Commercial Bank: Definition, Functions, and Services Explained

Definition

A commercial bank is a financial institution that provides services like loans, certificates of deposit, savings bank accounts, bank overdrafts, and so on to its customers.

Description

Commercial banks offer these services to individuals and corporations. Commercial banks make money by offering and earning interest on loans such as mortgages, auto loans, business loans, and personal loans. Customer deposits give banks the necessary funds to issue these loans.

Commercial banks were typically based in physical premises, but an increasing number now operate entirely online.

Commercial banks are vital to the economy because they provide capital, credit, and liquidity to the market.

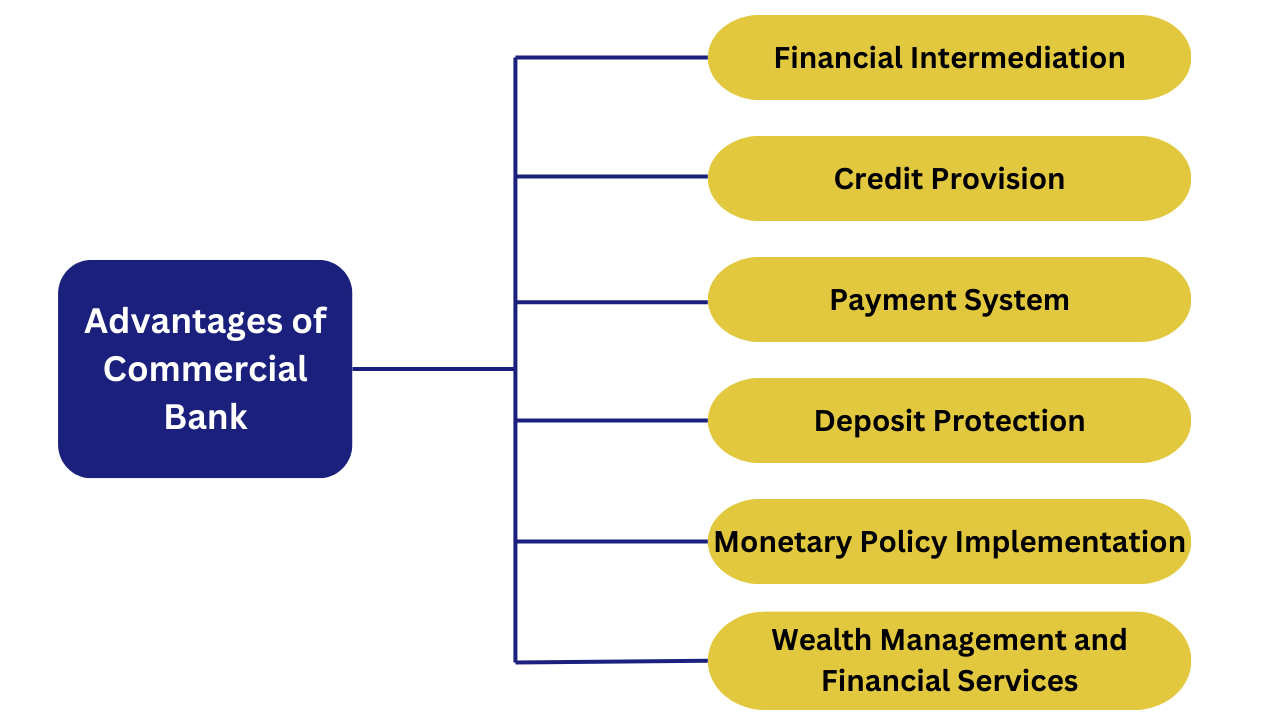

Advantages of Commercial Bank for startups

Commercial banks play an important role in the economy, acting as a key component of the financial system. Their significance can be summarised through numerous critical functions:

- Financial Intermediation: Commercial banks serve as mediators between depositors who lend money to the bank and borrowers seeking loans. This function is critical for the efficient allocation of resources in an economy, allowing savings to be transferred from savers to borrowers, who can then employ the funds for productive purposes.

