180-Day Depreciation Rule for Computers in India

By Filing Buddy . 13 Mar 26

Fiscal Optimization of Technology Acquisitions

In the modern Indian business world, buying technology is no longer just a simple shopping trip; it’s a high-stakes chess game played between tax laws and financial strategy. To save the most money, companies have to be obsessed with the "180-day rule," which says that if you don't start using your new gear (like servers or software) for at least half the year, you lose half of your tax depreciation benefits for that year. At the same time, businesses have to balance three different rulebooks: the Income Tax Act (which helps you pay less tax now), the Companies Act (which makes sure your books look honest to shareholders), and the GST framework (which lets you get a refund on the taxes you paid during the purchase).

The Legislative Foundation: Section 32 and the Block of Assets Concept

In simple terms, Indian tax law doesn't make you track every single laptop or chair separately. Instead, it puts similar items into "buckets" called Blocks of Assets. Every year, you get a discount on your taxes because your tech gets older and loses value, this is called Depreciation.

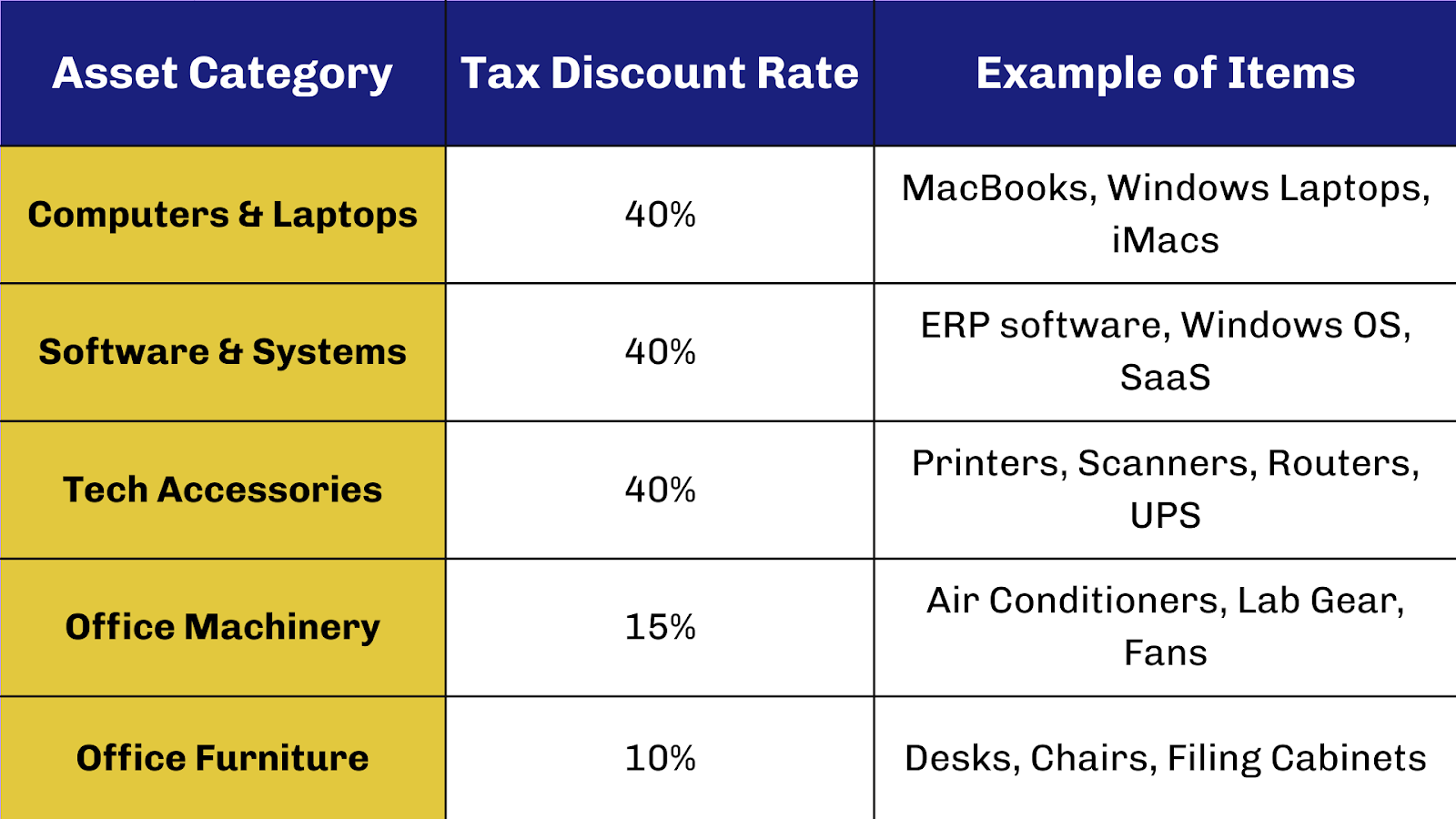

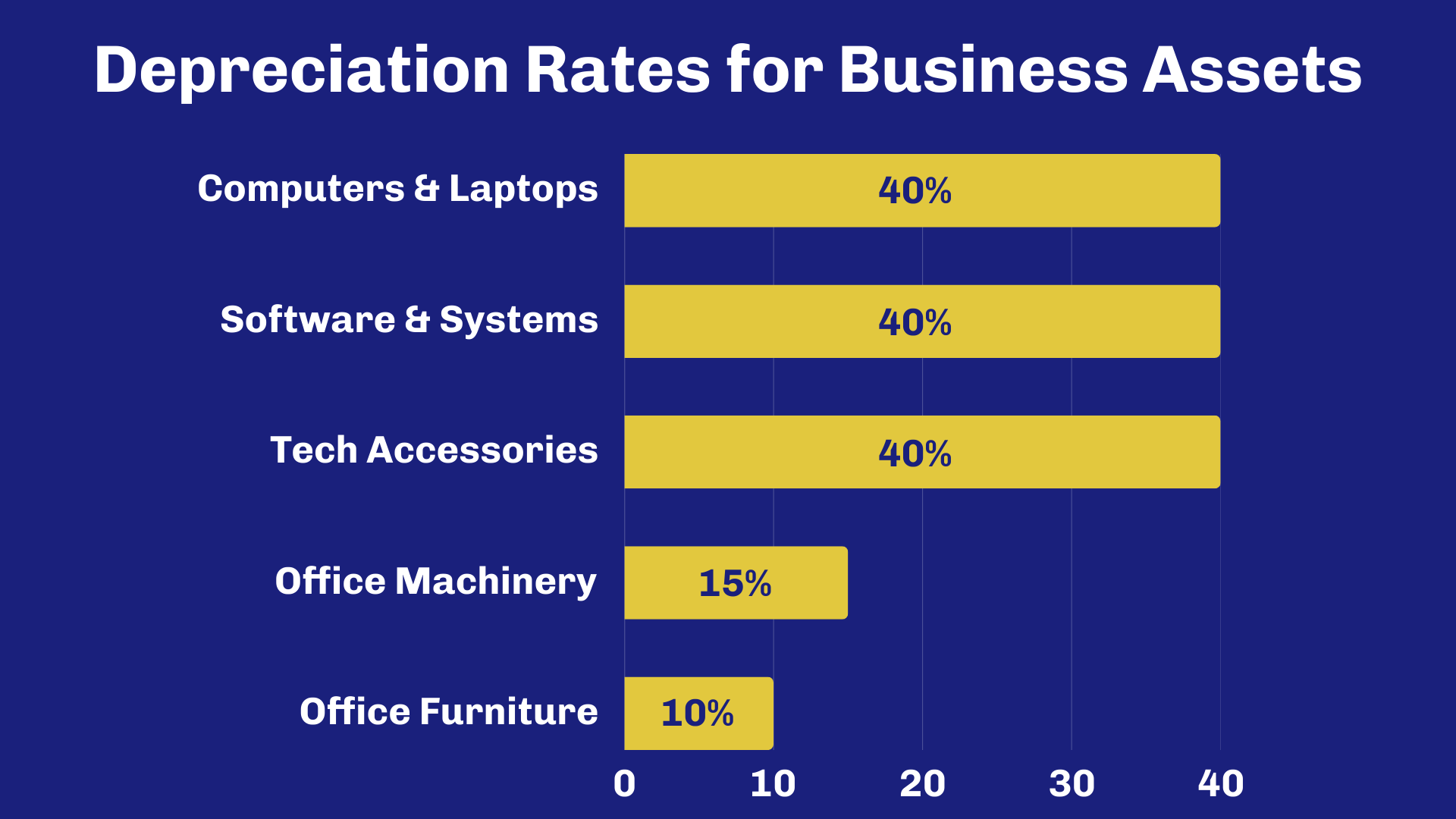

For tech gear like Mac Books, the government is generous: they know gadgets become outdated fast, so they let you write off 40% of the value every year. The only catch? You must start using the device for at least 180 days (roughly 6 months) in a financial year to get that full 40% discount. If you buy it late in the year, you only get half (20%) for that first year.

Tax Discount (Depreciation) Rates at a Glance

3 Things to Remember for Your Business

- The "Bucket" System: You don't delete a laptop from your books the moment it breaks. As long as there is a balance left in the "Computer Bucket," you keep getting tax benefits on the remaining value.

- The 180-Day Rule: To maximize your savings, try to buy and start using your tech before October 4th. If you buy it on October 5th or later, your tax benefit for that year is cut in half.

- Accelerated Savings: Because the rate is 40% for laptops, you can effectively "recover" the cost of your MacBook through tax savings much faster than you would for office furniture

