Broken Cap Table Fix for Indian Startups

By Filing Buddy . 27 Feb 26

The Structural Crisis Beneath the Funding Rebound

The Indian startup ecosystem currently stands at a pivotal inflection point. Following the harsh "funding winter" of 2022-2023, the market has demonstrated a robust resurgence, characterized by a rebound in venture capital deployment to $13.7 billion in 2024 and a maturation of exit pathways via domestic Initial Public Offerings (IPOs). However, as capital returns to the market, it is meeting a generation of startups that bear the structural scars of the volatile years that preceded this recovery. These scars are not always visible in topline revenue or user growth metrics; rather, they are embedded deep within the corporate governance architecture: the capitalization table (cap table).

A "broken" cap table, a condition in which the equity ownership structure is misaligned with the company’s future growth incentives, has emerged as a primary cause of deal failure at the Series A and Series B stages. Unlike product failures or market downturns, a broken cap table is a self-inflicted wound, often the result of early-stage negligence, predatory term sheets accepted during desperation, or the "dead equity" of departed co-founders. In the high-stakes environment of 2025-2026, where investors like Peak XV, Accel, and 3one4 Capital are scrutinizing governance hygiene with unprecedented rigor, a compromised equity structure renders a company effectively "uninvestable".

The analysis posits that cap table hygiene is no longer merely a legal housekeeping task; it is a strategic imperative. As the ecosystem moves toward a projected 2026 IPO boom, the ability to "fix" a broken cap table, navigating the "squeeze" of early investors, the tax implications of share transfers, and the psychological warfare of down-round negotiations will determine which startups survive to ring the opening bell and which remain zombies in a portfolio of dead equity.

The Anatomy of a Broken Cap Table: Diagnosis and Pathology

To fix a broken cap table, one must first understand the pathology of the breakage. In the Indian context, a cap table does not break overnight; it fractures slowly under the weight of short-term decisions made during the company’s infancy. Institutional investors typically categorize a cap table as "broken" when the equity distribution no longer supports the "alignment of interest" required to drive the company toward a 10x or 100x exit.

The "Dead Equity" Overhang

The most common and arguably most damaging form of breakage is "Dead Equity." This refers to significant ownership stakes typically ranging from 5% to 25% held by individuals or entities that are no longer actively contributing to the value creation of the enterprise.

The Departed Co-Founder Scenario

In the enthusiasm of the "zero-to-one" phase, co-founders often split equity equally (e.g., 33-33-33) without implementing robust vesting schedules. The concept of vesting earning equity over time was historically less standardized in India than in Silicon Valley, particularly in pre-2020 incorporations.

- The Problem: If one co-founder departs after 14 months to pursue a Master’s degree or a different venture, and there is no "reverse vesting" or "clawback" mechanism in the Shareholders' Agreement (SHA), they walk away with 33% of the company.

- The Investor View: A Series A investor looks at this table and sees that only 66% of the company is "working" for the future. The remaining 33% is a tax on all future growth. The active founders are effectively working one-third of their time for a passive shareholder. This creates a massive disincentive, leading investors to fear that the active founders will eventually burn out or leave to start a fresh entity where they own the majority.

The "Zombie" Advisor and Incubator

During the seed boom of 2015-2016 and again in 2021, many Indian startups traded equity for "incubation," "mentorship," or "advisory services."

- The Transaction: An advisor takes 2-5% equity for making introductions to VCs or helping with the pitch deck.

- The Reality: Three years later, the company has pivoted from B2C to B2B, the advisor is no longer relevant, but the 5% stake remains. In a ₹100 Crore valuation scenario, that advisor holds ₹5 Crore of value for work that effectively ceased years ago. This "expensive capital" crowds out the Employee Stock Option Plan (ESOP) pool and dilutes incoming investors.

The Fragmented "Party Round" Table

The democratization of angel investing in India, facilitated by platforms and syndicates, has had a double-edged effect. While it unlocked capital, it also created cap tables cluttered with 30, 40, or even 50 individual names.

- Governance Paralysis: Under the Companies Act, 2013, corporate actions such as a rights issue, a buyback, or a conversion of status (Private to Public) require shareholder resolutions. Tracking down 50 individual shareholders, some of whom may have changed addresses, died, or lost interest for wet-ink signatures, can stall a funding round for months.

