Audit Readiness Guide for Businesses in India

By Filing Buddy . 14 Mar 26

When Audit Readiness Fails: Satyam’s Collapse and Audit Reality

In 2009, India witnessed one of the biggest corporate shocks when the chairman of Satyam Computer Services admitted that the company’s financial statements had been falsified for years. Profits were inflated, and cash balances shown in the books simply did not exist. Within days, billions in market value disappeared and investor trust collapsed.

For many business owners, this case revealed a hard truth: financial records and compliance processes cannot be treated casually. When documentation, reconciliations, and oversight are weak, problems can remain hidden until regulators or auditors step in.

Today, with digital tax systems like GST and increased regulatory scrutiny, businesses operate in an environment where inconsistencies are detected faster than ever.

In this guide, you’ll learn what audit readiness really means, why it matters for businesses, and how to build a practical audit checklist that prepares your organization for tax audits, GST verification, and compliance reviews.

Audit Readiness Explained

Audit readiness is often misunderstood as something businesses deal with only when an audit is announced. In reality, it is a continuous process of maintaining financial records, compliance documentation, and reconciliations so that they can be verified at any time.

Businesses that stay audit ready do not scramble for documents when a notice arrives. Instead, their systems already maintain the information auditors and regulators typically ask for.

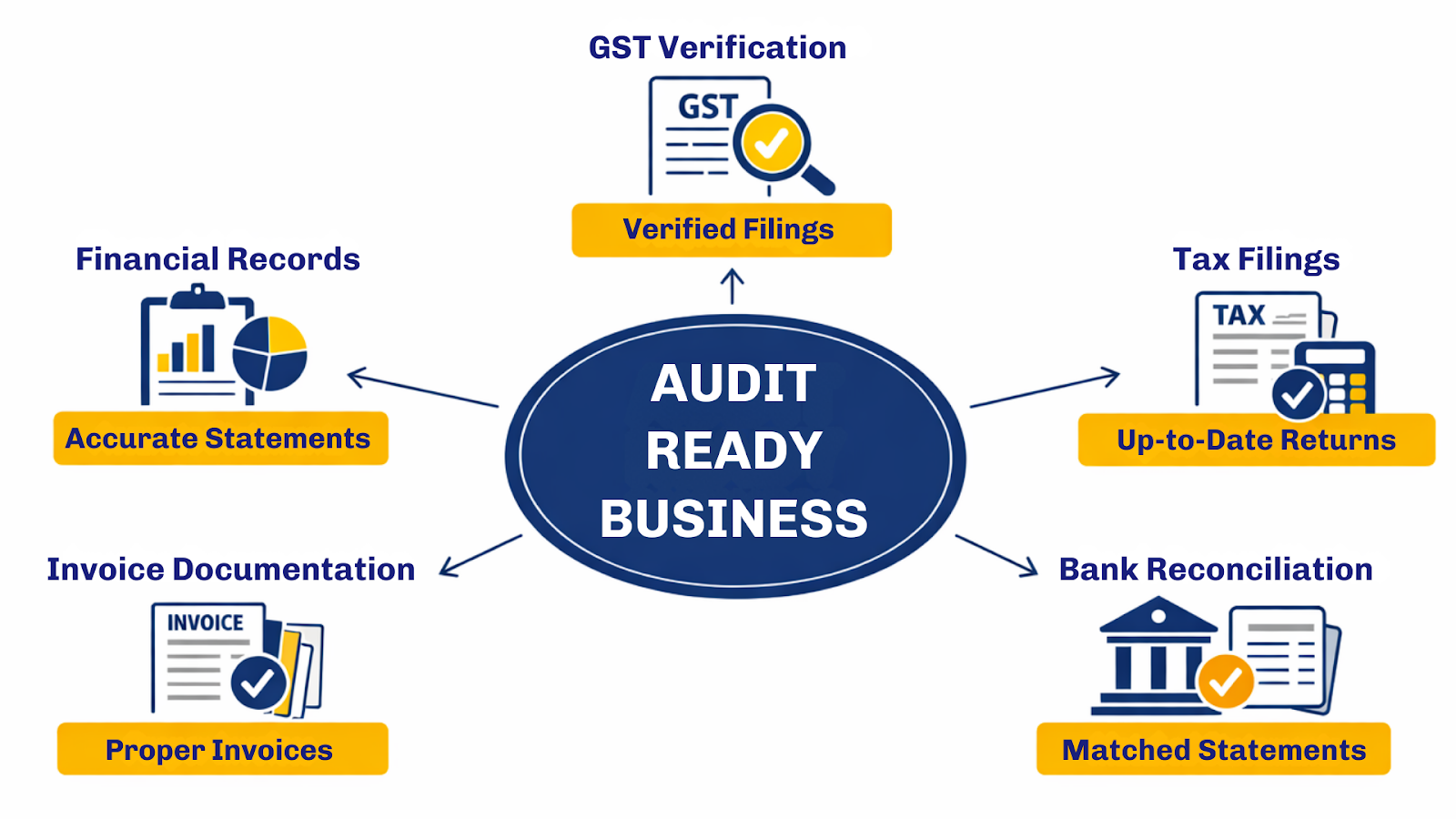

What Being Audit Ready Means

Audit readiness means a business maintains accurate, organized, and verifiable financial records that can be reviewed by auditors, regulators, or investors as needed.

In practical terms, an audit ready business can quickly produce documents such as:

- GST returns and reconciliations

- Profit and loss statements

- Balance sheets

- Sales and purchase invoices

- Bank statements

- Tax filings with supporting records

Being audit ready does not mean an audit is currently happening. It means the business has built systems that make responding to an audit straightforward if one occurs.

This distinction matters because many organizations start gathering records only after receiving a tax notice. By then, missing documents or mismatched data often create unnecessary complications.

A strong audit readiness framework usually includes:

- Organized accounting systems

- Monthly financial reconciliations

- Verified GST filings

- Proper invoice documentation

- Clear separation between personal and business expenses

When these processes are in place, responding to regulatory queries becomes far less stressful.

Why Founders Should Care

Many founders initially believe audits mainly affect large corporations. In reality, businesses of all sizes face compliance checks, particularly under GST, where digital systems automatically analyze financial data.

