VAT on Barter Transactions UAE: How to Legally Value and Report Non-Cash Deals in Dubai

By filing buddy . 10 Jul 26

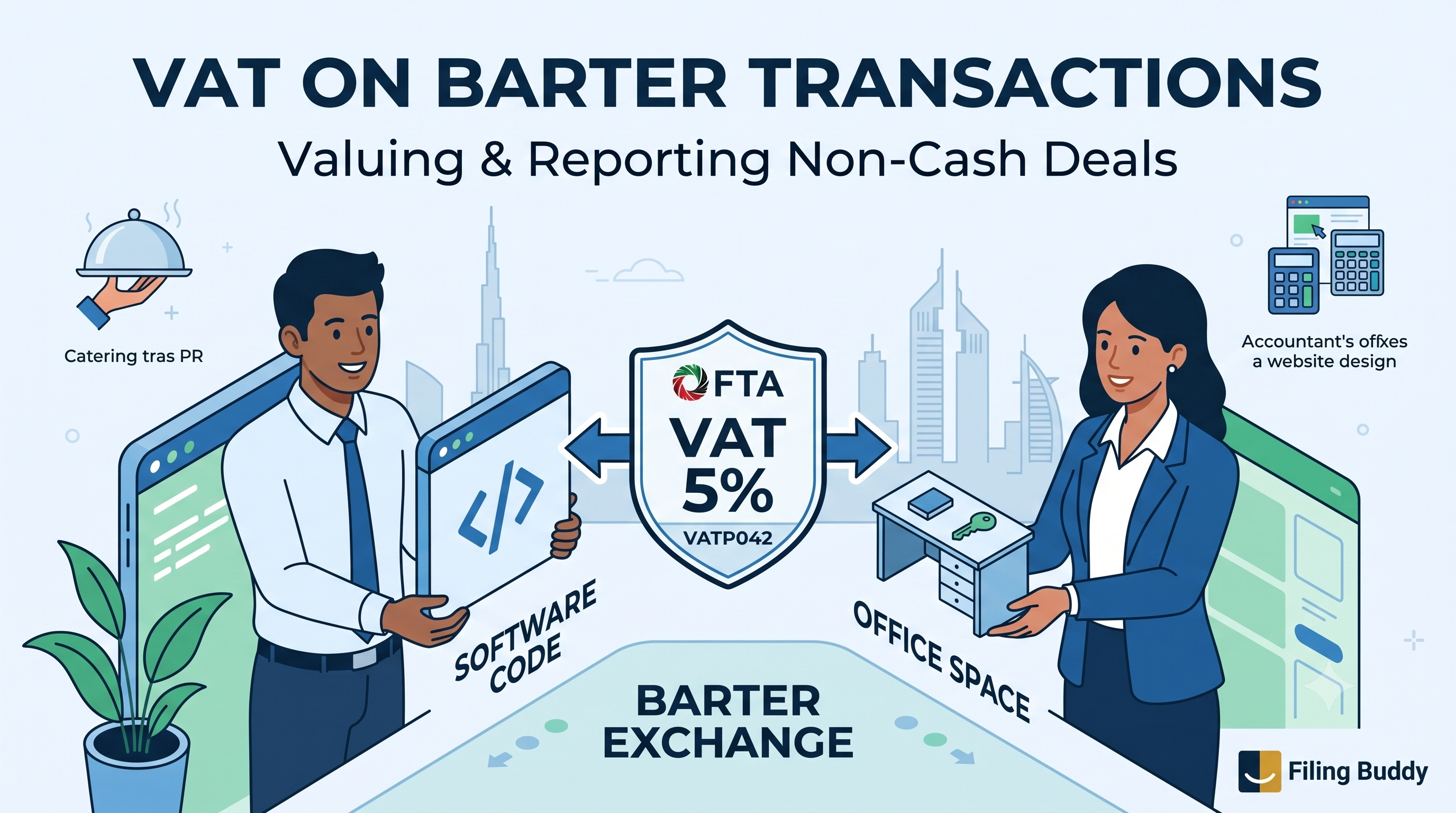

VAT on Barter Transactions: How to Legally Value and Report Non-Cash Deals in Dubai

Under the UAE Federal Tax Authority’s (FTA) VATP042 public clarification, barter transactions are strictly treated as two independent taxable supplies based on the market value of the non-cash goods or services exchanged, requiring both parties to account for and invoice VAT.

Let’s bust a massive myth right now. Many founders assume that if no cash changes hands, there is no tax to pay. In the early days of a startup, trading services—like exchanging software development for free office space, or offering a PR campaign for catering services—feels like a smart, cash-saving hack.