- The "Retail" Holdout Risk: In a restructuring or a "down round" (where the valuation drops), rights often need to be waived. Institutional investors understand the "pay-to-play" logic: take the hit to keep the company alive. Small individual investors, operating with a retail mindset, often refuse to sign waivers, feeling "cheated" by the valuation drop. A single shareholder with 0.5% equity can sometimes hold a restructuring hostage by refusing to sign a unanimous consent document.

The Incentive Gap: Founder Dilution

This is the "mathematical breakage." A healthy cap table at Series A typically sees the founders owning 50-60%. At Series B, they should ideally retain 30-40%.

- The Indian Context: Due to the scarcity of capital in certain periods (e.g., 2016, 2022), founders often diluted too much, too early. Raising ₹2 Crore for 25% dilution at the seed stage, followed by a bridge round of ₹3 Crore for another 15%, leaves founders with <50% before they even reach institutional Series A.

- The "Uninvestable" Threshold: If a founding team owns less than 20-25% at the Series B stage, VCs view the company as uninvestable. The logic is psychological: if the company faces a crisis (which it will), a founder with only 8% equity might calculate that their "opportunity cost" is better spent elsewhere. They lack sufficient "skin in the game" to endure the grueling 7-10 year journey to an IPO.

Toxic Term Overhang: The Governance Trap

A cap table is not just a list of percentages; it is a map of legal rights. In the desperate funding environments of the past, founders often granted "super-rights" to early investors to secure capital.

- Liquidation Preferences: The standard is "1x Non-Participating Preference," meaning the investor gets their money back or their percentage share, whichever is higher. A "broken" table features Participating Preferred stock (often >1x).

The Scenario: An investor puts in ₹10 Crore for 20% with a "2x Participating Preference." In a ₹100 Crore exit, the investor first takes ₹20 Crore (2x) off the top. Then, they also take 20% of the remaining ₹80 Crore (another ₹16 Crore). Total payout: ₹36 Crore (36% of the exit for 20% ownership). The founders and employees are "squeezed" out of the proceeds.

- Veto Rights: Startups with 5-6 different investors holding veto rights over operational decisions (hiring, budget deviations, pivoting) suffer from decision paralysis. This "board overgrowth" is a major red flag for growth investors who need the CEO to have the autonomy to execute.

The Regulatory Minefield: Legal Constraints in India

Fixing a cap table in jurisdictions like Delaware is relatively straightforward due to flexible corporate laws and standardized instruments. In India, however, equity restructuring is navigating a regulatory minefield comprising the Companies Act, the Income Tax Act, and FEMA. Understanding these constraints is critical, as a "fix" that triggers a massive tax liability is no fix at all.

The Twin Tax Traps: Section 56(2)(x) and Section 50CA

The Income Tax Act, 1961 contains anti-abuse provisions designed to prevent money laundering and tax evasion through share transfers. However, these provisions act as severe friction points for legitimate startup restructuring.

Section 56(2)(x): The "Deemed Gift" Tax

This section applies to the recipient (buyer) of shares.

- The Rule: If any person receives shares for a consideration that is less than the Fair Market Value (FMV), the difference between the FMV and the actual price paid is taxed as "Income from Other Sources".

- The Startup Trap: Suppose a departed founder agrees to return his 5% stake (FMV ₹10 Crore) to the active founders for a nominal price of ₹10,000 (since he is leaving amicably).

Tax Consequence: The active founders (recipients) are deemed to have received a "gift" of ₹9.99 Crore. They will be liable to pay tax at their highest slab rate (approx. 30-35%), amounting to ~₹3-3.5 Crore in cash tax, simply for restructuring the equity.

Section 50CA: The Seller's Deemed Income

This section applies to the transferor (seller) of shares.

- The Rule: If unquoted shares are transferred at less than FMV, the FMV is deemed to be the full value of consideration for the purpose of calculating Capital Gains Tax.

- The Startup Trap: In the scenario above, the departed founder receiving only ₹10,000 will be taxed as if he received ₹10 Crore. He faces a massive tax bill on money he never received. This makes voluntary surrender of shares financially impossible for the departing party.