For founders, audit readiness offers several advantages:

- Faster responses to tax notices

- Higher credibility with investors and lenders

- Reduced risk of compliance penalties

- Clearer financial visibility for decision-making

During investor due diligence, one question often reveals the true state of a company’s financial discipline:

“Are your financials clean and verifiable?”

If answering that question requires digging through emails and spreadsheets for days, it signals weak governance. When records are structured and reconciled, however, it builds immediate confidence.

In other words, audit readiness supports both compliance and business credibility.

Audit Risks for Indian Businesses

Regulatory scrutiny has increased significantly in recent years. Digital systems like GST allow authorities to analyze financial data across multiple filings, making inconsistencies easier to detect.

Even well-established companies occasionally receive tax notices or compliance queries. Understanding these risks helps businesses strengthen their internal processes before regulators step in.

Reliance’s ₹57 Crore GST Notice

Even the largest corporations face tax scrutiny. For example, Reliance Industries reportedly received a GST notice worth around ₹57 crore from tax authorities related to alleged underpayment of taxes in certain transactions.

For a company of Reliance’s scale, responding to such notices involves large teams of tax professionals and compliance specialists.

The broader message for businesses is clear: no organization is beyond regulatory review.

For smaller companies that lack dedicated compliance teams, issues such as the following can escalate quickly:

- GST mismatches

- Incorrect invoice reporting

- Input tax credit discrepancies

These issues can result in:

- Tax demands

- Interest liabilities

- Monetary penalties

Because GST systems link supplier and buyer filings, authorities can easily identify mismatches across returns. This is why regular GST verification and reconciliation are essential parts of audit readiness.

How Audits Impact Operations

When a tax audit or business audit begins, its impact often extends beyond accounting.

The process can affect multiple aspects of operations:

- Finance teams must retrieve years of records

- Management must respond to regulatory queries

- Legal advisors may become involved

- Cash flow may be affected if liabilities arise

Operational disruption often becomes the highest hidden cost.

Companies undergoing tax scrutiny may need to produce:

- Invoice-level transaction data

- Vendor details

- Reconciliation statements

- Proof of tax payments

If these records are scattered across emails, spreadsheets, and accounting tools, gathering them becomes a time-consuming exercise.

An audit ready organization, on the other hand, treats documentation as a continuous process rather than a last-minute reaction.