But the FTA does not view this as a casual favor. According to the recent VATP042 public clarification, these non-monetary exchanges are a massive hidden tax trap. Even if your bank account didn't move a single Dirham, the FTA considers both parties to have made a taxable supply. Failing to value, report, and invoice these barter deals leaves your business exposed to immediate tax penalties.

Let’s break down exactly how to protect your dhandha (business) when cash isn't part of the deal.

What Constitutes a Barter Transaction Under UAE VAT? (VATP042 Explained)

A barter transaction under UAE VAT law occurs when two parties exchange goods or services without monetary consideration, legally triggering two separate taxable supplies that must be independently evaluated for VAT at 5%, 0%, or Exempt rates.

When you enter a barter agreement, the FTA essentially splits the deal down the middle. Instead of looking at it as a single trade, the law treats it as if Party A made a distinct sale to Party B, and Party B made a distinct sale to Party A.

Because there are two separate supplies, the VAT treatment for each side might not even be the same. The tax rate applied depends entirely on the specific nature of what you are providing. For example, if you trade mainland commercial real estate services (Standard 5% VAT) for healthcare services (often 0% Zero-Rated), each party must apply their respective tax rules to the transaction.

This means you cannot simply ignore the transaction in your tax returns just because the perceived values "cancel each other out." If you are a VAT-registered entity making a taxable supply, you are legally obligated to declare it, regardless of how your client paid you.

The 3-Step Rule to Determine "Market Value"

To calculate VAT on a barter transaction, the FTA requires businesses to follow a strict 3-step sequential hierarchy to determine the fair "market value" of the non-cash goods or services exchanged.

This is the exact spot where most founders get stuck. If you trade a month of accounting services for a custom website design, how do you put a taxable number on that? You cannot just guess, and you certainly cannot claim the value is zero.

The FTA mandates that the value of your supply is based on the market value of what you received in return. To figure out that exact number, you must follow this three-tier sequential rule:

- Tier 1: The Exact Supply Value (Arm’s Length Price): The FTA first looks at what the exact good or service would sell for in the open UAE market between two completely unrelated parties.

- Example: If a restaurant gives a food blogger a VIP tasting menu in exchange for an Instagram reel, the value of the restaurant's supply is exactly what a normal paying customer would be charged for that menu on a regular Friday night.

- Example: If a restaurant gives a food blogger a VIP tasting menu in exchange for an Instagram reel, the value of the restaurant's supply is exactly what a normal paying customer would be charged for that menu on a regular Friday night.

- Tier 2: The "Similar" Supply Value: If you cannot find the exact market price, you move to Tier 2. You look at what a similar good or service would fetch in the open market under similar conditions.

- Example: If a farmer barters seeds for a rare, unpriced crop of organic tomatoes, they must look at what a comparable variety of organic tomatoes currently sells for in the Dubai market to establish the VAT base.

- Example: If a farmer barters seeds for a rare, unpriced crop of organic tomatoes, they must look at what a comparable variety of organic tomatoes currently sells for in the Dubai market to establish the VAT base.

- Tier 3: The Replacement Cost: What happens if the item is entirely unique and has no market equivalent? You move to Tier 3. The market value defaults to the cost it would take an unrelated supplier to build or replace the identical goods or services.

- Example: If you trade custom-built, one-of-a-kind warehouse machinery for warehouse space, the VAT value is calculated based on what it would cost to build that machinery from scratch today.

- You must follow this order. You cannot skip straight to "Replacement Cost" just because it might give you a lower tax bill. And remember, these values are always calculated excluding the tax amount itself.

Mixed Consideration and Invoicing Requirements

When a transaction involves both cash and non-cash elements (mixed consideration), the total value of the supply is the sum of the cash received plus the market value of the non-cash goods or services, and both VAT-registered parties must issue formal tax invoices to each other.

Sometimes a barter deal is not a straight 100% swap. Let’s say you run an advertising agency and you agree to build a website for a local logistics company. They agree to pay you AED 10,000 in cash, plus free warehouse storage for your equipment for six months.

How do you calculate the VAT on this? The FTA calls this "mixed consideration." You do not just charge VAT on the AED 10,000 cash. You must calculate the fair market value of that six-month warehouse lease, add it to the AED 10,000, and calculate the 5% VAT on the total combined amount.

The biggest mistake founders make here is skipping the paperwork because the transaction feels informal. Under VATP042, if both parties are VAT-registered, a handshake is not enough. You must legally issue mutual tax invoices.