The Valuation Challenge (Rule 11UA)

Both sections rely on the determination of "Fair Market Value" under Rule 11UA.

- DCF Method: For startups, the Discounted Cash Flow (DCF) method is typically used. However, DCF is based on future projections. A startup fixing its cap table to raise a Series A likely has high growth projections, leading to a high FMV, which exacerbates the tax liability in any restructuring transfer.

- Angel Tax Abolition (2025 Context): While the "Angel Tax" (Section 56(2)(viib)) which taxed the company for receiving investment above FMV, has been abolished effective FY 2025-26 , the provisions of 56(2)(x) (taxing the recipient for receipt below FMV) remain fully active and are the primary blocker for cap table cleanups.

Companies Act, 2013: Procedural Rigidities

- Buyback Limitations (Section 68): A company can theoretically buy back shares to extinguish dead equity. However, buybacks are strictly limited to 25% of the aggregate of paid-up capital and free reserves.

The Trap: Most startups have accumulated losses and negligible free reserves. Therefore, they mathematically cannot perform a buyback under Section 68 to remove a significant shareholder.

- Reduction of Capital (Section 66): This is a viable but cumbersome alternative. It involves a petition to the National Company Law Tribunal (NCLT). The process takes 6-9 months and requires demonstrating that creditor interests are not prejudiced. It is a "nuclear option" for cleaning up dead equity when negotiation fails.

FEMA and Cross-Border Complexities

If the restructuring involves non-resident investors (e.g., a foreign angel or a reverse flip from a Delaware entity), the Foreign Exchange Management Act (FEMA) applies.

- Pricing Guidelines:

Resident to Non-Resident: Price cannot be less than FMV.

Non-Resident to Resident: Price cannot be more than FMV.

- Form FC-TRS: Every transfer must be reported to the RBI via Form FC-TRS within 60 days. Late filings attract compounding fees. The "pricing guidelines" effectively prevent "sweetheart deals" where foreign investors might want to exit cheaply to help the founders; the law mandates the transaction occur at fair value.