- Credit Provision: Banks provide critical credit to individuals, corporations, and governments, facilitating everything from consumer purchases such as homes and automobiles to business expansion and infrastructure development. This credit is critical to economic growth and development.

- Payment System: Commercial banks provide the systems required to perform financial transactions, such as trade settlement, checking account management, and wire transfer services. These services guarantee the smooth operation of both domestic and international trade.

- Deposit Protection: Banks provide a secure environment for people and businesses to deposit money. By assuring the safety of these funds, banks protect wealth and make it available for lending to other clients, thereby assisting in the economy's liquidity management.

- Monetary Policy Implementation: Commercial banks play an important role in executing central banks' monetary policies. Interest rate modifications intended to control inflation or stimulate economic growth are frequently implemented through commercial banks.

- Wealth Management and Financial Services: In addition to providing necessary banking services, commercial banks offer a variety of financial services such as wealth management, financial advice, and planning to assist individuals and businesses in managing their financial destiny.

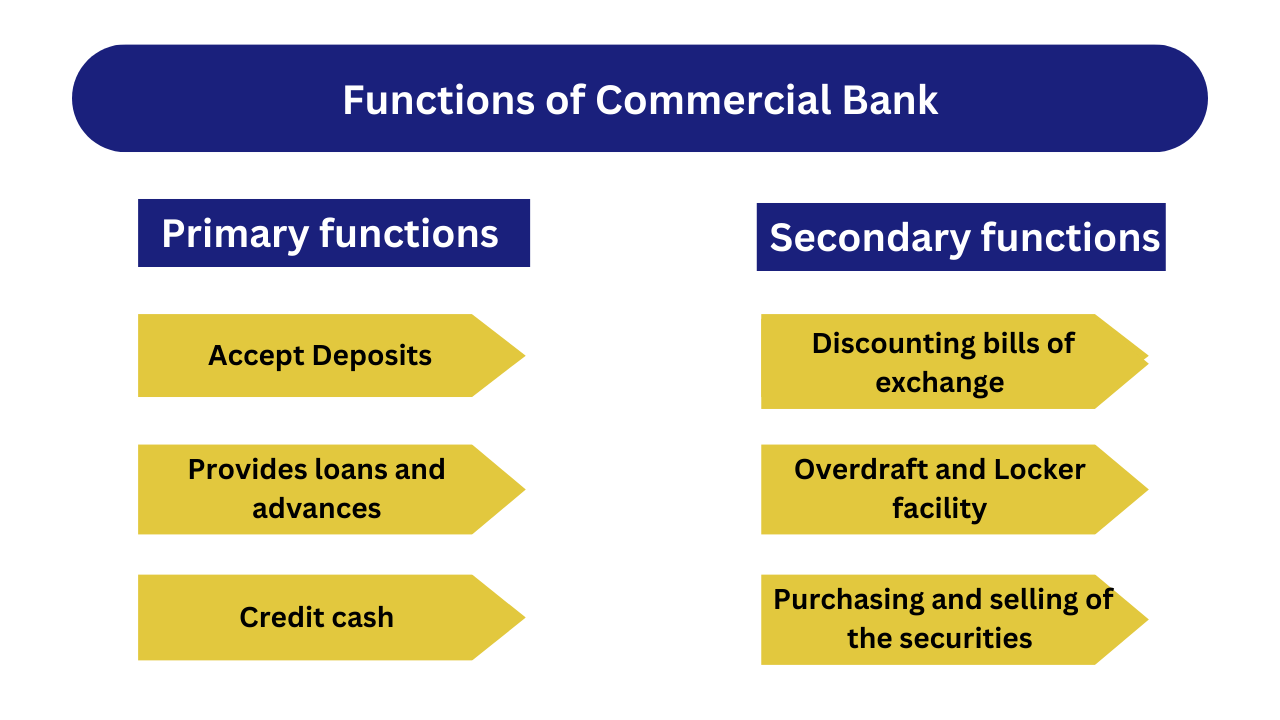

Functions of Commercial Bank

The functions of commercial banks are classified into two main divisions.