Tactical Timing: The 180-Day Proviso and the October Cutoff

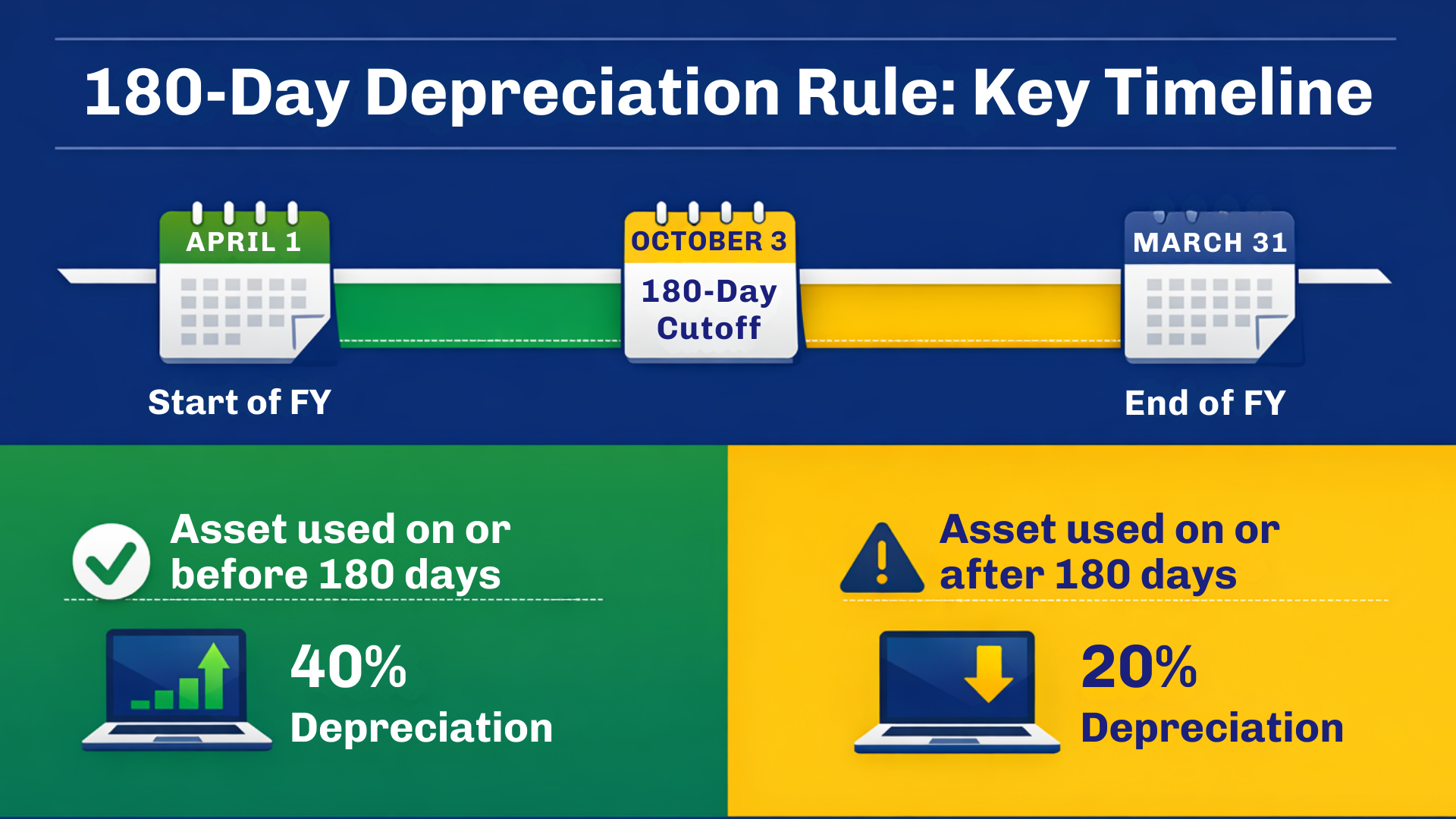

The 180-day rule is the most important deadline for your business budget. If you want a full tax discount on your new tech this year, you must not only buy it but also start using it for at least half the year (180 days).

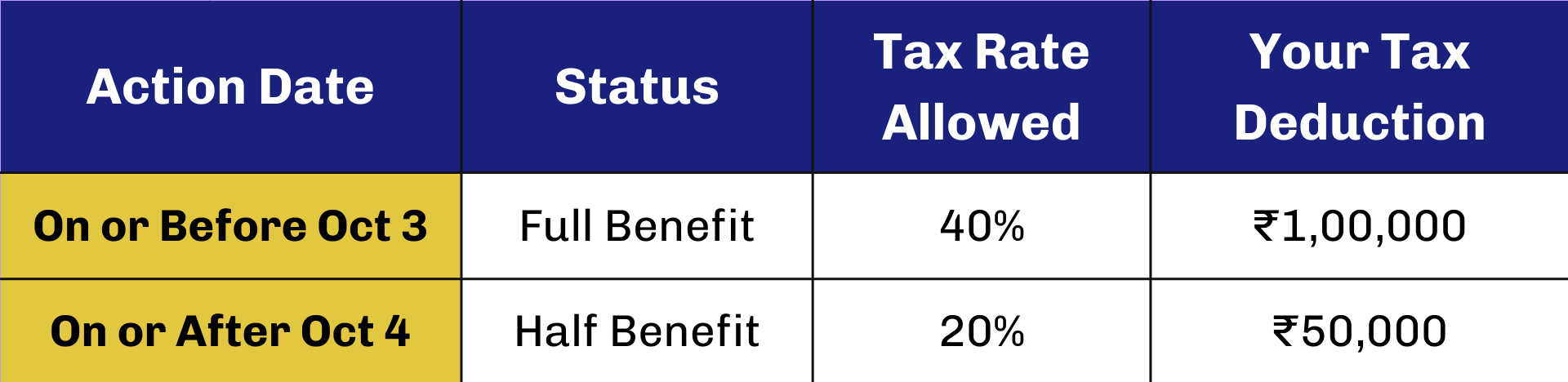

In India, the financial year ends on March 31. To hit that 180-day mark, your "Magic Date" is usually October 3 (or October 4 in a leap year like 2024 or 2028). If you miss this date by even one day, the government cuts your tax benefit in half for that entire year.

The Cost of Missing the Deadline

Example: Buying a high-end MacBook worth ₹2,50,000

"Buying" vs. "Putting to Use"

A common mistake is thinking the Invoice Date is all that matters. The law specifically says the asset must be "Put to Use."