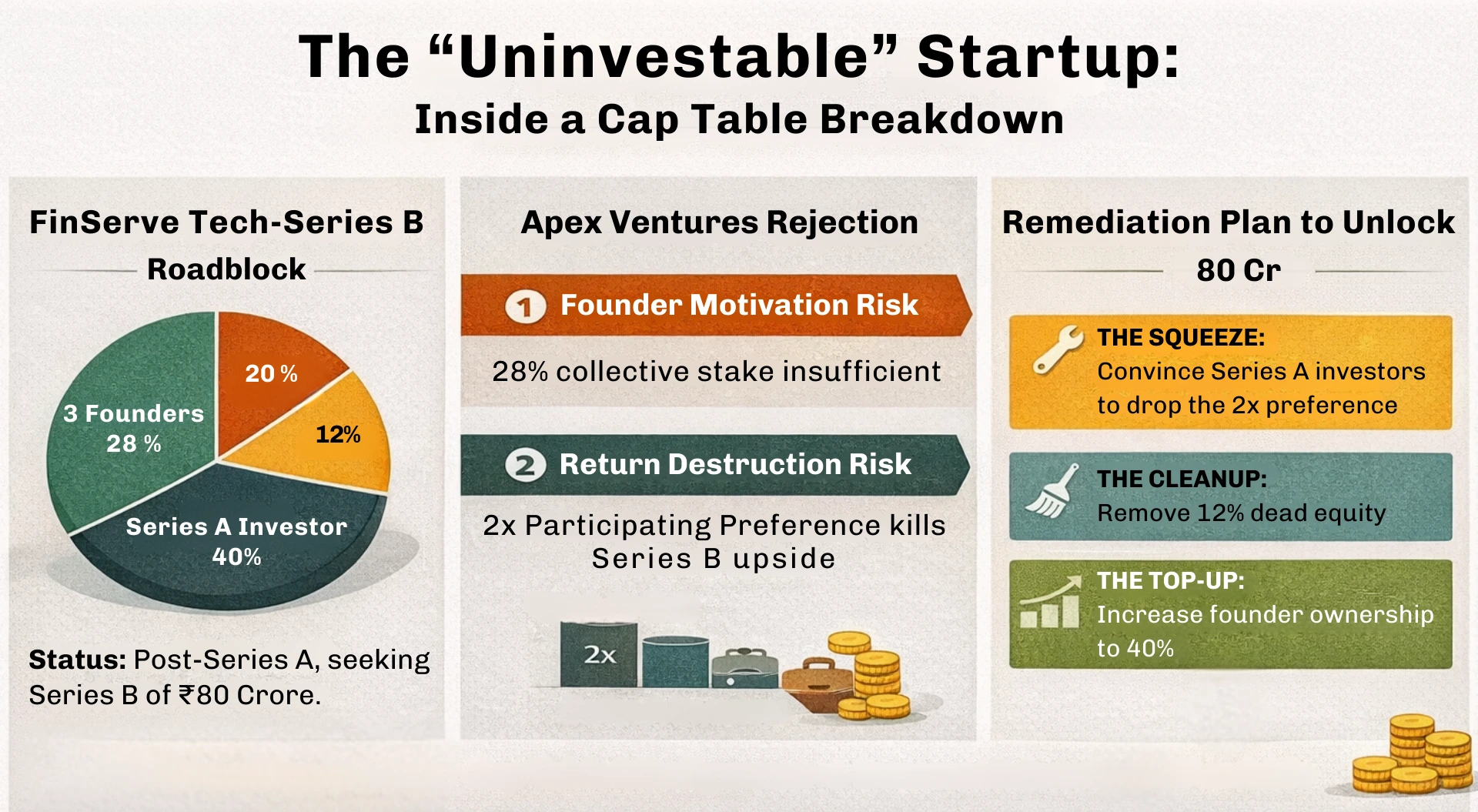

The "Uninvestable" Startup: A Composite Case Study

To illustrate the practical application of these principles, we examine a composite case study derived from common market scenarios in 2024-2025.

The Company: FinServe Tech (Anonymized), a Bangalore-based fintech infrastructure play.

Status: Post-Series A, seeking Series B of ₹80 Crore.

Revenue: ₹15 Crore ARR.

The Cap Table Crisis:

- Founders: 3 Active Founders own only 28% collectively (Severe Dilution).

- Ex-Founder: One co-founder left in 2022, holding 12% "dead equity."

- Series A Investors: Hold 40% with a 2x Participating Liquidation Preference.

- Angels: 30 small investors hold the remaining 20%.

The Rejection:

A lead growth investor, Apex Ventures, issues a term sheet with a "Condition Precedent" (CP): The cap table must be fixed. Apex argues that the founders' 28% stake is insufficient motivation, and the 2x participating preference of Series A investors destroys the return profile for incoming Series B capital. Apex designates the company "uninvestable" in its current state.

The Remediation Plan:

To unlock the ₹80 Crore funding, FinServe must execute a three-part maneuver:

- The Squeeze: Convince Series A investors to drop the 2x preference.

- The Cleanup: Remove the Ex-Founder's 12%.

- The Top-Up: Increase active founder ownership to 40%.

