Company Valuation for Startups: How to Calculate Your Startup’s True Worth in 2025

By Filing Buddy . 21 Jul 25

Why Startup Valuation Matters More Than Ever

Ever watched Shark Tank and wondered how founders throw out a ₹50 crore valuation with full confidence even without profits?

Welcome to the world of startup valuation, where numbers meet narratives, and potential often weighs more than profits. If you're a founder raising your first round, or just starting to explore entrepreneurship in India’s booming startup ecosystem, understanding company valuation is not just helpful, it's non-negotiable.

So… what is valuation, really?

At its core, company valuation is the process of figuring out what your business is worth either in today’s market or based on its future potential. When we say startup valuation, we’re typically talking about early-stage companies that may not have steady revenues (yet) but have high growth potential.

Think of valuation as your company’s price tag but one that changes based on context: investor expectations, market opportunity, competition, team strength, and even trends.

Did You Know?

India saw over $10 billion in venture capital investments in 2024 alone. Most of those deals were made without the startup turning a profit thanks to forward-looking valuations based on future growth!

Why does this matter more than ever?

- Fundraising: Your valuation determines how much equity you give up for investment. Undervalue it? You lose ownership. Overvalue it? You might scare off investors.

- Attracting Strategic Investors: A sound valuation tells investors you know your numbers, market, and vision.

- Long-term Strategy: Valuation impacts everything from ESOPs to acquisitions to IPO planning.

Pro Tip From a Founder’s Desk

“Your startup’s valuation is not about what you’ve done. It’s about what you can do. You’re selling a future so make it believable, not hypothetical.”

Quick Checklist: Is This You?

- You’re building your first pitch deck

- You want to raise funding in the next 6–12 months

- You’re unsure how to value your pre-revenue startup

You’ve Googled “how to calculate valuation of a startup” at least once

If yes, this guide is exactly where you need to be.

What is Company Valuation? (And Why It’s Not Just About Revenue)

In the sections ahead, we’ll break down the different valuation methods, when to use them, and how to align them with your startup journey. Because understanding valuation isn’t just about impressing investors it’s about owning your story.

But before we get into the “how,” let’s clarify the “what.”

What is Company Valuation, Really?

At its simplest, company valuation refers to the process of determining the economic worth of a business whether it’s a ₹10 lakh bootstrapped D2C brand or a ₹100 crore SaaS scaleup. But here's the twist: the value of a company isn’t set in stone. It can differ wildly depending on who's looking and why.

There are two lenses through which a startup’s value is usually viewed:

- Intrinsic Value: The “real” worth of your company based on fundamentals like future cash flows, growth potential, and business risks.

- Market Value: The price someone is actually willing to pay for your company today driven by investor sentiment, trends, and comparisons with other startups.

Ever noticed how two startups with similar revenue get very different valuations? That’s intrinsic vs market value in action.

Storytime The Same Numbers, Two Valuations

An edtech founder with ₹80 lakh in annual revenue gets a ₹5 crore valuation. Meanwhile, a healthtech founder with the same revenue lands a ₹15 crore term sheet. Why?

Because the market values the healthtech sector more aggressively in 2025 it's viewed as future-forward, scalable, and in high demand.

The Core Principles Behind Every Valuation

Whether you’re using basic valuation models or complex forecasting spreadsheets, every calculation boils down to a few key ideas:

Time-Specific: Your startup’s value changes with time, especially in fast-moving markets. Today’s ₹2 crore valuation might be ₹4 crore next quarter or ₹1 crore if your traction drops.

Future Cash Flows Matter: Most models, especially the value of the company formula in Discounted Cash Flow (DCF), are based on how much money your business could generate in the future, not just what it makes today.

Market Forces Influence Valuation: Trends, competition, investor appetite, and even government policies (like DPI or startup incentives) shape what the market is willing to pay.

Liquidity Increases Value: Startups with healthy reserves or clear paths to revenue are seen as lower risk improving what we call the net valuation of the business.

