What is an Amortization Schedule? | Loan & Mortgage Example, Formula & Table

What is an Amortization Schedule?

An amortization schedule is a structured table that outlines the details of each loan repayment over the term of a loan or the useful life of an intangible asset. It breaks down every instalment into two parts: interest paid and principal repaid, giving you a transparent view of how your debt decreases over time.

Loan Amortization Schedule

A loan amortization schedule provides a systematic breakdown of loan repayments. It shows how each monthly payment is divided between principal and interest and how the loan balance reduces over time. This helps borrowers clearly understand how their debt is repaid and how much interest they’re actually paying.

Amortization Schedule for a Mortgage

In the case of mortgages, an amortization schedule for mortgages works the same way but is tailored for long-term real estate loans. Mortgage amortization schedules are typically stretched across 15 to 30 years, and early payments consist largely of interest, with principal repayment increasing over time.

Amortization Schedule Formula

To calculate the monthly payments or principal and interest breakup, you can use:

1. Principal Payment Formula:

Principal Payment = TMP - (OLB × Interest Rate / 12)

Where:

- TMP = Total Monthly Payment

- OLB = Outstanding Loan Balance

2. Monthly Payment Calculation Formula:

TMP = Loan Amount × [i × (1+i)^n / ((1+i)^n - 1)]

Where:

- i = Monthly interest rate

- n = Total number of payments

Amortization Schedule Table

The amortization schedule table typically includes:

- Payment Number

- Payment Date

- Beginning Balance

- Monthly Payment

- Interest Paid

- Principal Paid

- Ending Balance

This schedule is an essential financial planning tool, helping borrowers understand how their loans are repaid over time.

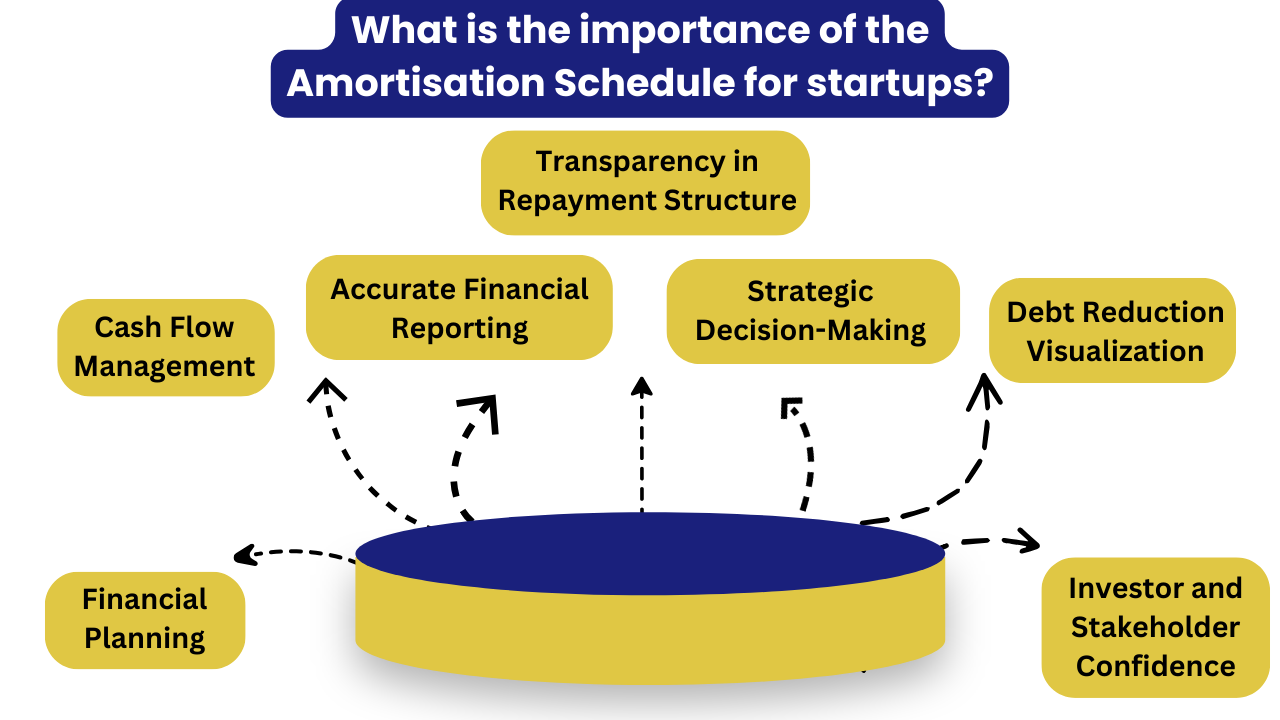

What is the importance of the Amortization Schedule for startups?

