When Should You NOT Elect for Small Business Relief?

Small Business Relief is beneficial, but it is not always the best strategic choice. You may consider avoiding SBR in the following situations:

- You expect significantly higher profits next year

If you anticipate strong taxable profits in the future, carrying forward current tax losses could reduce future tax liability. - You are currently in a tax loss position

Electing SBR means you cannot declare or carry forward tax losses. This may eliminate future tax-saving opportunities. - You plan to use group relief

Businesses within a group cannot transfer losses or benefit from restructuring relief if SBR is elected. - You want to carry forward interest expenses

Net interest expenditure incurred during an SBR period cannot be carried forward. - You are close to the AED 3 million threshold and expanding

Crossing the limit even once permanently disqualifies you from SBR.

Practical Examples

Example 1 – Eligible and Beneficial

Revenue: AED 2.5 million

Profit: AED 800,000

Since revenue does not exceed AED 3 million, the business is eligible to elect Small Business Relief (SBR).

Result:

No 9% Corporate Tax payable for that tax period.

Example 2 – Threshold Breach

Revenue: AED 3.2 million

Since revenue exceeds AED 3 million, the business does not qualify for Small Business Relief.

Result:

The business becomes ineligible to elect SBR for that and all subsequent tax periods.

Example 3 – Growth Disqualification

Year 1 Revenue: AED 2.9 million

Year 2 Revenue: AED 3.1 million

Year 1: Eligible to elect SBR.

Year 2: Revenue exceeds AED 3 million.

Result:

The business becomes permanently ineligible to elect SBR from Year 2 onward, even if revenue falls below AED 3 million in future periods.

Conclusion

Small Business Relief is a powerful opportunity for early-stage SMEs under the UAE Corporate Tax regime. It can significantly reduce compliance burden and eliminate the 9% Corporate Tax during eligible periods.

However, it is not suitable for every business. The decision to elect SBR requires careful evaluation of future profits, tax losses, group structure, and growth plans. Since the relief is temporary and available only until 31 December 2026, proper planning and professional guidance are essential before making the election.

FAQs

Is Small Business Relief automatic?

No. SBR is not automatic. You must register for Corporate Tax and specifically elect for the relief in your tax return.

Can Free Zone companies apply for SBR?

Qualifying Free Zone Persons cannot apply for SBR, as they already benefit from a 0% Corporate Tax rate on qualifying income.

What if my revenue fluctuates each year?

Eligibility depends on revenue being AED 3 million or less in the current and all previous tax periods. If you exceed it once, you permanently lose eligibility.

Does VAT affect the AED 3 million threshold?

No. VAT collected is excluded from revenue because it is collected on behalf of the government and does not belong to the business.

Is an audit mandatory under SBR?

An audit is not automatically required for SBR. However, the FTA may review or audit your records to verify eligibility.

Can I switch in and out of SBR every year?

Yes, as long as you remain eligible. However, once you exceed AED 3 million revenue in any period, you cannot elect SBR again.

What happens during an FTA audit?

The FTA may examine revenue records, bank statements, invoices, and business structure to confirm eligibility and check for artificial separation.

Contact Us

An expert will call you within 24 hours. No payment required to get started.

Related Post

.png)

Navigating UAE VAT Compliance

Explore the key changes in UAE VAT compliance for 2024, their implications for businesses, and practical steps to ensure adherence under the latest regulations for seamless tax management.

. 5 min read.png)

UAE Corporate Tax Deadline September 30, 2025 – Filing Buddy Compliance Guide

Stay compliant with UAE corporate tax. Learn who must file, key deadlines, penalties, and how Filing Buddy ensures 100% corporate tax compliance before the September 30, 2025 deadline.

. 3 min read

UAE Scrap Metal VAT Reverse Charge Guide 2026

Learn how the UAE’s scrap metal Reverse Charge Mechanism impacts VAT, compliance, and refunds. Stay compliant and prepare your business today..

3 min