Underlying Assets Count: Got strong IP, a growing customer base, or proprietary tech? These assets boost your valuation even before the profits roll in.

Did You Know?

Some of India’s most valuable startups like Zerodha or Razorpay focused heavily on profitability and liquidity, which boosted their net valuation over time and made them investor favorites in tough markets.

“Valuation isn’t a number you pull out of a hat, it's a story backed by logic. The stronger your fundamentals, the more credible your pitch.”

So, while revenue helps, it’s far from the whole picture. The real value of your startup comes from your vision, traction, and the belief that you can turn tomorrow’s potential into today’s numbers.

Mini-Scenario: D2C Founder with No Profits – What’s Your Valuation?

Let’s make this real.

Imagine you’re a 23-year-old founder from Bengaluru who just launched a D2C skincare brand. You’ve bootstrapped it with savings, built a solid Instagram following, and done ₹12 lakhs in sales over the last 6 months. There’s buzz, influencers are talking, and repeat orders are climbing.

But here’s the kicker:

You’re not profitable. You’re reinvesting everything into packaging, influencer marketing, and fulfillment.

And now, an angel investor you met at a co-working event asks:

“So, what’s your startup’s valuation?”

Valuation With No Profits? Yes, It’s Possible.

This is where the real-world complexity of startup valuation kicks in.

Valuation isn’t just a revenue game. It's about traction, momentum, and perceived future value.

- Your sales velocity proves demand

- Your customer retention shows product-market fit

- Your influencer ROI and growth metrics hint at scalability

Even without profits, an investor might still assign a ₹3–5 crore valuation based on:

- Projected revenue over 12–18 months

- Comparable D2C deals in the market

- Strength of brand recall and digital community

- Total addressable market (TAM) in India’s ₹20,000+ crore skincare industry

Valuation = Art + Science

Unlike mature businesses where cash flow formulas dictate value, early-stage startup valuation is 50% financial logic and 50% founder narrative.

Did You Know?

Nykaa raised its first round with minimal profits but massive belief in the Indian beauty e-commerce boom; its valuation was built on future dominance, not current balance sheets.

“If you’re pre-profit, show clear traction metrics and unit economics. VCs and angels invest in momentum, not just numbers.”

So, when you’re asked “What’s your company valuation?” don’t panic if your P&L doesn’t sparkle yet. If you can prove future value with current momentum, you're in the game.

Types of Startup Valuation Methods

Now that we’ve seen how valuation isn’t just about profits, let’s explore the actual valuation methods founders and investors use to determine what a startup is worth.

Broadly, we can split them into two buckets:

a. Relative Valuation Models (based on comparisons)

b. Absolute Valuation Models (based on intrinsic characteristics)

a. Relative Valuation Models: What’s Everyone Else Worth?

In a nutshell, relative valuation compares your startup to other similar companies in your industry to find a fair value.

It’s fast, intuitive, and super common in early-stage investing.

Think of it like this: if a similar D2C startup raised funds at a ₹10 crore valuation with ₹1 crore in revenue, and your revenue is ₹80 lakhs with better growth, your valuation might fall in the ₹8–10 crore range.

This method relies heavily on valuation multiples such as:

- P/E Ratio (Price to Earnings): Most useful for profitable companies.

- EV/EBITDA: Popular in private equity and mature businesses.

- P/S Ratio (Price to Sales): Often used in early-stage startups that have revenue but no profits.

Example:

Startup A (your competitor) just raised ₹5 crores at a 10x revenue multiple. You’re growing faster with similar gross margins. Using the same relative valuation method, your fair valuation could be ₹6–7 crores.

“Investors don’t value you in isolation. They look at benchmarks who else is raising, at what stage, and how you're positioned.”

When to Use This Method:

- You have revenue but limited profitability

- There are comparable startups in the same sector

- You need a fast, investor-friendly way to position your worth

b. Absolute Valuation Models: What Are You Really Worth?