1. Financial Planning:

Amortization schedules help startups plan their financial commitments by outlining the scheduled repayment of loans or amortizable assets, allowing for better budgeting.

2. Cash Flow Management:

Understanding the timing and amounts of amortization payments assists startups in managing their cash flow effectively, preventing potential liquidity issues.

3. Transparency in Repayment Structure:

Amortization schedules provide a transparent breakdown of each payment, illustrating the proportion allocated to interest and principal aiding in clear financial communication.

4. Accurate Financial Reporting:

Utilising amortization schedules ensures accurate and compliant financial reporting, reflecting the actual cost distribution of assets or loans over time.

5. Strategic Decision-Making:

Based on the insights gained from amortization schedules, startups can make informed decisions about loans and asset investments, considering the impact on long-term finances.

6. Debt Reduction Visualization:

The schedule visually represents the debt reduction over time, allowing startups to track progress and celebrate milestones in becoming debt-free.

7. Investor and Stakeholder Confidence:

Transparent and well-managed amortization schedules instill confidence in investors and stakeholders, showcasing the startup's commitment to sound financial practices and repayment plans.

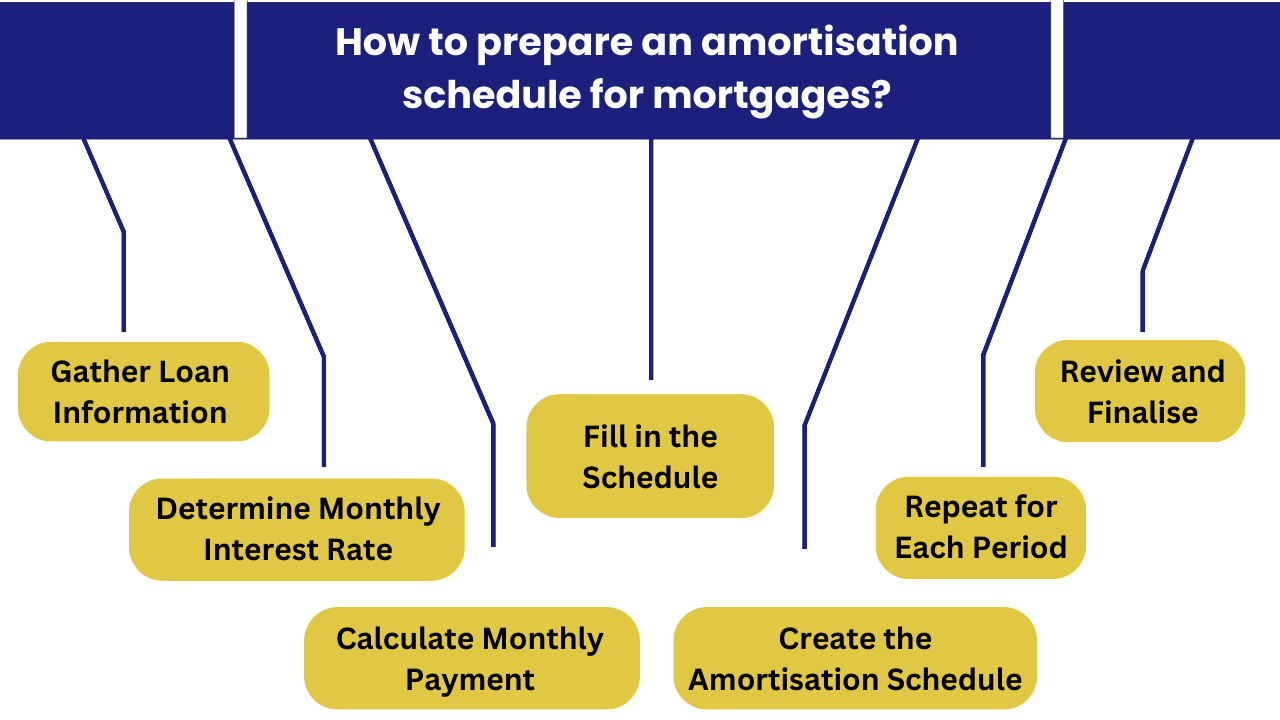

How to prepare an amortization schedule for mortgages?

This is how you can prepare amortization schedule for mortgages:

- Gather Loan Information:

Collect essential details about the mortgage, including the loan amount, interest rate, loan term (in years), and the start date of the mortgage.

- Determine Monthly Interest Rate:

Divide the annual interest rate by 12 to get the monthly interest rate. For example, if the annual rate is 5%, the monthly rate would be 0.05 / 12.