- The Risk: If you buy 50 MacBooks on September 25 but they sit in a locked cupboard until October 10 because the office wasn't ready, you only get the 50% (half) benefit.

- The Proof: To protect yourself during a tax audit, keep proof that the tech was actually working, like IT installation logs, emails sent from the new devices, or "Ready to Use" certificates from your tech team.

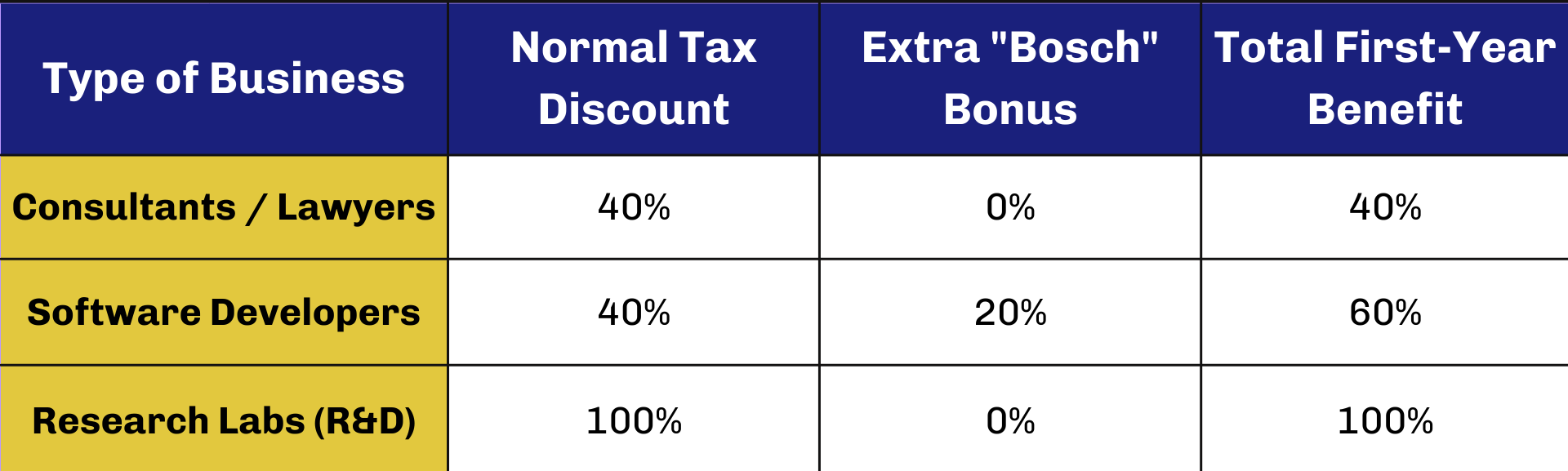

The "Bosch" Hack: How Software Companies Get 60% Tax Benefits

Normally, the government gives an extra 20% "Additional Depreciation" only to factories that manufacture physical products. However, a major legal win (the Bosch case) has changed the game for the Indian tech sector. The courts ruled that developing software is just like "manufacturing" a product.

This means if you are a software startup or an IT company, your Mac Books and servers aren't just "office gadgets", they are the "factory machinery" used to build your software.

Comparison of First-Year Tax Shields

Critical Rules to Claim the 60%

- The "Production" Rule: You can only claim the extra 20% on Mac Books used by developers and engineers who actually "build" the software. If you give a MacBook to an HR manager or an Accountant, the tax office will likely reject the extra 20% claim because they aren't "producing" anything.

- The 180-Day Split: If you start using the laptop after October 3, both benefits are cut in half for that year (20% normal + 10% extra = 30% total).

- Carry Forward: If you miss the full claim because you bought the laptop late, don't worry, the law allows you to claim the remaining 10% of that "extra" bonus in the next financial year.

- Proof is Mandatory: You must keep a "Laptop Register" that shows exactly which employee is using which serial number and what their job role is.