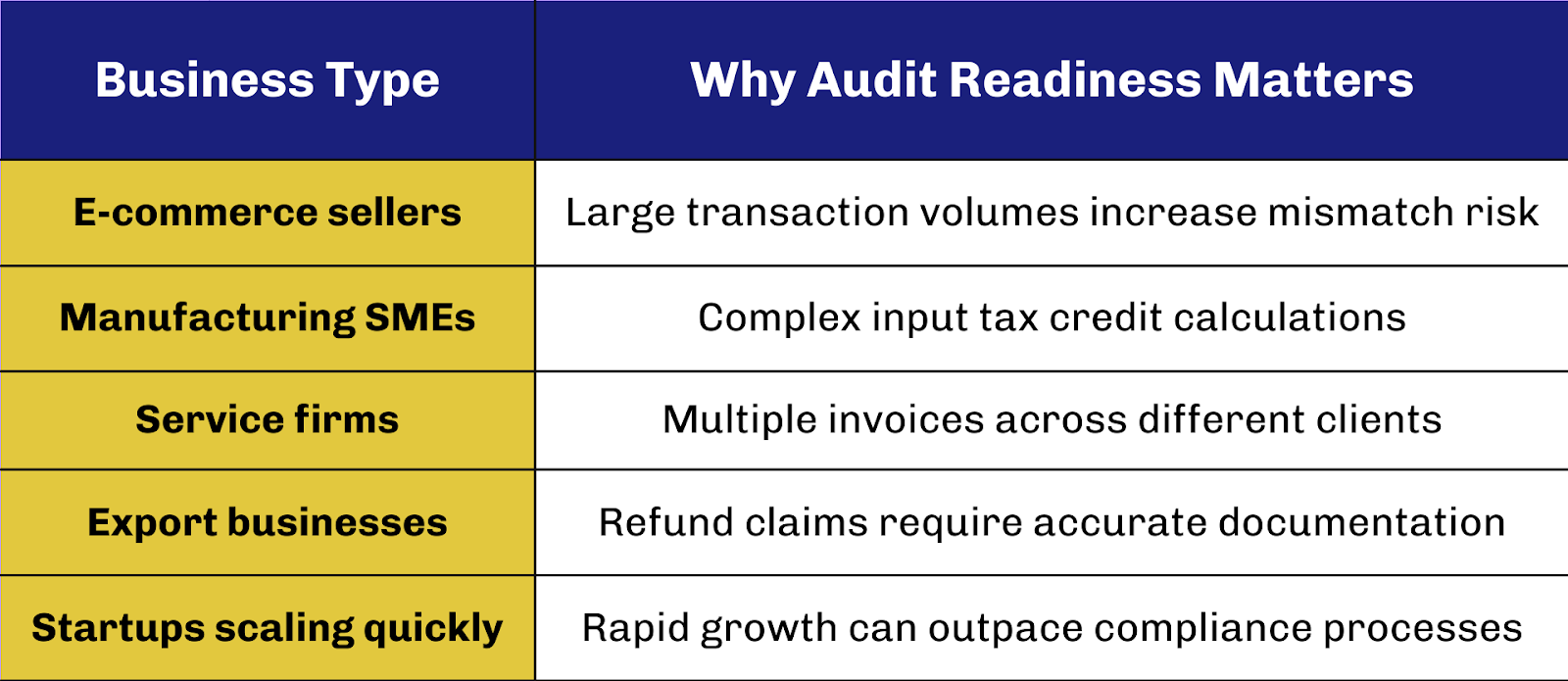

Businesses That Must Stay Audit Ready

Strong financial discipline benefits every organization, but certain businesses face higher scrutiny because of their operations, transaction volumes, or regulatory requirements.

Companies that grow quickly or operate in sectors with high GST activity often encounter verification checks more frequently.

Startups Facing Investor Due Diligence

Startups often focus heavily on product development and growth, but investors pay close attention to financial governance.

During funding rounds, investors conduct financial due diligence, which includes reviewing:

- accounting records

- tax filings

- compliance history

- liabilities and contingent risks

If inconsistencies appear in financial statements or tax filings, investors may delay or renegotiate funding.

In many cases, startups realize too late that compliance hygiene directly influences valuation and investor confidence.