- Calculate Monthly Payment:

Use the loan amount, monthly interest rate, and loan term to calculate the fixed monthly payment using the formula for an amortizing loan. The formula is typically.

Monthly Payment=P × [(1+i)^n / (1+i)^n-1]

Where:

P = Loan amount (principal)

i = Monthly interest rate (Annual interest rate ÷ 12)

n = Total number of payments (Loan term in years × 12)

- Create the Amortization Schedule:

Set up a table with columns for Payment Number, Payment Date, Beginning Balance, Monthly Payment, Interest Paid, Principal Paid, and Ending Balance.

- Fill in the Schedule:

Begin with the first payment. For each subsequent row, calculate the interest paid and principal paid using the formulas:

- Interest Paid = Beginning Balance * Monthly Interest Rate

- Principal Paid = Monthly Payment - Interest Paid

- Ending Balance = Beginning Balance - Principal Paid

- Repeat for Each Period:

Repeat these calculations for each period, updating the Beginning Balance, Interest Paid, Principal Paid, and Ending Balance columns. Continue until the Ending Balance reaches zero.

- Review and Finalise:

Check the amortization schedule for accuracy, ensuring that the sum of principal and interest payments equals the monthly payment. This schedule is a roadmap for understanding how each payment contributes to the loan's repayment.

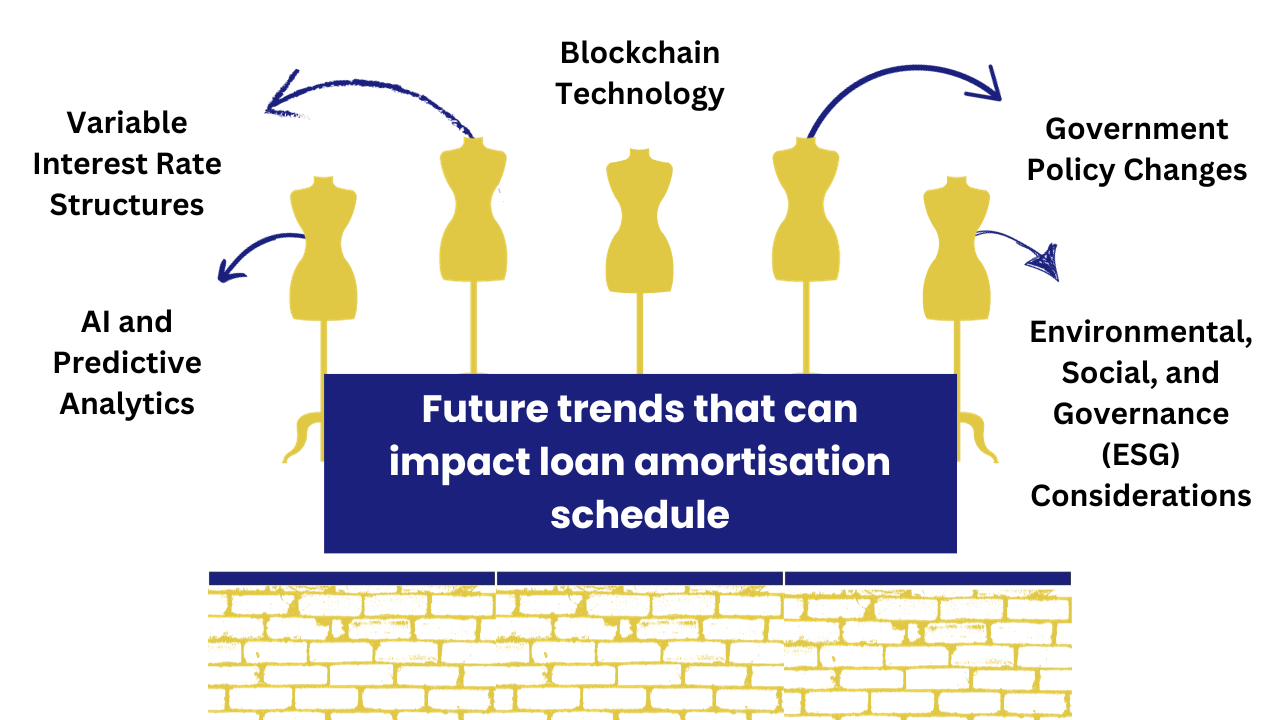

Future trends that can impact loan amortization schedule

Some of the trends that can impact loan amortization schedule:

Blockchain Technology:

Adopting blockchain technology in the financial sector may impact loan amortization schedules by introducing transparent and secure methods for recording and managing financial transactions. Smart contracts powered by blockchain could automate and enhance the efficiency of loan payment schedules.

