LLP Agreements: Creating a Solid Foundation for Your Business

By Jyotisman . 02 May 25

3.png)

Creating a Solid Foundation for Your Business with Limited Liability Partnership (LLP) Agreements

Starting and running a business can be an exciting and rewarding endeavor, but it also comes with its fair share of responsibilities and potential risks. One legal structure that offers a balance between personal liability protection and flexibility is the Limited Liability Partnership (LLP).

In this comprehensive guide, we'll explore what an LLP is, its features, the rights and duties of partners, the role of designated partners, the liabilities of partners in an LLP, and the importance of creating a solid foundation for your business with a well-crafted LLP Agreement.

What is a Limited Liability Partnership (LLP)?

A Limited Liability Partnership (LLP) is a business structure that combines the benefits of a partnership with limited liability protection, typically associated with corporations. It is designed to provide a more flexible and tax-efficient framework for professionals and businesses with multiple partners.

Limited Liability Partnership Features:

1. Limited Liability: One of the primary features of an LLP is that partners' personal assets are protected from the business's debts and liabilities. This means that if the LLP faces financial trouble, the personal assets of partners, such as homes and savings, are generally safe.

2. Pass-Through Taxation: Similar to a general partnership, an LLP offers pass-through taxation. This means that the LLP itself is not subject to income tax. Instead, profits and losses are reported on the individual tax returns of the partners.

3. Management Flexibility: LLPs offer more flexibility in management compared to corporations. Partners have the freedom to define the roles, responsibilities, and decision-making processes within the LLP.

4. No Minimum Capital Requirement: Unlike some other business structures, LLPs typically do not require a minimum capital investment. This allows professionals to start their practice without significant upfront costs.

Rights and Duties of Partners in an LLP

In an LLP, partners have specific rights and duties. Understanding these is crucial to ensuring a smooth and productive partnership.

Rights of Partners:

1. Right to Participate: Partners have the right to actively participate in the management and decision-making of the LLP, depending on the terms of the LLP Agreement.

2. Right to Share in Profits: Partners are entitled to a share of the profits as per the LLP Agreement or as agreed upon.

3. Right to Information: Partners have the right to access the LLP's financial and operational information.

4. Right to Inspect Books: Partners can inspect and review the books and records of the LLP.

Duties of Partners:

1. Duty of Good Faith: Partners have a fiduciary duty to act in good faith and in the best interests of the LLP.

2. Duty of Loyalty: Partners must act loyally and avoid conflicts of interest. They should not compete with the LLP or take actions that harm the partnership.

3. Duty of Care: Partners should exercise reasonable care and diligence in their roles, making decisions that are in the best interest of the LLP.

4. Duty to Contribute: Partners may be required to contribute capital as agreed upon in the LLP Agreement.

Role of Designated Partner in an LLP

In an LLP, there is a specific role called the "Designated Partner." This individual holds a unique position with certain responsibilities.

Responsibilities of a Designated Partner:

1. Fulfilling Compliance: Designated partners are responsible for ensuring that the LLP complies with all statutory requirements and filings.

2. Maintaining Records: They maintain and preserve all records required by the LLP Act.

3. Representing the LLP: Designated partners often act as the face of the LLP, representing it in various legal matters and transactions.

4. Liabilities: They may have additional liabilities compared to other partners if the LLP fails to meet its compliance obligations.

Liabilities of Partners in an LLP:

1. Limited Personal Liability: As the name suggests, partners in an LLP have limited personal liability. This means that their personal assets are typically not at risk in the event of business debts and liabilities.

2. Liability for Own Actions: Partners are generally liable for their own actions and negligence but not for the actions of other partners.

3. Liability for Unfulfilled Obligations: If a partner fails to fulfill their obligations under the LLP Agreement, they may be personally liable for any resulting losses.

4. Liability for Non-compliance: Designated partners are specifically responsible for LLP compliance. If the LLP fails to meet compliance requirements, the designated partners may face personal liability.