Unlike relative models, absolute valuation focuses purely on your startup’s internal fundamentals, projected cash flows, growth rate, risk regardless of what others are doing.

Let’s break this into key sub-methods:

Discounted Cash Flow (DCF)

The Discounted Cash Flow method is a favorite among financial analysts and VCs who want a grounded, future-focused valuation. It estimates the present value of your startup based on projected free cash flows, discounted using an appropriate risk rate.

Imagine your SaaS startup expects to generate ₹1 crore in free cash flow annually for the next 5 years. Using DCF, those future cash flows are “discounted” back to their present value.

Business Value Formula (Simplified):

Startup Value = Σ (Free Cash Flow in Year N / (1 + Discount Rate)^N)

Free Cash Flow = Cash from Operations – Capital Expenditure

Mini Scenario:

Your fintech app projects ₹50 lakhs in free cash flow next year. Using a 12% discount rate, the present value is ₹44.6 lakhs. You do this for 5 years, add a terminal value and boom, your valuation is ₹3–5 crores.“DCF is only as good as your projections. Keep them realistic, and always show the assumptions to investors.”

Discounted Dividend Model

Used more in traditional businesses or late-stage startups, this model assumes that dividends are the primary return to investors. Not ideal for most early-stage Indian startups (since you’re likely reinvesting profits), but good to know.

Formula (Gordon Growth Model):

Value of Stock = Dividend per Share / (Discount Rate – Dividend Growth Rate)

Use This If:

- Your startup is profitable and pays consistent dividends (rare in early stages)

- You’re valuing a holding company or cash-flow-rich business

Capital Asset Pricing Model (CAPM)

The CAPM helps calculate the expected return on equity for your investors and it’s often used in conjunction with DCF to decide the discount rate.

Think of CAPM like riding a bike in traffic: the riskier the road (market), the higher the reward you expect for taking it.

CAPM Formula:

Re = Rf + β × (Rm - Rf)

Where:

- Re = Expected Return

- Rf = Risk-Free Rate (e.g. 10-year government bond)

- β (Beta) = Risk of your startup vs the market

- (Rm – Rf) = Market Risk Premium

“Beta is like your startup’s heartbeat compared to the market. High beta? Fast growth, but volatile. Low beta? Stable, but slower scale.”

Quick Checklist: Choosing the Right Method

| Stage | Revenue | Profitability | Best Fit Model |

| Early | No | No | Relative (P/S) |

| Mid | Yes | Low | DCF + CAPM |

| Late | Yes | Yes | DCF or Dividend Model |

With these valuation models in your toolkit, you can now start backing up your pitch with real logic not just ambition.

Quick Checklist: Which Valuation Method Should You Use?

Ever found yourself stuck wondering which valuation model is “right” for your startup? Should you go with a DCF even if your startup has no stable cash flow? Or use P/E multiples when you haven’t turned a profit yet?

Here’s the good news you don’t need an MBA to figure this out. Below is a simple decision-making checklist tailored for Indian founders to help you choose the right valuation method based on your business stage, profitability, and industry.

Mini Scenario:

Riya, the founder of a bootstrapped SaaS platform, is raising her seed round. She has ₹10L in monthly recurring revenue but is reinvesting every rupee. She's confused: Should she use DCF, or a relative valuation model like EV/Revenue?

Let’s break it down.

Quick Valuation Checklist for Founders

| Criteria | Best Valuation Method | Why It Works |

| Pre-revenue startup (idea stage) | Scorecard or Berkus Method (Covered in bonus section) | Focuses on team, product vision, and market potential |

| Early-stage (Revenue but no profits) | Relative Valuation (e.g. EV/Revenue, P/S Ratio) | Compares you to competitors based on traction metrics |

| Profit-generating startup | P/E Ratio, EV/EBITDA | Strong profits allow comparison using earnings-based metrics |

| Cash flow visibility (3–5 years) | Discounted Cash Flow (DCF) | Ideal for forecasting intrinsic value using free cash flow |

| Dividend-paying startups (rare in India) | Discounted Dividend Model | Used when regular dividends are distributed |

| High-risk, volatile sector (e.g. crypto, defense tech) | CAPM Model | Helps calculate expected return based on market risk |

Quick Self-Test:

Can you guess which method works best for a D2C startup that’s breaking even but has huge influencer traction?