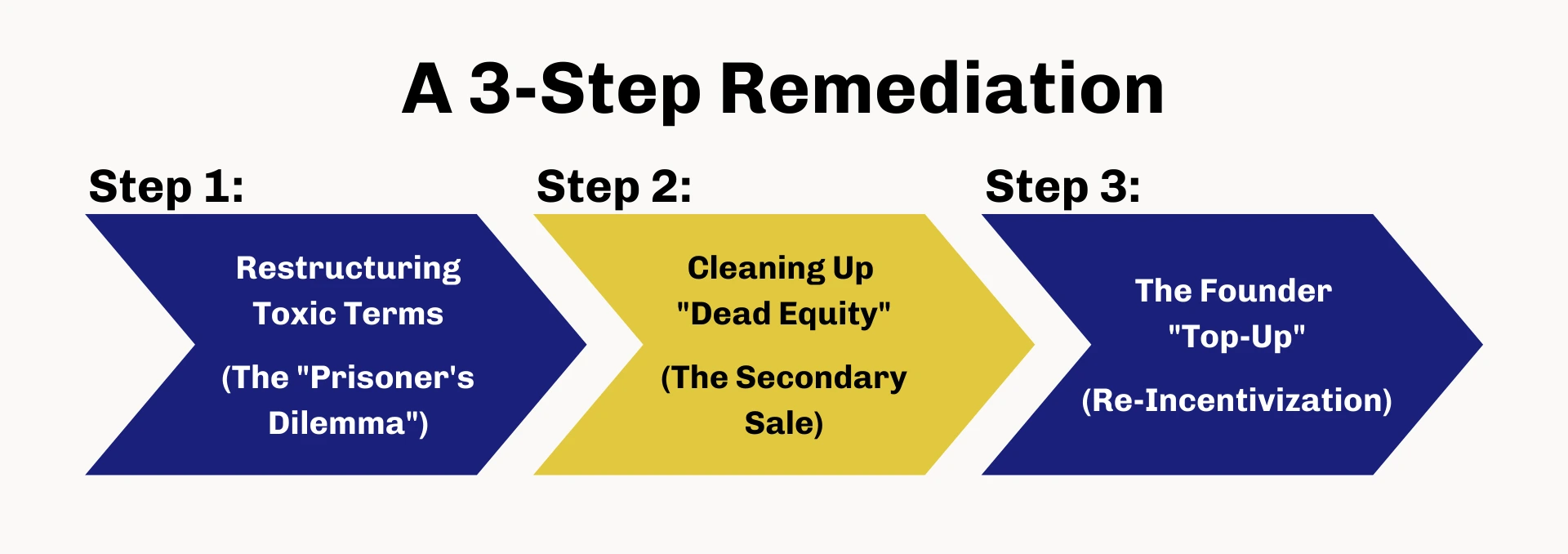

Strategic Remediation: The Mechanics of the Fix

Fixing FinServe’s cap table requires a blend of negotiation psychology, financial engineering, and legal restructuring.

Step 1: Restructuring Toxic Terms (The "Prisoner's Dilemma")

The Series A investors holding the 2x Participating Preference must be convinced to convert to standard 1x Non-Participating Preference. This is a commercial negotiation.

- The Leverage: The company is running out of runway. The founders present the Series A investors with a binary choice:

Choice A: Insist on the 2x preference. Apex Ventures walks away. The company runs out of cash. The Series A investment goes to zero.

Choice B: Waive the 2x preference. Apex invests. The company survives and grows. The Series A stake is diluted but retains potential value.

- The "Pay-to-Play" Lever: If the company’s Articles of Association (AoA) contain a "Pay-to-Play" clause, the company can force the Series A investors to participate in the new round or face conversion of their preferred stock into common stock, stripping them of their liquidation preference entirely.

- Unanimous Consent: In the absence of a "Drag Along" rights clause that forces minority investors to accept the decision of the majority, this restructuring requires unanimous consent. This is where the fragmentation of the cap table (30 angels) becomes a nightmare, as a single dissenter can block the process.

