Loan Confirmations in Audit: Process, Risks & Checklist

By Filing Buddy . 06 Mar 26

The Audit Paper Trail Every Finance Team Must Get Right

In the world of statutory audits, few documents are as deceptively simple and as critically important as the loan confirmation. A single-page balance confirmation letter can determine whether a company’s borrowings are fairly presented, whether interest expenses are accurate, and whether financial statements can be relied upon by lenders, investors, and regulators.

Whether your auditor is from a Big Four firm like Deloitte or a mid-sized practice such as BDO, loan confirmations are a standard and essential part of the audit process. Yet many finance teams treat them as routine paperwork until a discrepancy surfaces.

This comprehensive guide explains:

- What loan confirmations are

- Why auditors insist on them

- What details must be included

- Common errors and risks

- Best practices for finance teams

- Practical email templates you can use

If your organization has bank borrowings, director loans, NBFC funding, intercompany loans, or external debt, this guide will help you strengthen your audit trail.

What Is a Loan Confirmation?

A loan confirmation is a written statement from a lender confirming the outstanding balance and key terms of a loan as of a specific date, usually the financial year-end.

It is obtained directly from:

- Banks

- Financial institutions

- NBFCs

- Group companies

- Directors or related parties

- Private lenders

From an audit perspective, it is third-party evidence, which carries higher reliability than internal records.

Why Are Loan Confirmations So Important in an Audit?

A. Independent Verification of Liability

Management may report a loan balance of 2,500,000 in the trial balance. But auditors cannot rely solely on internal records. They need confirmation from the lender that:

- The loan exists

- The amount is accurate

- The terms are correctly recorded

B. Validation of Interest and Accruals

Confirmations help auditors verify:

- Interest rate

- Interest accrued but not paid

- Penal interest (if any)

- Processing fees or charges

Even small errors in interest calculation can materially affect financial statements.

C. Identification of Unrecorded Liabilities

Sometimes:

- Additional facilities are sanctioned but not recorded

- Guarantees are outstanding

- Letters of credit or overdrafts exist but are not properly disclosed

D. Fraud Prevention

In rare but serious cases, companies have misrepresented debt levels. Independent confirmations reduce the risk of financial misstatement.

What Information Should a Loan Confirmation Include?

A properly drafted loan confirmation should contain:

- Borrower name

- Loan account number

- Sanctioned limit

- Outstanding principal as of year-end

- Interest rate

- Interest accrued but unpaid

- Security details

- Repayment schedule

- Penal charges (if applicable)

- Confirmation signature and stamp

Types of Loan Confirmations

1. Bank Loan Confirmation

This is the most common type. It includes:

- Term loans

- Cash credit facilities

- Overdrafts

- Working capital loans

- Bank guarantees

Banks usually provide confirmations on official letterhead.

2. NBFC Loan Confirmation

NBFC confirmations may sometimes lack detailed breakdowns. Finance teams should request:

- Principal vs interest split

- Late payment charges

- Processing fee adjustments

3. Director / Related Party Loan Confirmation

These are particularly sensitive from a governance perspective. Confirmations must specify:

- Whether the loan is interest-bearing

- Repayment terms

- Whether it is secured or unsecured

Auditors scrutinize related-party transactions.

4. Intercompany Loan Confirmation

Group companies must reconcile balances mutually. Differences often arise due to:

- Timing mismatches

- Unrecorded interest

- Currency translation differences

Mutual confirmation avoids consolidation issues.

The Standard Audit Process for Loan Confirmations

Audit firms, whether global networks like PricewaterhouseCoopers or national practices, generally follow a structured confirmation process:

- Management prepares a list of all loans

- Auditor drafts confirmation requests

- Requests are sent directly to lenders

- Responses are received independently

- Differences are reconciled

In some cases, auditors use digital confirmation platforms. However, traditional email confirmations remain common in many jurisdictions.