Being audit ready ensures founders can demonstrate:

- financial transparency

- operational discipline

- compliance maturity

These signals matter greatly when negotiating funding or partnerships.

Businesses Under GST Verification

Businesses operating under GST face regular data checks because the system links transactions across suppliers and buyers.

Authorities frequently analyze mismatches between:

- GSTR-1 (sales reporting)

- GSTR-3B (tax payment)

- vendor filings

When discrepancies appear, businesses may receive scrutiny notices requesting explanations.

Some business categories face higher verification risks.

For these businesses, maintaining audit readiness ensures that GST verification checks can be handled smoothly.

The Practical Audit Checklist

Many business owners assume filing tax returns is enough to remain compliant. However, auditors and regulators typically review supporting documentation, reconciliations, and transaction trails in greater detail.

A practical audit checklist helps ensure that financial and tax data can be verified whenever required.

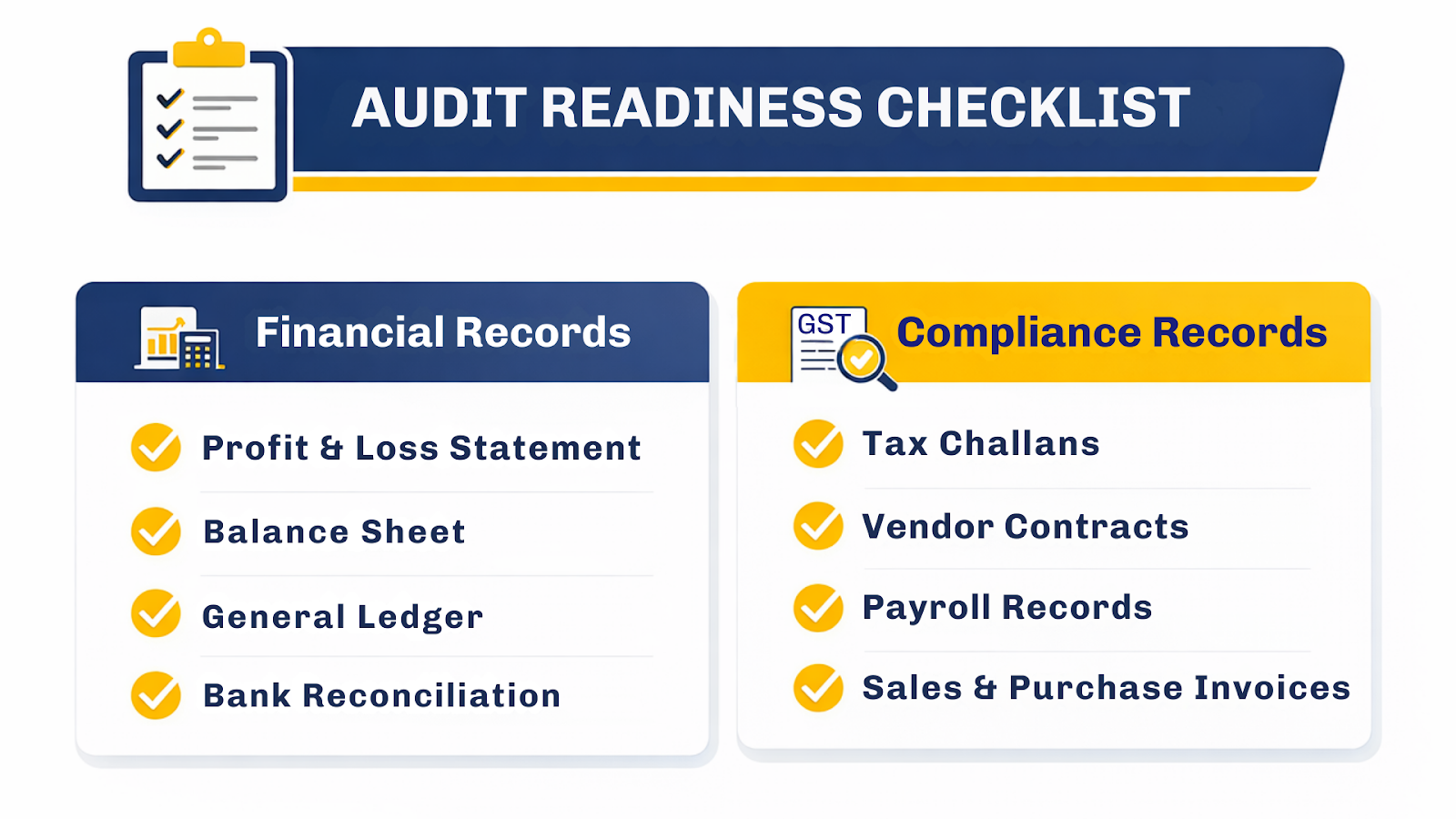

Core Financial Records Checklist

Even businesses that file tax returns regularly may struggle to produce supporting documentation during an audit.