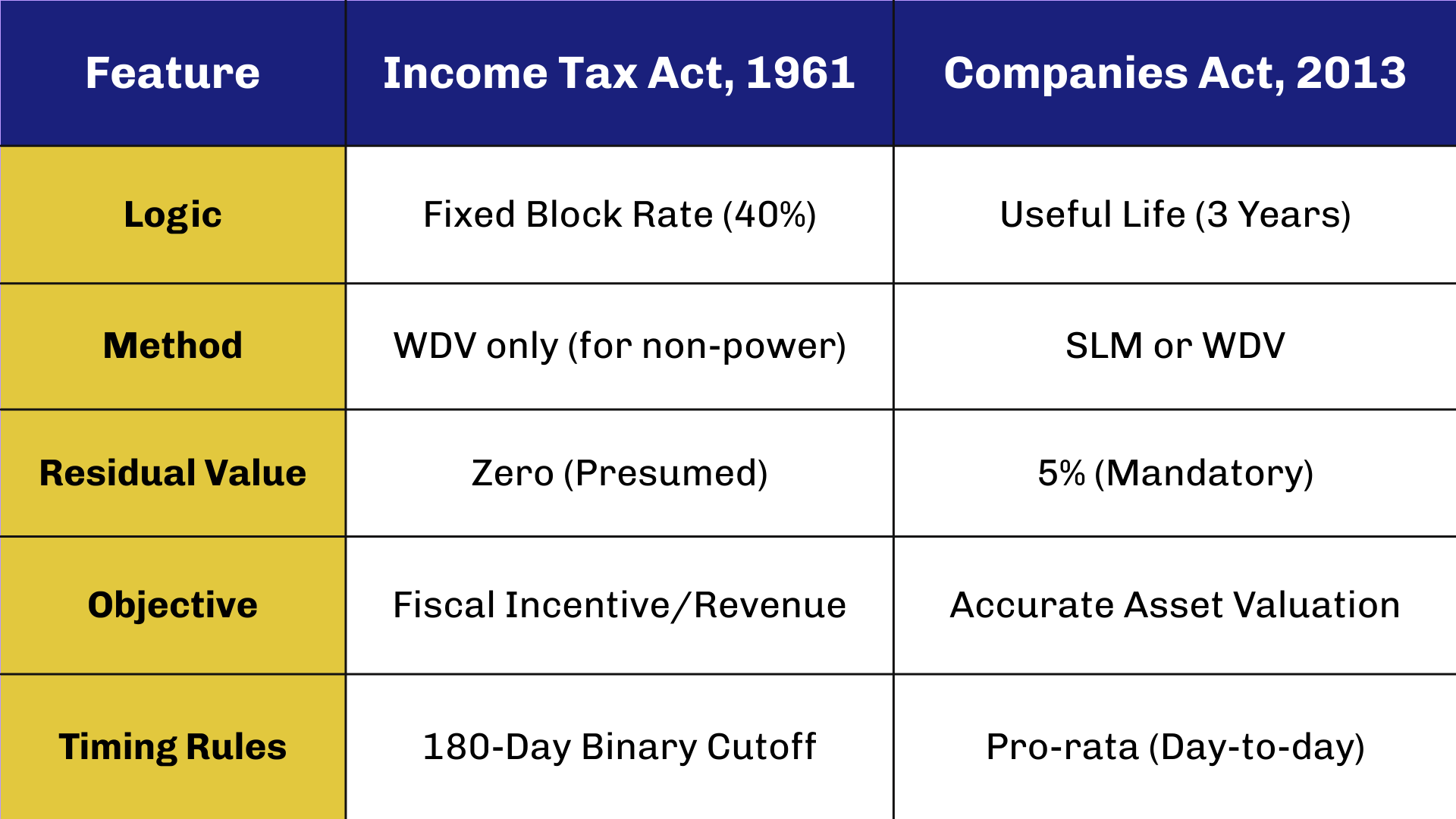

Companies Act vs. Income Tax Act: The Dual Record-Keeping Mandate

Corporate entities in India face a divergence in how they must report depreciation for financial statements versus tax filings. This leads to the necessity of maintaining two separate depreciation schedules.