(a) Primary functions

Accept Deposits: The bank accepts savings, current, and fixed deposits. The surplus balances acquired from firms and individuals are used to meet the temporary needs of commercial activities.

Provides loans and advances: Another essential duty of this bank is to provide loans and advances to entrepreneurs and company owners while collecting interest. For any bank, it is the principal source of earnings. In this method, a bank keeps a small portion of its deposits as a reserve and gives (lends) the remainder to borrowers through demand loans, overdrafts, cash credit, short-term loans, and other similar products.

Credit cash: Clients who receive credit or loans are not given liquid cash. First, a bank account is formed for the consumer, and then the funds are sent. This procedure enables the bank to manufacture money.

(b) Secondary functions

Discounting bills of exchange: It is a written agreement acknowledging the amount to be paid in exchange for products purchased at a future date. The payment can also be made before the specified period using a commercial bank discounting mechanism.

Overdraft facility: An advance made to customers by allowing the current account to overdraw up to a certain maximum.

Purchasing and selling of the securities: The bank allows you to sell and acquire securities.

Locker facilities: A bank offers customers lockers to keep their valuables or documents safe. Banks demand a minimum annual fee for this service.

How do commercial banks work?

Commercial banks play an essential role in the financial system by offering various financial services to individuals, businesses, and governments. Here's a simple explanation of how commercial banks operate:

- Accepting deposits.

Commercial banks offer a secure environment for consumers and corporations to deposit money. These deposits can take numerous forms, including savings accounts, current accounts, and fixed deposits. Banks pay interest on these deposits, which varies according to the type of account and the current economic conditions.

- Making Loans

The primary activity of commercial banks is to lend money. These loans can be for various purposes, including personal, mortgage, auto, and business financing. Banks charge interest on these loans, typically more than the interest they pay on deposits. The difference between interest gained on loans and interest paid on deposits is a significant source of bank profits.

- Credit Creation

When banks lend money, they only sometimes provide real cash but instead establish credit that is deposited into the borrower's account. This technique effectively expands the money supply in the economy. Banks must save a portion of deposits as reserves, which limits the overall quantity of money they can produce.

- Payment and Settlement Services

Banks provide critical services that let money move inside and between economies. This includes managing checking accounts, allowing debit and credit card transactions, giving Internet banking services, and processing wire transfers. These services are critical to personal financial management and corporate operations.

- Financial Services

Aside from basic banking activities, commercial banks provide various other financial services, including wealth management, investment advice, currency exchange, and safe deposit lockers. They are also progressively offering insurance and retirement planning services.

- Risk Management

Before granting loans, banks conduct rigorous risk assessments to reduce potential default losses. They also handle interest, currency, and investment risk. Prudent risk management promotes the bank's financial health and stability.

- Implementing Monetary Policy

As the central bank instructs, commercial banks are essential in implementing a country's monetary policy. Commercial banks often implement policies impacting interest rates and reserve requirements, which affect lending, borrowing, and total economic activity.

- Regulation and Compliance

Commercial banks are subject to robust regulatory frameworks to protect their stability and integrity. They must follow different rules and regulations that govern their operations, including consumer protection, anti-money laundering, and capital adequacy.