Relative valuation (like P/S Ratio) is your friend here. You're not profitable yet, but your growth and brand equity matter.

Did You Know?

Most early-stage investors in India use a mix of intuition, comparable deals, and simple revenue multiples especially in sectors like D2C, EdTech, and FinTech.

“As a founder, the goal is not to pick the most complex formula. It’s to pick the one that helps you and the investor speak the same language.”

- There is no one-size-fits-all business valuation formula; it depends on where you are in your journey.

- Relative methods work better when cash flows are unpredictable.

- Absolute methods work when you have historical or forecastable financial data.

Always align your method with your fundraising narrative.

Did You Know? Fun & Surprising Startup Valuation Facts

Startup valuations aren't just about formulas they're also about perception, timing, and the story you sell.

Here are some eye-opening valuation facts from the Indian and global startup ecosystem that show just how varied and unexpected startup valuations can be, even within the same industry:

Zomato’s IPO Valuation: Just ~1x Revenue

When Zomato went public in 2021, its valuation was roughly 1x its revenue (₹4,000 crore revenue vs ~₹4,000 crore valuation at listing).

Despite being a household name with a massive user base, Zomato’s valuation was constrained by losses and public market scrutiny. This shows that public markets often lean conservative compared to VC investors.

Valuation Insight:

Public investors rely more on fundamentals startup valuation based on revenue multiples here reflects caution over cash burn.

Meesho Raised at 12x Revenue

In contrast, Meesho, a social commerce platform, raised funds at nearly 12x its annual revenue in a private round.

Why the premium? Because investors saw viral growth, market dominance in Tier II–III cities, and a scalable low-CAC model despite operating losses.

Valuation Insight:

In private markets, startup valuation is driven by narrative + future potential, not just present profits.

HealthifyMe Once Raised at 16x ARR

Health-focused startups like HealthifyMe have commanded high valuation multiples due to niche markets, low churn, and high LTV. In one of its funding rounds, insiders report it was valued at 16x ARR (Annual Recurring Revenue).

Valuation Insight:

SaaS or subscription startups can fetch higher business valuation due to predictable recurring revenue streams.

Neobank Valuations Can Be 25x+ Revenue

Several Indian neobanks have raised money at 20–25x their revenue, especially when targeting underserved fintech sectors (e.g. Razorpay, Jupiter). Why? Because investors price in long-term monetization and market size.

| Company | Valuation Multiple | What Drove It? |

| Zomato | ~1x Revenue | Losses + public market realism |

| Meesho | ~12x Revenue | Growth narrative + market dominance |

| HealthifyMe | ~16x ARR | Recurring revenue + niche appeal |

| Jupiter/Razorpay | 20–25x Revenue | TAM + monetization potential |

“A startup’s valuation multiple is not fixed; it's a reflection of momentum, market belief, and story clarity.”

From the Founder’s Desk: Common Mistakes in Startup Valuation

Insights for Early-Stage Entrepreneurs

Getting your startup valuation right is more than just crunching numbers; it's about setting realistic expectations and building investor trust. As someone who has sat across the table from investors, here are the most common startup valuation mistakes I see founders make (and how to avoid them):

1. Overestimating TAM (Total Addressable Market)

It’s tempting to claim your product addresses a "$100 billion market" but remember, investors value realism over hype.

What goes wrong?

Founders often confuse TAM with actual serviceable markets or ignore constraints like regional regulations, customer affordability, or competition.

Valuation Insight: Overblown TAM leads to inflated startup valuation expectations and can damage credibility.