An effective audit checklist typically includes:

- Profit and loss statements

- Balance sheets

- General ledger reports

- Bank reconciliation statements

- Sales and purchase invoices

- Vendor contracts

- Payroll records

- Tax payment challans

Maintaining these records in a structured format makes it easier to respond to regulatory queries.

Another overlooked aspect is data consistency across systems. Numbers reported in financial statements should match the data submitted in tax filings.

Even small mismatches can trigger deeper scrutiny.

GST Verification Essentials

GST compliance involves more than simply filing returns. Authorities increasingly rely on data analytics to verify whether businesses have reported transactions accurately.

A strong GST verification process includes:

- Monthly reconciliation between GSTR-1 and GSTR-3B

- Vendor invoice matching

- Input tax credit validation

- Verification of tax rate classifications

Compliance also extends to pricing transparency.

For example, regulators once investigated Tata Starbucks after a GST rate reduction. Authorities determined that the company had not passed on certain tax benefits to consumers, leading to action under anti-profiteering rules.

This case highlights an important insight: GST verification can examine how businesses price and report transactions, not just whether taxes were paid.

Maintaining clear records and calculations helps businesses demonstrate compliance during such reviews.

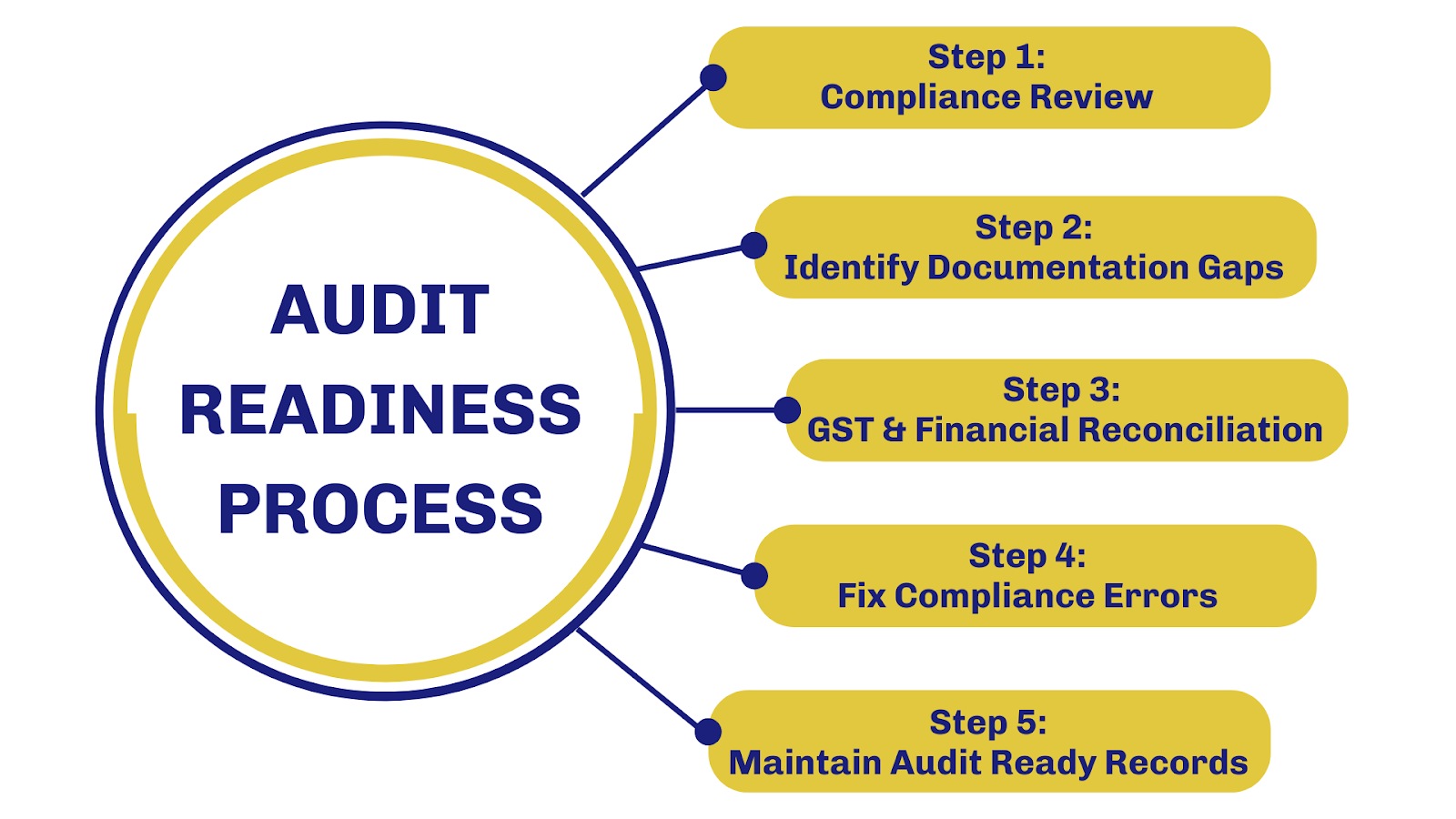

The Audit Readiness Process

Many businesses believe audits begin only when authorities send a notice. In reality, audit readiness begins much earlier, within the company’s daily financial processes.

Every invoice issued, GST return filed, and bank reconciliation completed creates a digital trail that auditors and regulators can review later.

Pre-Audit Gap Identification

Becoming audit ready usually begins with identifying gaps in existing compliance systems.

Businesses often discover issues such as:

- Missing invoices

- Mismatched GST filings

- Incomplete accounting records

- Vendor data inconsistencies

A structured review process typically includes:

- Reviewing past tax filings

- Reconciling financial records with GST data

- Checking documentation for major transactions

- Verifying tax payments and credits

Finding these issues early allows businesses to fix them before regulators raise questions.

For many organizations, this stage reveals how fragmented their documentation systems have become over time.