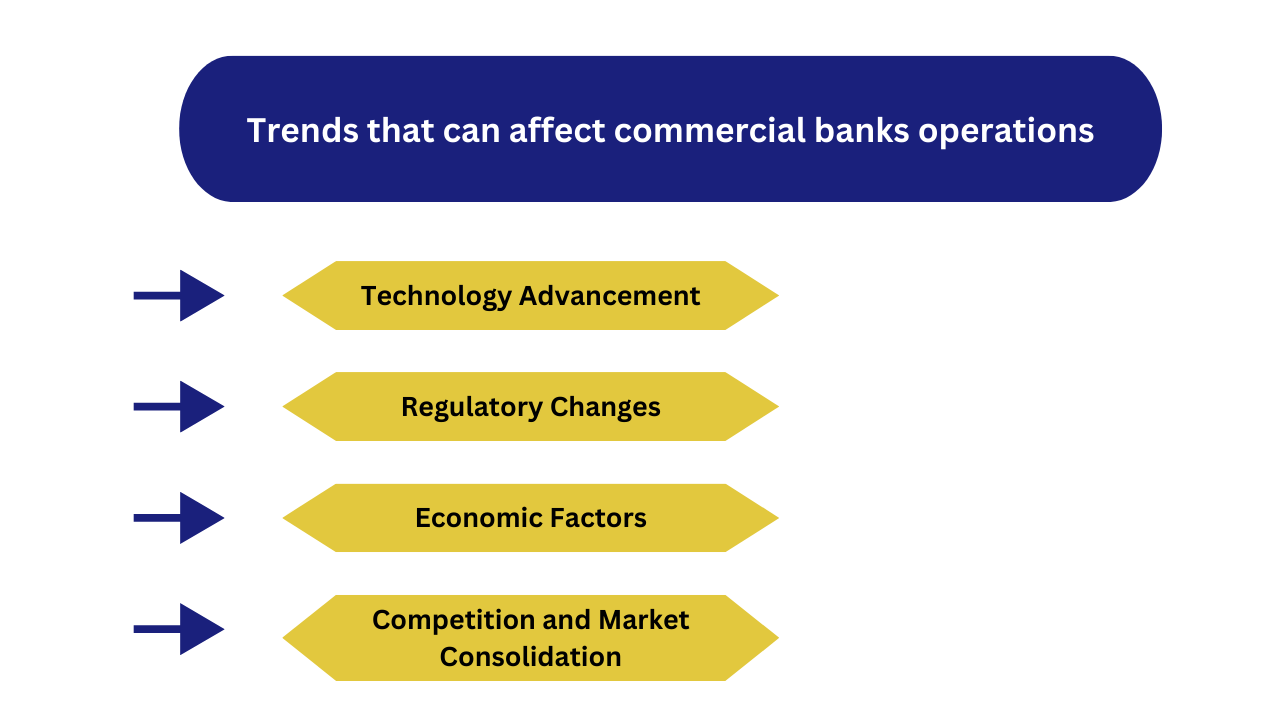

Trends that can affect commercial banks operations

Some of the trends, ranging from economic changes to technological advancements. Understanding these trends is crucial for banks to adapt and thrive.

Here are some key trends that can influence commercial bank operations:

- Technological advancements

- Digital Banking: The trend to internet and mobile banking is accelerating. Customers demand smooth digital services to manage their accounts, move funds, and obtain credit.

- FinTech Competition: Startups and non-traditional financial services companies provide novel banking solutions such as peer-to-peer payments, neobanks, and digital wallets, forcing incumbent banks to innovate.

- Blockchain and cryptocurrency: These technologies provide new methods for processing payments and protecting transactions, potentially lowering costs and increasing transaction speed.

- Cybersecurity: As banking services digital, cybersecurity becomes more important. Banks must make significant investments in system security to secure sensitive financial data.

- Regulatory Changes

- Increased Regulation: Following the financial crisis, there has been an increase in worldwide regulatory scrutiny. Banks must meet more strict capital adequacy, liquidity, and consumer protection standards.

- International Regulations: Different legislation across jurisdictions challenges global banking operations, necessitating banks' flexibility and adaptability.

- Environmental, Social, and Governance (ESG) Criteria: Banks face increased pressure to incorporate ESG criteria into their operations and lending procedures, influencing investment decisions and risk assessments.