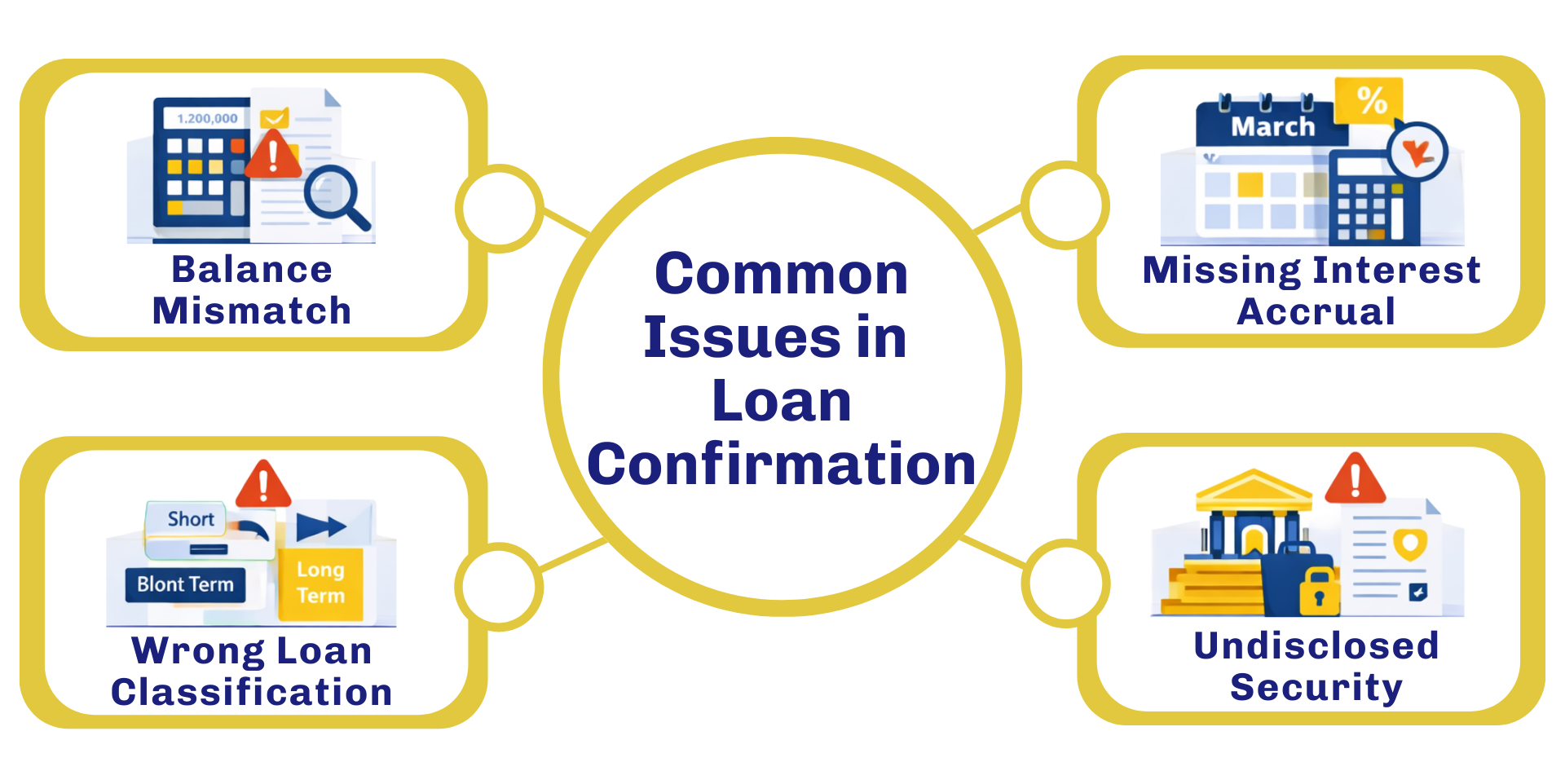

Common Issues in Loan Confirmations

Issue 1: Balance Mismatch

Company books show: 1,200,000

Bank confirms: 1,235,000

Possible reasons:

- Unrecorded interest

Bank charges are not accounted

Wrong cutoff date

Issue 2: Accrued Interest Missing

Companies sometimes forget to accrue interest for March. Confirmations quickly expose this error.