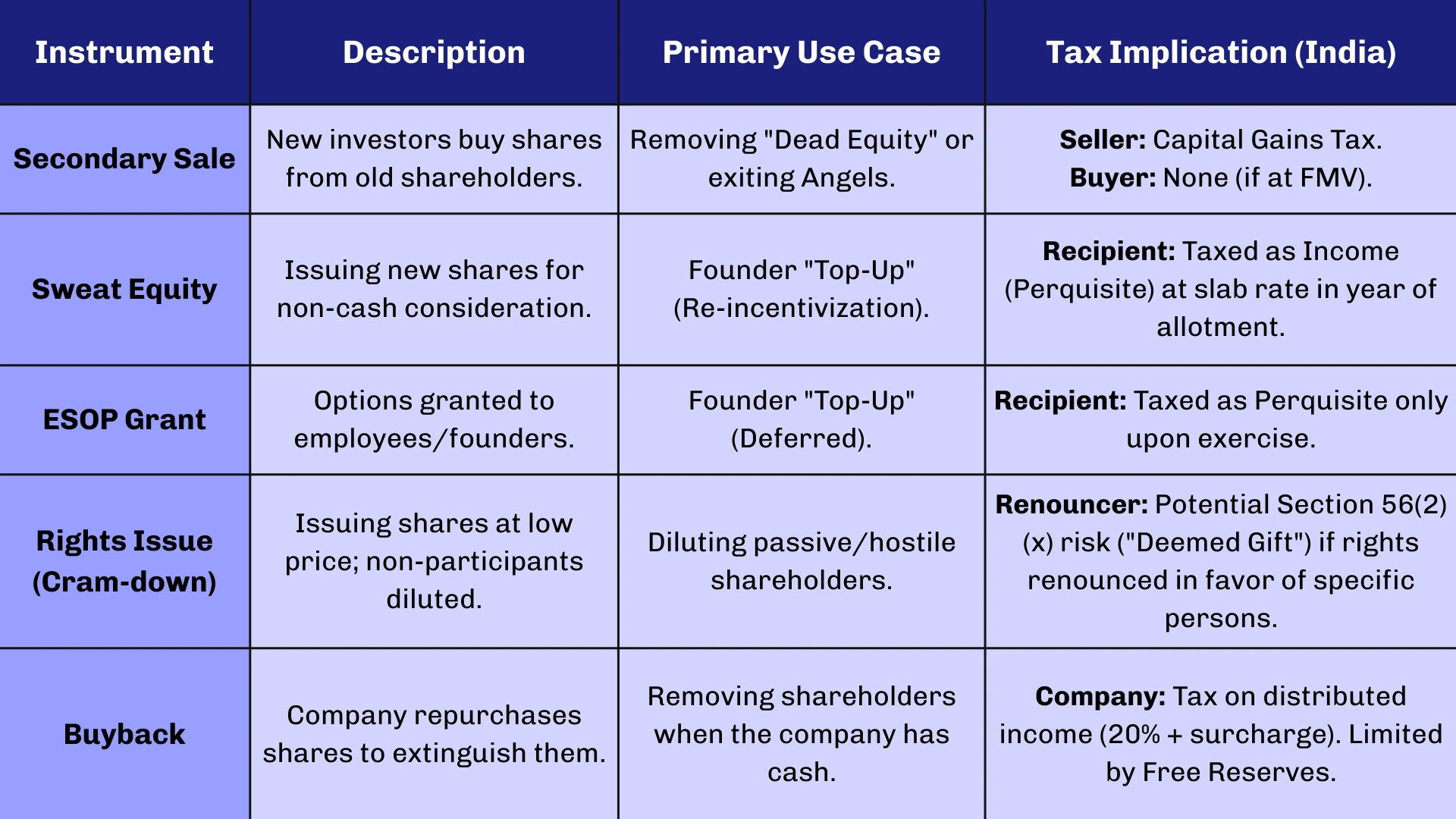

Step 2: Cleaning Up "Dead Equity" (The Secondary Sale)

The Ex-Founder holding 12% must be removed. Since a buyback is impossible due to lack of reserves, the solution is a Secondary Sale.

- The Mechanism: Apex Ventures (or a specialized Secondary Fund like Trica or Encore) agrees to purchase the 12% stake directly from the Ex-Founder.

- Pricing the Exit: To incentivize the Ex-Founder to sell, the price must be attractive enough to offer liquidity but lower than the Series B price (a "secondary discount," typically 15-20%).

- Structuring for Tax (Avoiding Section 56): The transaction happens at a negotiated price. As long as this price is above the FMV (determined by the Merchant Banker's report), the Ex-Founder pays Capital Gains Tax (12.5% LTCG or slab rate for STCG), and the buyer faces no Section 56(2)(x) liability because they are paying more than or equal to FMV, not less.

- 2025 Market Trend: Specialized "Secondary Funds" have emerged in India specifically to mop up this dead equity, acting as the "janitors" of the cap table before the primary growth investors enter.

Step 3: The Founder "Top-Up" (Re-Incentivization)

To bring the active founders from 28% to 40%, the company must issue new shares.

Option A: The ESOP Grant (Post-2025 Reform)

Historically, promoters were barred from receiving ESOPs. However, SEBI and the Companies Act have relaxed these norms for DPIIT-recognized startups (for 10 years).

- The Fix: The company expands the ESOP pool and grants massive options to the founders.

- The Cost: This dilutes all other shareholders (Series A and Angels). The investors must agree to this dilution as the "price of admission" to keep the founders motivated.

- Tax Trap: ESOPs are taxed as a "perquisite" (salary) upon exercise. If the founders exercise these options when the valuation is high, they face a crippling tax bill. They typically hold these as options and exercise only at a liquidity event (secondary sale or IPO).