Fixing Compliance Before Tax Audit

Once gaps are identified, businesses can begin correcting compliance issues.

Common corrective actions include:

- Reconciling GST returns

- Updating accounting entries

- Validating vendor invoices

- Organizing supporting documents

Rapidly growing startups sometimes encounter these challenges as they scale.

For instance, Zomato disclosed GST demand and penalty orders exceeding ₹40 crore from authorities during tax assessments.

Cases like this demonstrate how growing businesses often face deeper scrutiny as they scale. Preparing documentation and reconciliations in advance makes responding to such queries far easier.

Cost of Poor Audit Readiness

Many businesses assume compliance gaps only result in small penalties. In reality, poor audit readiness can lead to much larger problems, including tax demands, operational disruption, and reputational damage.

When regulators question financial records, businesses may need to explain transactions from several years earlier. Without organized documentation, even legitimate companies may struggle to justify their numbers.

₹285 Crore GST Fraud Crackdown

Poor documentation can sometimes escalate into serious investigations.

In one major case, authorities uncovered a network of shell companies used to claim fraudulent GST input tax credits, resulting in penalties estimated at around ₹285 crore. Courts upheld enforcement actions against individuals involved in facilitating the scheme.

Investigators found that fake invoices and fabricated transactions were used to claim tax benefits.

While most legitimate businesses are not involved in fraud, the case demonstrates an important point: authorities closely analyze invoice trails and transaction records.

Incomplete documentation can easily raise suspicion during such reviews.

Business Audit Penalties Explained

When compliance gaps are discovered during a tax audit or business audit, penalties can arise in several forms.

Common consequences include:

- Tax demands for underreported liabilities

- Interest on unpaid taxes

- Monetary penalties

- Extended scrutiny or investigation

In severe cases, authorities may also:

- Block input tax credit

- Freeze bank accounts

- Initiate legal proceedings

Beyond financial penalties, reputational damage can also affect relationships with investors, lenders, and business partners.

This is why proactive audit readiness is far more effective than reacting after receiving a notice.