Tip: Use conservative market sizing, and clearly define your SAM (Serviceable Available Market) and SOM (Serviceable Obtainable Market) in your pitch.

2. Misusing Comparable Valuations

Startups often say: “X company raised at ₹200 Cr, we should too.”

But comparing your early-stage D2C brand to a Series C SaaS unicorn is a flawed approach.

What goes wrong?

Misaligned comparables result in unrealistic expectations and poorly calibrated equity offers.

Valuation Insight: Investors look at comparables, yes but only if they share industry, growth metrics, and stage.

Tip: Select 3–5 relevant benchmarks, ideally using a startup valuation calculator or platforms like Tracxn, PitchBook, or Crunchbase to stay grounded.

3. Ignoring Burn Rate & Cash Flow in Valuation of Startups

Valuation isn’t just top-line growth how much you’re burning each month matters.

What goes wrong?

Founders ignore their runway, or set high valuations without sustainable monetization plans.

Valuation Insight: If your startup burns ₹20 lakhs a month with low retention, a high share valuation becomes unjustifiable, no matter the revenue.

Tip: Balance growth potential with cost efficiency. Investors reward those who can grow smartly, not just quickly.

4. Blindly Trusting Startup Valuation Calculators

Online startup valuation calculators are good directional tools, but not gospel truth.

What goes wrong?

Founders get misled by automated tools that ignore nuances like brand equity, founder reputation, team strength, or market timing.

Valuation Insight: Calculators don’t capture qualitative drivers use them as a supporting input, not the final answer.

Tip: Combine calculator estimates with real investor feedback and professional advisory support.

“Your startup’s valuation is not a trophy, it's a reflection of your business fundamentals, market narrative, and execution clarity.”

Avoid these common traps, and you’ll be far better prepared for investor conversations whether you're raising Pre-Seed, Seed, or Series A.

Quick Self-Test: Can You Pick the Right Valuation Method?

Think you’ve understood how startup valuation works? Let’s put your instincts to the test. Below are 3 common startup scenarios that choose the most suitable valuation method for each.

No right or wrong, just smart guidance based on investor behavior and real-world logic.

Scenario 1: Bootstrapped D2C Startup (₹10L MRR, Profitable)

You’ve grown organically over 2 years, have steady revenue, and a loyal customer base — but no external funding yet.

Which method fits best?

A. Comparable Company Analysis

B. Discounted Cash Flow (DCF)

C. Berkus Method

D. First Chicago Method

Correct Approach: A – Comparable Company Analysis

Since you're profitable with traction, investors will benchmark you against similar bootstrapped D2C startups to estimate your share valuation.

Scenario 2: Funded B2B SaaS Startup (₹1.5Cr ARR, 30% MoM Growth)

You’ve raised a Seed round and have consistent SaaS revenue with strong retention and low churn.

What’s the right method here?

A. Scorecard Valuation

B. Revenue Multiple Method

C. Cost-to-Duplicate

D. Risk Factor Summation

Correct Approach: B – Revenue Multiple Method

B2B SaaS startups are typically valued using ARR-based revenue multiples, especially when growth is predictable.

Scenario 3: Pre-Revenue AI Tech Platform

Your MVP is ready, you have a strong team, and early interest but no paying customers yet.

What valuation approach works here?

A. DCF

B. Berkus Method

C. Market Multiple

D. Liquidation Value

Correct Approach: B – Berkus Method

For pre-revenue startups, especially tech platforms, the Berkus Method helps quantify valuation based on intangible drivers like idea quality, team, and prototype readiness.

Why This Matters:

Knowing which startup valuation method fits your business model helps:

- Set realistic investor expectations

- Strengthen your pitch narrative

- Avoid undervaluing or overhyping your company

Every founder should know when to use a startup valuation calculator and when to rely on investor-aligned frameworks like Berkus, Scorecard, or ARR multiples.