Option B: Sweat Equity (Section 54)

The company issues "Sweat Equity" shares to founders for "value addition."

- Benefit: Unlike ESOPs, these are actual shares issued immediately.

- Tax Trap: The entire value of the shares (at FMV) is taxed as income in the year of allotment. Unless the founders have cash to pay 30% tax on the paper value of the shares, this option is cash-flow prohibitive.

- The "Gross-Up" Solution: In rare cases, the investor may agree to inject extra primary capital to pay a "signing bonus" to the founders, which is then used to pay the taxes on the sweat equity. This is expensive but clean.

Advanced Restructuring: The "Reverse Flip"

A specific type of cap table breakage involves geography. Many Indian startups flipped to Delaware or Singapore (2018-2021) to attract global capital. Now, looking at the robust Indian IPO market in 2025-2026, they need to come home. This is the Reverse Flip.

The Rationale

With domestic IPOs like Zomato and Swiggy demonstrating deep liquidity, and regulatory reforms (like the abolition of Angel Tax) making India attractive, the "foreign premium" has vanished. A foreign domicile is now a "governance tax" preventing a domestic listing.

The Mechanism: Inbound Merger vs. Share Swap

- Inbound Merger: The foreign holding company merges into the Indian subsidiary. The foreign shareholders receive shares of the Indian company.

NCLT Process: Requires approval from the National Company Law Tribunal. Timeframe: 9-12 months.

- Share Swap: The shareholders of the foreign entity swap their shares for shares in the Indian entity.

Tax Nightmare: This swap is a taxable transfer. The shareholders are technically "selling" their foreign shares. They may be liable for Capital Gains Tax in the foreign jurisdiction (e.g., US/Singapore) and potentially in India (under indirect transfer rules), often without receiving any cash to pay the tax.

Solution: 2024-2025 budgets have tried to make this tax-neutral for the company, but shareholder-level taxation remains a complex advisory area requiring precise valuation.

Case Studies: Lessons from the Trenches

Case Study A: The "Zombie" Seed Round (Anonymized)

Context: An EdTech startup raised a "party round" of ₹3 Crore from 45 individual angels in 2020. The Breakage: In 2024, the company needed to pivot and raise a down-round to survive. The legal requirement for the down-round was a waiver of anti-dilution rights. The Crisis: 40 of the 45 angels signed. 5 angels, holding a combined 1.5%, refused to sign, feeling the down-round was "unfair." The Fix: The company had to execute a Rights Issue at a steep discount, structured in a way that legally diluted the non-participating shareholders massively (a "cram-down"). This was legally aggressive and risked litigation (oppression and mismanagement petition under Section 241/242 of Companies Act), but the company proceeded on the advice that "survival is the best defense".

Case Study B: The Zepto-Style Cleanup (Secondary Liquidity)

Context: High-growth quick commerce player Zepto (referenced in snippets) prepared for a massive round by cleaning up its cap table. The Strategy: Before the primary IPO/Pre-IPO round, a large secondary block was executed. Early investors and potentially early employees/founders were given an exit option. The Insight: This served two purposes:

- Reward: It generated wealth for early backers, building reputation.

- Consolidation: It moved equity from disparate early investors to a single, stable institutional holder (or family offices), streamlining the cap table for the IPO prospectus (DRHP).

Future Outlook: 2026 and Beyond

As we look toward 2026, the norms for cap table hygiene are shifting from "remedial" to "preventative."

The "Governance Audit" Standard

Startups heading for IPOs in 2026 are now subjected to "Governance Audits" by merchant bankers 18-24 months prior to listing. These audits explicitly flag "related party" equity and "dead equity" as material risks. The "fix" is no longer optional; it is a listing requirement.

The Rise of the "Founder-Friendly" Secondary

With the deepening of the Indian venture secondary market (estimated at >$100M in annual volume), we are seeing the emergence of funds whose primary thesis is "Cap Table Recapitalization." These funds partner with founders to buy out "nuisance" shareholders, effectively serving as white knights.

Post-Abolition of Angel Tax

The abolition of the Angel Tax has removed the "Sword of Damocles" from domestic capital raises. This allows founders to execute "internal bridge rounds" or "cleanup rounds" at flat valuations without the fear of receiving an Income Tax notice for raising money above FMV.