- Economic Factors

- Interest Rate Changes: The central bank's interest-rate decisions considerably impact bank profitability. Low-interest rate environments can reduce net interest margins and earnings.

- Economic Cycles: Recessions and booms influence loan demand and default rates. Banks must carefully manage the risks that come with economic downturns.

- Global Economic Instability: Trade wars, Brexit, and global pandemics can all disrupt financial markets and bank operations worldwide.

- Competition and Market Consolidation

- The banking industry may consolidate through mergers and acquisitions to improve competitiveness, decrease costs, and leverage resources.

- Global Expansion: Banks aim to expand into new markets to capitalise on growth prospects, particularly in emerging economies where banking penetration is still increasing.

Example

The State Bank of India (SBI), the country's largest public sector banking and financial services corporation, is a well-known example of an Indian commercial bank. SBI has an extensive network of branches in India and abroad.

It provides a wide range of services expected to commercial banks, including:

- Personal Banking Services: SBI offers savings accounts, fixed deposits, personal loans, home loans, auto loans, and education loans to meet the different needs of its customers.

- Business Banking: The bank provides products specialised to businesses, such as business loans, trade finance services, and treasury solutions. SBI also offers specialist banking solutions for small and medium-sized firms (SMEs), with an awareness of their distinct financial demands.

- Digital Banking: The banks have made substantial technological investments to provide robust online and mobile banking services such as digital payments, online account management, and digital loans. The bank's digital platform, YONO (You Only Need One), is viral for its extensive financial services, which are easily accessible via cellphones.

- NRI Services: Recognizing India's substantial diaspora, SBI provides specialist services for non-resident Indians, such as NRI accounts, foreign currency loans, and investment opportunities in India.

FAQ

What are the different types of commercial banks?

Commercial banks can be divided into various types:

- Public sector banks are owned by the government and offer full banking services.

- Private Sector Banks: Owned by private entities, they provide identical services to public banks but serve different consumer sectors.

- Foreign banks are those that are headquartered outside of the country but have branches within it, and they frequently specialise in international banking services.

- Regional rural banks specialise in serving rural areas and the agriculture sector.

Difference between Central bank and commercial bank

The primary differences are:

- Central banks oversee the country's financial system and monetary policy, whereas commercial banks provide financial services to individuals, corporations, and institutions.

- Central banks issue money, handle the country's foreign reserves, and function as bankers for the government and commercial banks. Commercial banks primarily accept deposits, lend money, and provide other financial services.

- Profit Orientation: Central banks do not seek profit, whereas private banks do.

What are Commercial bank investment programs?

Commercial banks' investment programs usually focus on:

- Risk management entails investing in a combination of high- and low-risk securities to balance prospective rewards with the safety of bank money.

- Cash management entails ensuring that there is enough cash to meet depositors' daily operational needs and withdrawal demands.

- Diversification is the process of spreading investments across numerous industries and asset types in order to reduce the risks associated with a particular investment or market.

- Regulatory compliance entails adhering to regulations that limit the types of investments that banks can undertake and the amount of capital that can be kept against specific assets.

Why choose Us?

Filing Buddy is an entity which is focused at providing legal, financial, and corporate and compliances consultancy services to business entities. Our organisation is a structure made of enthusiastics.

EXPERTISE & RELIABILITY

Trusted industry professionals ensuring compliance, accurate tax filing, and comprehensive services for your business needs.

TAILORED SOLUTIONS

Customized services to meet your specific requirements, including business incorporation, trademarks, patents, and seamless GST return filing.

TIMELY SUPPORT

Dedicated support team committed to providing prompt assistance, resolving queries, and ensuring smooth operations for your business.

COMPETITIVE ADVANTAGE

Gain a competitive edge with our comprehensive suite of services, enabling you to focus on growth while we handle your compliance and taxation needs.

.webp)

.webp)

.webp)