Variable Interest Rate Structures:

With ongoing changes in global economic conditions, future trends may see an increase in variable interest rate structures. This could lead to more dynamic and complex loan amortization schedules, requiring borrowers to adapt to fluctuating interest rates.

AI and Predictive Analytics:

Integrating artificial intelligence (AI) and predictive analytics into financial systems may influence loan amortization schedules. Advanced algorithms could analyse borrower behaviour and market trends, leading to more personalised and predictive adjustments to repayment schedules.

Environmental, Social, and Governance (ESG) Considerations:

The growing emphasis on ESG factors may impact loan structures and, consequently, amortization schedules. Lenders may incorporate sustainability criteria into loan agreements, influencing the terms and conditions and affecting repayment schedules based on environmental and social performance.

Government Policy Changes:

Changes in government policies, especially related to economic stimulus, interest rates, or financial regulations, can significantly impact loan amortization schedules. Future trends in policy-making could introduce new variables affecting the timing and structure of loan repayments.

Example

Let's consider an example of a mortgage amortization schedule for a $200,000 loan with a 4% annual interest rate and a 30-year term. Here is a simplified version:

Loan Information:

- Loan Amount: $200,000

- Annual Interest Rate: 4%

- Loan Term: 30 years

Calculate Monthly Interest Rate:

4%X12=0.00333

Monthly Interest Rate=12X4%=0.00333

Calculate Monthly Payment:

Using the formula PMT=(1+r)n−1P⋅r⋅(1+r)n:

200,000⋅0.00333⋅(1+0.00333)360(1+0.00333)360−1MonthlyPayment=(1+0.00333)360−1200,000⋅0.00333⋅(1+0.00333)360

The calculated monthly payment is approximately $954.83.

Create Amortization Schedule:

| Payment Number | Payment Date | Beginning Balance | Monthly Payment | Interest Paid | Principal Paid | Ending Balance |

| 1 | 01/01/2023 | $200,000 | $954.83 | $666.67 | $288.16 | $199,711.84 |

| 2 | 01/02/2023 | $199,711.84 | $954.83 | $665.04 | $289.79 | $199,422.05 |

| ... | ... | ... | ... | ... | ... | ... |

| 360 | 01/12/2052 | $955.12 | $954.83 | $3.98 | $950.85 | $4.26 |

| 361 | 01/01/2053 | $4.26 | $954.83 | $0.02 | $954.81 | $0.45 |

FAQ

Q1. What is an amortization schedule?

An amortization schedule is a table that shows the breakdown of each loan payment into interest and principal over the loan term.

Q2. Why is an amortization schedule important?

It helps borrowers understand how their payments are applied and how the loan balance reduces over time, aiding in budgeting and financial planning.

Q3. How is the interest calculated in an amortization schedule?

Interest is typically calculated on the outstanding loan balance using the monthly interest rate derived from the annual rate.

Q4. Do all loans follow an amortization schedule?

No, only amortizing loans like mortgages, auto loans, and personal loans follow a fixed repayment schedule. Credit cards and interest-only loans may not.

Q5. Can I create my own amortization schedule?

Yes, you can use spreadsheet tools like Excel or online calculators by inputting your loan amount, interest rate, and loan term.

Q6. How does early repayment affect the amortization schedule?

Early payments reduce the principal faster, saving you interest and shortening the loan term, but they may come with prepayment penalties in some cases.

Q7. What happens if interest rates change in a variable-rate loan?

For variable-rate loans, the amortization schedule adjusts based on new rates, leading to fluctuating monthly payments and interest amounts.

Q8. How does an amortization schedule benefit startups?

It aids in financial forecasting, cash flow management, and demonstrates repayment clarity to investors and stakeholders.

Why choose Us?

Filing Buddy is an entity which is focused at providing legal, financial, and corporate and compliances consultancy services to business entities. Our organisation is a structure made of enthusiastics.

EXPERTISE & RELIABILITY

Trusted industry professionals ensuring compliance, accurate tax filing, and comprehensive services for your business needs.

TAILORED SOLUTIONS

Customized services to meet your specific requirements, including business incorporation, trademarks, patents, and seamless GST return filing.

TIMELY SUPPORT

Dedicated support team committed to providing prompt assistance, resolving queries, and ensuring smooth operations for your business.

COMPETITIVE ADVANTAGE

Gain a competitive edge with our comprehensive suite of services, enabling you to focus on growth while we handle your compliance and taxation needs.

.webp)

.webp)

.webp)