Conclusion

A cap table is the DNA of a startup. When it is mutated by dead equity, toxic terms, or fragmentation, the organism cannot grow. The Indian startup ecosystem has matured to a point where "growth at all costs" has been replaced by "growth with governance."

Fixing a broken cap table is a painful, expensive, and emotionally draining process. It involves difficult conversations with former friends (departed founders), aggressive negotiations with early backers (the "squeeze"), and navigating a labyrinth of tax laws that seem designed to punish restructuring. Yet, it is a necessary rite of passage for any company aspiring to the public markets.

The "uninvestable" label is not permanent. As demonstrated by the mechanisms of secondary transfers, recapitalizations, and legal restructuring, a broken cap table can be fixed. But the window for doing so is finite. In the 2025-2026 funding cycle, the founders who proactively clean their house, consolidating ownership, aligning incentives, and simplifying governance will be the ones who secure the capital to build India's next generation of generational companies.

Appendix: Comparison of Remediation Instruments

FAQs: Fixing a Broken Cap Table in Indian Startups

1. What is a broken cap table in a startup?

A broken cap table is an equity structure that discourages investors due to excessive dilution, dead equity, related-party holdings, or poor governance. It signals funding risk and future control issues.

2. Why do VCs reject startups because of cap table issues?

VCs reject startups when founders hold too little equity, inactive shareholders own large stakes, or governance risks exist. It reduces founder incentive and complicates future funding rounds.

3. What is dead equity in startups?

Dead equity refers to shares held by inactive founders, early advisors, or disengaged investors who no longer contribute but still retain ownership.

4. How much founder dilution is too much before Series A?

If founders collectively hold below 50–60% before Series A, investors may see misaligned incentives. Excessive early dilution signals poor capital strategy.

5. How can founders fix a broken cap table?

Founders can restructure through buybacks, secondary sales, ESOP realignment, share transfers, or recapitalization before major funding rounds.

6. What is cap table recapitalization?

Cap table recapitalization involves restructuring shareholding to clean up dead equity, rebalance ownership, and improve investor readiness.

7. What is a founder-friendly secondary round?

It’s when secondary investors buy shares from inactive or nuisance shareholders, helping founders clean up the cap table without new dilution.

8. What are governance audits before IPO?

Governance audits are pre-IPO reviews by merchant bankers that assess shareholder structure, related-party equity, and compliance risks.

9. Can Section 56(2)(x) apply to share transfers?

Yes. If shares are transferred below fair market value, the difference may be taxed in the hands of the recipient under Section 56.

10. How did the abolition of Angel Tax help startups?

It removed tax scrutiny on premium share issuances, allowing bridge or cleanup rounds at fair valuations without fear of income tax notices.

11. What is a reverse flip in startups?

A reverse flip is when an overseas holding structure is shifted back to India, often requiring cap table cleanup and regulatory alignment.

12. Why is cap table hygiene important before fundraising?

Investors conduct due diligence. A messy cap table delays deals, reduces valuation leverage, and increases legal complexity.

13. How does ESOP mismanagement affect cap tables?

Over-allocated or improperly structured ESOP pools can cause unexpected dilution and create investor concerns during funding rounds.

14. When should startups clean up their cap table?

Ideally 12–18 months before a major funding round or IPO, not during due diligence.

15. Can inactive shareholders block fundraising?

Yes. Minority shareholders with special rights or voting power can delay approvals and complicate deal execution.

Contact Us

An expert will call you within 24 hours. No payment required to get started.

Related Post

.png)

Why Do 9 In 10 Startups Fail in India?

Learn how from science exhibitions in schools to the hostel rooms of IITs and IIMs, each day a startup is born. Also, explore the reasons for failed startups in India.

. 5 min read.png)

Startup India Fund Scheme- How to Apply, Features, Benefits

Discover this scheme's contribution to the growth of early-stage startups through seed funding, mentoring, networking, and others.

. 3 min read.png)

4 Common Reasons Why Businesses Need to Amend Their Registered Trademark

Learn why businesses often need to make amendments to their registered trademarks. Discover the importance of trademark name search for business identity and the procedure for making changes in India.

. 5 min read