Issue 3: Incorrect Classification

A short-term loan may be wrongly classified as long-term. Confirmation of repayment schedule helps correct this.

Issue 4: Security Not Disclosed

Auditors must ensure assets pledged as collateral are disclosed in notes to accounts.

Best Practices for Finance Teams

1. Maintain a Loan Register

Keep a centralized tracker containing:

- Lender name

- Loan number

- Sanction date

- Interest rate

- EMI schedule

- Outstanding balance

- Security pledged

This reduces last-minute audit stress.

2. Perform Year-End Reconciliation Before Audit

Don’t wait for the auditor to detect mismatches. Reconcile:

- Principal balance

- Interest accrual

- Charges

- TDS (if applicable)

3. Send Confirmation Requests Early

Banks may take time to respond. Send requests at least:

- 3–4 weeks before audit deadline

4. Keep Written Evidence

Maintain:

- Email trails

- Signed letters

- Follow-up reminders

These form part of your audit documentation.

Digital Confirmations: The Evolving Landscape

With increased digitization, many firms now use secure confirmation portals. Some large audit networks like Ernst & Young encourage electronic confirmations for efficiency and security.

Benefits include:

- Reduced fraud risk

- Faster turnaround

- Audit trail tracking

- Direct third-party authentication

However, smaller organizations still rely heavily on email-based confirmations.

Internal Controls Around Borrowings

Loan confirmations are not just an audit requirement; they are a reflection of internal control quality.

Strong internal controls include:

- Proper authorization of borrowings

- Board approval documentation

- Clear segregation of duties

- Regular interest reconciliation

- Monitoring of covenant compliance

Poor controls often lead to audit qualifications.

Red Flags Auditors Watch For

Auditors are trained to identify unusual indicators such as:

- Frequent loan rollovers

- High related-party borrowings

- Negative cash flows despite high borrowings

- Unusually low interest expense

- Undisclosed guarantees

A properly obtained confirmation either validates or challenges these concerns.

How Loan Confirmations Impact Financial Statement Disclosures

Loan confirmations support:

- Borrowings note disclosures

- Current vs non-current classification

- Interest expense reporting

- Related-party disclosures

- Contingent liability disclosures

Errors in confirmations can impact debt ratios, covenant calculations, and investor confidence.

How to Handle Differences in Confirmations

If a discrepancy arises:

- Compare bank statement with ledger

- Check interest recalculation

- Review charges debited after cutoff

- Pass necessary journal entries

- Document reconciliation

Never ignore small differences; they accumulate.

The Bigger Picture: Transparency and Trust

At its core, loan confirmation is about credibility.

Lenders trust audited financial statements. Investors rely on debt disclosures. Regulators expect transparency. A single missing confirmation can delay audit sign-off and create unnecessary risk.

Firms like KPMG emphasize third-party confirmations because they strengthen the reliability of reported numbers.

When handled properly, loan confirmations:

- Reduce audit queries

- Prevent misstatements

- Improve governance

- Strengthen financial integrity

Final Checklist for Finance Teams

Before audit closure, confirm:

- All loans identified

- Confirmation requests sent

- Responses received directly

- Differences reconciled

- Interest properly accrued

- Disclosures aligned with confirmations

- Documentation filed

If you can confidently check all boxes, your audit paper trail is strong.

Conclusion

Loan confirmations may appear routine, but they form one of the most powerful pillars of audit evidence. They validate the existence, accuracy, and completeness of borrowings, one of the most material line items in financial statements.

For finance teams, mastering the loan confirmation process means fewer audit delays, stronger internal controls, and better stakeholder confidence.

Use the templates above, maintain proactive communication with lenders, and treat confirmations not as a compliance formality, but as a critical element of financial discipline.

FAQs: Loan Confirmations in Audit

1. What is a loan confirmation in auditing?

A loan confirmation is a written statement from a lender verifying the outstanding loan balance and terms as of a specific date. Auditors obtain it directly from banks, NBFCs, or lenders to independently confirm liabilities recorded in a company’s financial statements.

2. Why do auditors require loan confirmations?

Auditors use loan confirmations to independently verify borrowings. They confirm loan balances, interest terms, repayment schedules, and other conditions directly with lenders, ensuring that liabilities reported in financial statements are accurate and complete.