Build Audit Readiness Early

Audit readiness is ultimately about discipline and transparency in financial practices. Businesses that keep their records organized and compliance processes consistent are far better prepared to handle audits, regulatory checks, or financial reviews.

The key takeaways are simple:

- Audit readiness should be continuous, not reactive

- Poor documentation can lead to penalties and scrutiny

- Clear financial records build trust and operational confidence

In practice, this means maintaining organized records, verifying GST filings regularly, and ensuring transactions are properly documented.

Staying proactive about compliance makes audits far less stressful. Stay compliant with Filing Buddy.

FAQs

1. What does audit readiness mean for a business?

Audit readiness means maintaining accurate financial records, reconciliations, and compliance documents so auditors or regulators can review them anytime. An audit ready business can quickly provide GST filings, invoices, tax records, and financial statements without scrambling for documents.

2. Why is audit readiness important for businesses?

Audit readiness reduces the risk of penalties, tax notices, and compliance stress. It also improves financial transparency, builds credibility with investors and lenders, and allows businesses to respond quickly to regulatory queries.

3. What is included in an audit checklist?

An audit checklist typically includes financial statements, GST returns, bank reconciliations, invoices, vendor contracts, payroll records, tax payment challans, and supporting documentation for major transactions.

4. How often should a business review its audit readiness?

Businesses should review audit readiness at least quarterly. Regular reconciliation of financial records and GST filings ensures errors are detected early and corrected before they become compliance issues.

5. What triggers a GST verification by authorities?

GST verification may be triggered by mismatches between GSTR-1 and GSTR-3B filings, incorrect input tax credit claims, suspicious invoice patterns, or discrepancies between vendor and buyer filings.

6. What is the difference between a tax audit and a business audit?

A tax audit verifies whether a business has correctly reported income and taxes under tax laws. A business audit reviews overall financial records, internal controls, and compliance processes.

7. Which businesses are more likely to face audits?

Businesses with high transaction volumes, GST registrations, large input tax credit claims, rapid growth, or complex vendor networks are more likely to face tax audits or GST verification checks.

8. Can small businesses be audited?

Yes. Small businesses can be audited, especially under GST compliance checks or income tax scrutiny. Digital tax systems allow authorities to detect inconsistencies regardless of business size.

9. What documents are required during a tax audit?

Common documents include financial statements, GST returns, invoices, purchase records, bank statements, ledgers, payroll data, and tax payment proofs.

10. What are common mistakes that make businesses fail audits?

Common mistakes include poor record-keeping, missing invoices, mismatched GST filings, incorrect input tax credit claims, and inconsistent financial statements.

11. How does GST reconciliation help with audit readiness?

GST reconciliation ensures that sales data, tax payments, and vendor invoices match across filings. Regular reconciliation prevents mismatches that could trigger tax notices or GST verification.

12. What happens if a business fails an audit?

If discrepancies are found, authorities may impose tax demands, interest charges, penalties, or further investigations. In severe cases, authorities may restrict input tax credits or initiate legal action.

13. How can businesses prepare for a GST audit?

Businesses should maintain proper invoices, reconcile GST returns regularly, verify vendor filings, and keep organized documentation for tax payments and financial transactions.

14. Does audit readiness help during investor due diligence?

Yes. Investors often review financial records, tax filings, and compliance history before investing. Being audit ready helps businesses demonstrate transparency and financial discipline during due diligence.

15. How can Filing Buddy help businesses stay audit ready?

Filing Buddy helps businesses organize financial documentation, verify GST filings, and prepare compliance records. Its “We Are Audit Ready” certificate helps businesses demonstrate structured financial processes and regulatory preparedness.

Contact Us

An expert will call you within 24 hours. No payment required to get started.

Related Post

How to Obtain a Company Registration Number in India

Understanding Corporate Identification Numbers (CINs) and How to Obtain Them in India

. 2 mins.png)

Difference between Udyog Adhaar and Udyam Certificate

Want to get registered for Udyog Aadhar and Udyam Certificate? Here is their registration processes. Also, know about their differences. Explore their features, benefits, and processes to register online for each, helping you to choose the right option as per your need.

. 3 min read.png)

Changing Your Bank Signatory? Here are the Y Documents Required by Most Banks in India

Learn how bank signatory is important for financial workflow. Know why bank signatories are important and discover the documents required to change signature of your signatory.

. 5 min read