Bonus: Startup Valuation Formulas You Can Try Right Now

Whether you're building your pitch deck or preparing for a “Shark Tank” moment, knowing the math behind how to calculate company valuation gives you an edge.

Let’s break down some simplified, yet powerful business valuation formulas you can actually apply — even without a finance degree.

1. Discounted Cash Flow (DCF) – Future-Proof Valuation

DCF is great for startups with predictable future cash flows.

Formula:

Where:

- CF= Expected future cash flow

- r= Discount rate (usually 12–25% for startups)

- n= Number of years forecasted

Use it when: You have revenue projections and want to estimate your company's present value.

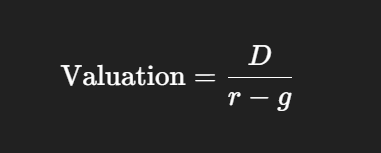

2. Dividend Discount Model – Rare but Real

If your startup pays (or plans to pay) dividends:

Formula:

Where:

- D= Expected annual dividend

- r= Required rate of return

- g= Growth rate of dividends

Use it when: You’re a profitable, dividend-paying business (more common post-Series B+).

3. Market Cap / Earnings Shark Tank Style Valuation

This is what investors use to benchmark you quickly.

Formula:

Where:

- P/E = Price to Earnings (typical range for startups is 10–30x)

- Revenue multiple = Depends on industry (SaaS often gets 6–12x)

Use it when: You want a fast benchmark, like in a “Shark Tank” pitch works well for profitable or scaling startups.

How to Calculate the Value of a Company?

| Method | Best For | Formula Style |

| DCF | Predictable cash flows | Cash flow projection × risk-adjusted discount |

| Dividend Model | Dividend-paying businesses | Dividends ÷ (Discount Rate – Growth Rate) |

| P/E or Revenue Multiple | Quick benchmark valuation | Profit × P/E OR Revenue × Multiple |

Even if you're not a finance pro, having a grip on at least one business valuation formula helps you justify your startup valuation during fundraising or exit planning.

Final Thoughts: Your Valuation is a Story Tell It Well

Startup valuation isn’t just a number on a spreadsheet, it's a reflection of your vision, traction, market potential, and belief in your business.

Investors don’t just buy numbers, they buy narratives.

Whether you're using DCF, revenue multiples, or any other valuation method, remember that the how matters just as much as the what. A compelling story backed by logical numbers can help you win trust, funding, and long-term partners.

Recap: What You’ve Learned

- Startup valuation is a mix of data and storytelling.

- Multiple valuation methods exist based on your business model and growth stage.

- You now understand how to calculate valuation of a startup using simplified formulas, founder-friendly logic, and real-world investor expectations.

Ready to Take the Next Step?

Want help building your pitch deck and backing it with data-driven valuation?

Talk to our Startup Experts – Let’s co-create a deck that sells your vision.

Key Takeaways

What is Startup Valuation?

It’s the process of determining how much your startup is worth today based on traction, potential, risk, and comparable benchmarks.

Why Does It Matter?

Startup valuation shapes how much equity you give up, how investors perceive you, and what milestones you’re expected to hit next.

Types of Valuation Models You Should Know

- Discounted Cash Flow (DCF) – Future cash flow based

- Revenue Multiples – Popular in D2C, SaaS

- Scorecard & Berkus – Great for early-stage, pre-revenue startups

- Market Comparables – Based on similar companies' valuations

- P/E Ratios & Market Cap – More useful in mature stages or public comparisons

Which Method is Best for You?