The Importance of an LLP Agreement:

1. Defining Partner Roles: An LLP Agreement clearly defines the roles and responsibilities of each partner, preventing conflicts and misunderstandings.

2. Profit Sharing: The agreement outlines how profits and losses will be distributed among partners, ensuring transparency.

3. Decision-Making Processes: It specifies how decisions will be made within the LLP, streamlining the decision-making process.

4. Dispute Resolution: In the event of conflicts or disputes, the agreement provides a framework for resolution.

5. Compliance with Legal Requirements: An LLP Agreement helps the LLP meet legal requirements and obligations.

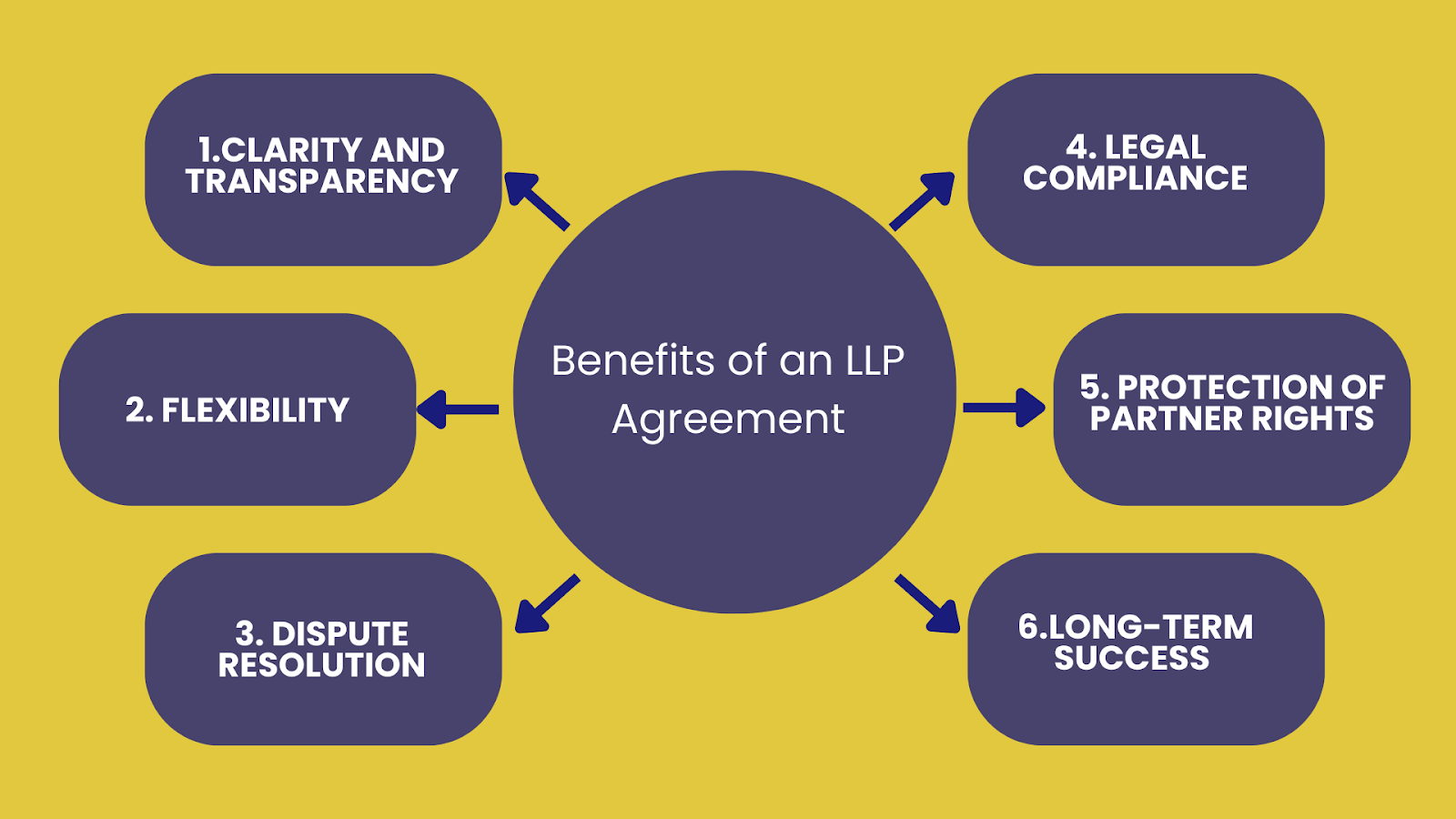

The Benefits of an LLP Agreement:

Creating an LLP Agreement is a crucial step in building a solid foundation for your business. Let's explore some of the benefits of having a well-crafted LLP Agreement.

1. Clarity and Transparency:

- An LLP Agreement clarifies the roles and responsibilities of each partner, ensuring that everyone is on the same page. This clarity reduces the likelihood of misunderstandings and conflicts.

2. Flexibility:

- The agreement allows partners to define how decisions will be made and how profits and losses will be shared. This flexibility is especially valuable for LLPs with complex structures or unique requirements.

3. Dispute Resolution:

- In the event of disagreements or disputes, the LLP Agreement provides a framework for resolution. This can help partners resolve issues without resorting to legal action.

4. Legal Compliance:

- An LLP Agreement helps the LLP meet legal requirements and obligations. It ensures that the partnership is structured in accordance with relevant laws and regulations.

5. Protection of Partner Rights:

- The agreement safeguards the rights of partners, including their financial interests and decision-making authority.

6. Long-Term Success:

- By clearly defining the terms of the partnership, the LLP Agreement sets the stage for long-term success. Partners can work together more effectively, knowing that their interests and roles are protected.

Additional Resources for Your LLP Success

To further support your LLP's success, consider the following additional resources and best practices:

1. Continuous Communication: Maintain open and regular communication with your partners. A strong partnership requires ongoing dialogue and collaboration.

2. Professional Legal Advice: Consult with a legal professional who specializes in business law to ensure that your LLP Agreement is comprehensive and compliant with all relevant laws.

3. Regular Updates: Periodically review and update your LLP Agreement to reflect changes in the business, new partners, or evolving needs.

4. Tax Planning: Work with a tax advisor to optimize your tax strategy and take full advantage of the tax benefits available to LLPs.

5. Business Insurance: Explore business insurance options to further protect your LLP from unforeseen risks and liabilities.

Creating a Solid Foundation for Your LLP with an LLP Agreement:

To ensure a successful and harmonious partnership, it's vital to create a comprehensive LLP Agreement. This document outlines the terms and conditions of the partnership, including the rights, duties, and responsibilities of each partner, profit-sharing arrangements, decision-making processes, and dispute resolution mechanisms. It's a legally binding contract that governs the LLP's operation, and with the expert guidance of Filing Buddy, you can simplify the process and ensure your agreement aligns with all legal requirements.

Contact Us

An expert will call you within 24 hours. No payment required to get started.

Related Post

LLP vs. LLC: Choosing the Right Structure for Your Business

Making the appropriate legal structure choice is one of the most important decisions you'll need to make when launching a business in India. Limited Liability Companies (LLCs) and Limited Liability Partnerships (LLPs) are two well-liked alternatives.

. 3 min read.png)

Revised LLP (Amendment) Rules for 2023 – Enhanced LLP Form No. 3

The Ministry of Corporate Affairs (MCA) has recently issued the Limited Liability Partnership (LLP) (Amendment) Rules, 2023, which were officially gazetted on June 2, 2023. These rules bring about amendments to the pre-existing Limited Liability Partnership Rules of 2009. These amendments came into effect upon their publication in the Official Gazette. A noteworthy change introduced through these amendments is the revision of the LLP Form No.3, which pertains to "Information concerning Limited Liability Partnership Agreement."

. 3 min read.png)

Zepto: On Track to Profitability? Understanding the Company's Financial Landscape.

Learn how Zepto India has emerged as a game changer in the online grocery delivery market. Discover how its operations surprised many.

. 5 min read