The Fair Valuation Objective of the Companies Act

Under the Companies Act, 2013, specifically Schedule II, the objective of depreciation is to represent a "true and fair view" of the asset’s consumption over its useful life. For computers and laptops, the useful life is established at 3 years, and for servers, it is 6 years. Companies can choose between the Straight-Line Method (SLM) and the Written Down Value (WDV) method.

The Companies Act requires a pro-rata calculation of depreciation from the exact date the asset is available for use. This is far more precise than the 180-day binary rule used in taxation. For a MacBook purchased in November, the Companies Act would allow depreciation for five months of usage, whereas the Income Tax Act would allow a flat 50% of the annual 40% rate. This disparity creates a "timing difference," necessitating the recognition of Deferred Tax Assets (DTA) or Deferred Tax Liabilities (DTL) in the corporate balance sheet.

Presumptive Taxation (Section 44ADA): The Freelancer's VIP Lane

For independent professionals, including software developers, designers, and consultants, the Income Tax Act provides a simplified "presumptive" scheme under Section 44ADA. This scheme allows eligible individuals to pay tax on a presumed profit of 50% of their gross receipts, effectively exempting them from the need to maintain detailed expense records or claim individual depreciation.

The Deemed Depreciation Catch

A critical nuance often overlooked by freelancers is that while Section 44ADA assumes that the 50% of receipts not taxed cover all business expenses, the law mandates that the WDV of any business asset shall be calculated as if the depreciation had been actually allowed.

If a freelance UI designer earns ₹40 lakhs and buys a MacBook for ₹2 lakhs, and opts for Section 44ADA, they declare ₹20 lakhs as income. They cannot claim the ₹80,000 MacBook depreciation separately. However, for the next year’s records, the MacBook’s value is still deemed to have fallen to ₹1,20,000. This adjustment is vital because if the professional later moves out of the presumptive scheme or sells the MacBook, the "deemed" depreciation will be subtracted from the original cost to calculate the short-term capital gain or loss.

Digital-First Thresholds for 2025-26

The Union Budget has enhanced the limits for Section 44ADA to encourage digital adoption. If an individual's cash receipts do not exceed 5% of their total gross receipts, they can opt for the presumptive scheme even if their turnover reaches ₹75 lakhs. For professionals whose primary costs are high-end technology (like the Mac Studio or MacBook Pro), the 50% profit assumption is often highly advantageous, as their actual operational expenses may be significantly lower than the 50% deemed allowance.