- Pre-revenue → Use Scorecard or Berkus

- Bootstrapped but profitable → Try DCF or earnings multiples

- VC-funded SaaS → Go for revenue multiples

- Fintech or complex IP startups → Combine DCF + Comparables

Formula Cheat Sheet

- DCF Formula:

Value=CF1/(1+r)1+CF2/(1+r)2+...+CFn/(1+r)nValue = CF₁ / (1 + r)¹ + CF₂ / (1 + r)² + ... + CFₙ / (1 + r)ⁿ

(Where CF = Cash Flow, r = discount rate) - Revenue Multiple:

Valuation=Revenue×IndustryMultipleValuation = Revenue × Industry Multiple - P/E Ratio:

Valuation=Earnings×P/ERatioValuation = Earnings × P/E Ratio

Startup Valuation (Shark Tank style):

Valuation= Amount Asked ÷ Equity Offered Valuation = Amount Asked ÷ Equity Offered

FAQs – Company Valuation for Startups

1. What is startup valuation and why is it important?

Startup valuation is the process of determining the economic value of a startup company. It’s crucial for fundraising, equity distribution, mergers, and strategic planning.

2. What is the best startup valuation method?

There’s no one-size-fits-all method. The best startup valuation method depends on your revenue stage, business model (SaaS, D2C, Fintech), and growth potential.

3. How to calculate startup valuation without revenue?

Pre-revenue startups can use methods like the Berkus method, Scorecard Valuation, or risk factor summation to estimate value based on qualitative metrics like team, traction, and market size.

4. How do investors value a startup in India?

Indian investors typically use a mix of comparable transactions, discounted cash flow (DCF), and traction-based valuation to determine startup worth.

5. Which valuation formula is used in Shark Tank?

Most founders on Shark Tank pitch valuations using the Post-Money Valuation Formula:

Valuation = Investment / Equity % being offered.

6. What are the common mistakes in startup valuation?

Overestimating market size (TAM), ignoring competition, lack of defensible projections, and using the wrong business valuation formula are frequent founder errors.

7. What is the difference between startup valuation and company valuation?

Startup valuation usually deals with early-stage, high-risk companies with limited revenue. Company valuation applies to businesses of any maturity and often includes traditional financials.

8. What is a good valuation for a seed-stage startup?

Seed-stage valuations vary, but in India, it often ranges between ₹3 crore and ₹15 crore, depending on team strength, market, traction, and investor appetite.

9. How does traction affect startup valuation?

High traction (e.g., user growth, revenue, retention) boosts valuation by showing real-world demand and product-market fit—even without profits.

10. What is DCF and how is it used in startup valuation?

DCF (Discounted Cash Flow) estimates a startup's value based on future cash flows, discounted to today’s value. It’s more common for revenue-generating startups.

11. What is the Scorecard Valuation Method?

The Scorecard Method evaluates a pre-revenue startup by benchmarking it against similar funded startups and scoring factors like team, product, and market.

12. How to calculate business valuation using revenue multiples?

Use the formula:

Valuation = Revenue × Industry Multiple

Example: If your D2C startup earns ₹1 crore annually and the multiple is 5×, your estimated valuation = ₹5 crore.

13. What tools or startup valuation calculators can I use?

Several online calculators (like Equidam, Startups.com, or even Excel templates) let you plug in revenue, EBITDA, and growth rates to compute valuation.

14. How does market comparables valuation work?

This method compares your startup to similar companies that have recently raised funding, then adjusts for your traction and metrics.

15. Can a startup have a high valuation with zero profits?

Yes. Many high-growth startups raise funds based on future potential, user growth, or market size rather than profitability (e.g., Meesho, Udaan).

Contact Us

An expert will call you within 24 hours. No payment required to get started.

Related Post

.png)

Why Do 9 In 10 Startups Fail in India?

Learn how from science exhibitions in schools to the hostel rooms of IITs and IIMs, each day a startup is born. Also, explore the reasons for failed startups in India.

. 5 min read.png)

Startup India Fund Scheme- How to Apply, Features, Benefits

Discover this scheme's contribution to the growth of early-stage startups through seed funding, mentoring, networking, and others.

. 3 min read.png)

4 Common Reasons Why Businesses Need to Amend Their Registered Trademark

Learn why businesses often need to make amendments to their registered trademarks. Discover the importance of trademark name search for business identity and the procedure for making changes in India.

. 5 min read