3. Who provides a loan confirmation during an audit?

Loan confirmations are typically issued by lenders such as banks, NBFCs, financial institutions, group companies, directors, related parties, or private lenders who have provided funding to the company.

4. What information is included in a loan confirmation letter?

A loan confirmation usually includes the borrower name, loan account number, sanctioned limit, outstanding principal, interest rate, accrued interest, repayment schedule, security details, and the lender’s authorized signature.

5. When are loan confirmations usually obtained?

Loan confirmations are usually obtained at the end of the financial year during statutory audits. They confirm the loan balance and terms as of the reporting date used in the financial statements.

6. What happens if loan confirmation balances do not match company records?

If balances differ, auditors investigate the cause. Common reasons include unrecorded interest, bank charges, incorrect cutoff dates, or posting errors. Finance teams must reconcile the difference and pass necessary journal entries.

7. Are loan confirmations mandatory for audits?

While not always legally mandatory, loan confirmations are considered a standard audit procedure under auditing standards. They provide reliable third-party evidence that strengthens the credibility of financial statements.

8. What types of loans require confirmation in an audit?

Auditors typically obtain confirmations for bank loans, NBFC borrowings, director or related-party loans, intercompany loans, and other external borrowings recorded in the company’s books.

9. How do auditors send loan confirmation requests?

Auditors usually prepare confirmation requests and send them directly to lenders through email, physical letters, or digital confirmation platforms. Responses are received independently to ensure reliability.

10. Can loan confirmations be obtained electronically?

Yes. Many audit firms now use secure digital confirmation platforms. Electronic confirmations improve efficiency, reduce fraud risk, and provide better audit trail tracking compared to traditional paper confirmations.

11. Why are loan confirmations considered strong audit evidence?

Loan confirmations are obtained from independent third parties. Because they come directly from lenders rather than company records, auditors consider them highly reliable evidence when verifying borrowings.

12. What risks can loan confirmations reveal?

Loan confirmations can reveal balance mismatches, missing interest accruals, undisclosed collateral, incorrect loan classification, and unrecorded liabilities that may impact financial statement accuracy.

13. How should finance teams prepare for loan confirmations?

Finance teams should maintain a loan register, reconcile balances before the audit, calculate interest accruals accurately, and send confirmation requests early to ensure timely responses from lenders.

14. What is the difference between a loan confirmation and a bank balance confirmation?

A loan confirmation verifies borrowing balances and loan terms with a lender. A bank balance confirmation verifies cash balances held with a bank. Both are independent confirmations used as audit evidence.

15. What should companies do if a lender does not respond to confirmation requests?

If no response is received, auditors may perform alternative procedures such as reviewing loan agreements, bank statements, repayment schedules, and interest calculations to verify the loan balance.

Contact Us

An expert will call you within 24 hours. No payment required to get started.

Related Post

LLP vs. LLC: Choosing the Right Structure for Your Business

Making the appropriate legal structure choice is one of the most important decisions you'll need to make when launching a business in India. Limited Liability Companies (LLCs) and Limited Liability Partnerships (LLPs) are two well-liked alternatives.

. 3 min read2.png)

LLP Agreements: Creating a Solid Foundation for Your Business

A Limited Liability Partnership (LLP) is a business structure that combines the benefits of a partnership with limited liability protection, typically associated with corporations. It is designed to provide a more flexible and tax-efficient framework for professionals and businesses with multiple partners.

. 3 min read.png)

Revised LLP (Amendment) Rules for 2023 – Enhanced LLP Form No. 3

The Ministry of Corporate Affairs (MCA) has recently issued the Limited Liability Partnership (LLP) (Amendment) Rules, 2023, which were officially gazetted on June 2, 2023. These rules bring about amendments to the pre-existing Limited Liability Partnership Rules of 2009. These amendments came into effect upon their publication in the Official Gazette. A noteworthy change introduced through these amendments is the revision of the LLP Form No.3, which pertains to "Information concerning Limited Liability Partnership Agreement."

. 3 min read