Here is exactly what must happen to stay compliant:

- Mutual Invoicing: You must issue a tax invoice to the logistics company for the website design, and they must issue a tax invoice to you for the warehouse storage.

- Net vs. Gross Breakdown: Your tax invoice must clearly separate the Net Value of the supply, the 5% VAT amount, and the Total Consideration (Gross Amount).

- Proper VAT Returns: Both of you must declare these supplies as output tax in your respective quarterly VAT returns, just as you would for a standard cash-based sale.

If you fail to issue these invoices, the FTA views it as underreporting your taxable income. During an audit, this triggers immediate administrative penalties for both failing to issue a tax invoice and failing to account for the correct output VAT.

Actionable Checklist: How to Protect Your Non-Cash Deals Right Now

To fully comply with VATP042, businesses engaging in barter must formally document the exchange value in a contract, establish a supportable market value for the items exchanged, and issue mutual tax invoices before filing their next VAT return.

You cannot leave non-cash deals off the books. If your startup relies heavily on trading services to preserve cash flow, you need a strict internal process to ensure these deals do not trigger a massive FTA penalty.

Here is your immediate execution plan:

- Draft a Formal Barter Agreement: Never rely on a verbal agreement or an informal email. Draft a simple contract that explicitly states what is being exchanged, the agreed-upon market value of each supply, and the fact that both parties will issue a VAT-compliant tax invoice.

- Document Your Valuation Method: Do not just pull a number out of thin air. Keep a screenshot of your standard pricing sheet, a link to a competitor's similar service, or a quote for replacement costs in your files. If the FTA audits the transaction, you must prove exactly how you arrived at that specific tier of the valuation hierarchy.

- Issue Mutual Tax Invoices Immediately: As soon as the barter transaction takes place, generate a tax invoice showing the gross consideration, the net value, and the 5% VAT. Demand the same from your barter partner.

- Account for the Output Tax in Your Return: Ensure your finance team explicitly includes the value of the bartered supply in your quarterly VAT return as standard output tax.

Your Next Step with Filing Buddy

Barter transactions are an incredible way to grow your business without burning cash, but the tax mechanics are a minefield. You are a builder, not a tax auditor.

As your Dhandhe Ka Saathi, Filing Buddy simplifies this entirely. We help you establish the correct FTA-approved market value for your unique services, generate compliant mutual tax invoices, and seamlessly report these non-cash deals in your quarterly VAT returns. Do not risk a painful audit over a free service trade. Reach out to Filing Buddy today, and let us bulletproof your non-cash transactions.

FAQs

Do I have to pay VAT if I exchange services for goods in Dubai?

Yes, exchanging services for goods is a barter transaction, and under UAE law, both parties must account for and report VAT based on the market value of what they supplied.

A lack of cash does not mean a lack of tax liability. If you are VAT-registered and the service you provide is normally taxable, you must calculate the 5% VAT on the fair market value of your service and declare it on your next VAT return, exactly as if the client had paid you in cash.

How do you calculate VAT on a barter transaction?

VAT on a barter transaction is calculated by determining the market value of the non-cash consideration received and applying the relevant VAT rate (e.g., 5%) to that amount.

To find the correct market value, you must use the FTA's 3-step hierarchy: First, use the exact market price of the item. If that is unavailable, use the price of a similar item. If both are unavailable, calculate the replacement or build cost.

What is mixed consideration under UAE VAT law?

Mixed consideration occurs when a transaction is paid for using a combination of both cash and non-cash items, such as receiving AED 5,000 plus a free laptop for your services.

In these scenarios, your total taxable supply is the sum of the cash you received plus the fair market value of the non-cash items. You must calculate the 5% VAT on this total combined amount and issue a tax invoice reflecting both forms of payment.

Contact Us

An expert will call you within 24 hours. No payment required to get started.

Related Post

.png)

Decoding FTA Guidelines: Aggregated Financial Statements & Audit Compliance for UAE Corporate Tax Groups

Understand AFS rules and audit compliance for UAE Tax Groups under FTA guidelines. Learn key conditions, disclosures, and deadlines with expert Filing Buddy support.

. 5 min read.png)

UAE Free Zone Corporate Tax Updates

Unlock 0% UAE Free Zone tax benefits. Discover 2025 updates on qualifying activities and pricing rules—act now to stay compliant and avoid penalties.

. 3 min read.png)

UAE E-Invoicing – Complete Guide (2026)

Comprehensive guide to UAE eInvoicing (2026): understand DCTCE 5-corner model, XML invoices, FTA compliance, implementation timeline, and how businesses can prepare.

. 5 min read