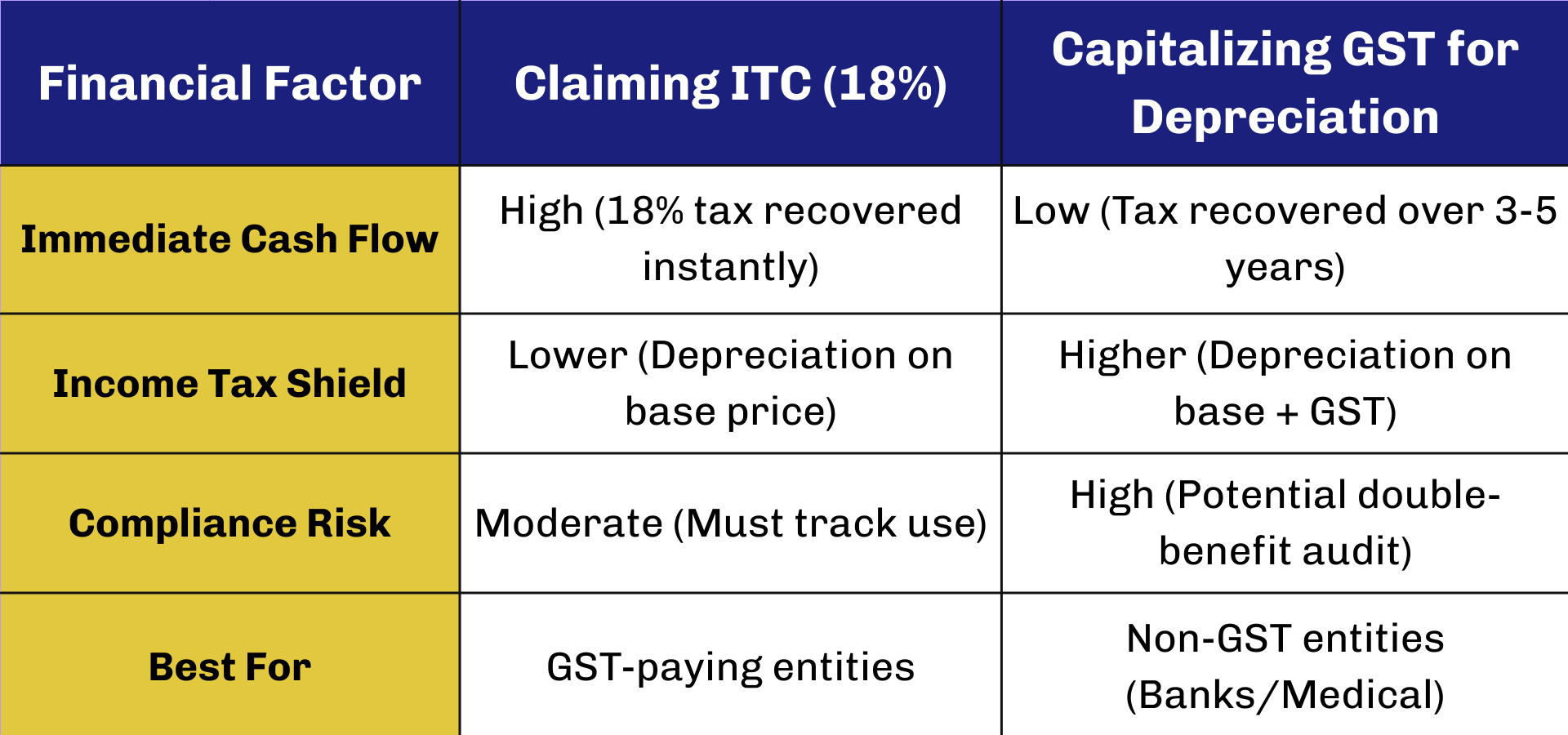

GST Integration: Navigating Input Tax Credit and Capitalization

The purchase of a MacBook in India attracts a standard GST rate of 18% under HSN Code 8471. For a business, the treatment of this 18% tax component is a pivotal tax planning decision governed by Section 16(3) of the Central Goods and Services Tax (CGST) Act.

The Section 16(3) Prohibition

The statute provides a clear restriction: a registered person cannot claim both Input Tax Credit (ITC) and depreciation on the tax component of the cost of capital goods.

- Option A: Claiming ITC (Recommended for most businesses): The buyer records the MacBook's base price as a capital asset and treats the 18% GST as an "Input Tax Credit". This GST amount is immediately available to offset the GST payable on the company’s sales. This provides a 100% recovery of the tax component in the first month.

- Option B: Capitalizing GST (Depreciation Shield): The buyer adds the 18% GST to the cost of the MacBook and claims 40% depreciation on the total amount. This reduces the Income Tax liability but loses the immediate 18% GST benefit.

For a MacBook Pro with a base price of ₹2,11,864 and GST of ₹38,136 (Total ₹2,50,000), a GST-registered developer should claim the ₹38,136 as ITC. Capitalizing it would only provide an initial income tax shield of ₹15,254 (40% of the GST component), which, at a 30% tax rate, results in a measly ₹4,576 actual tax saving, far inferior to the ₹38,136 liquid cash benefit of the ITC.

Section 35: The 100% Deduction for Scientific Research

In certain high-technology sectors, such as Artificial Intelligence, Biotech, or Renewable Energy, MacBooks may be used for scientific research related to the business. In such instances, Section 35 of the Income Tax Act provides an even more aggressive "hack" than the 180-day rule: a 100% immediate deduction.

Capital Expenditure in In-House R&D

Section 35(1)(iv) allows for a deduction of the entire capital expenditure incurred on scientific research. Unlike Section 32, which follows a declining balance method, Section 35 allows a company to write off the full cost of the hardware in the year of purchase, regardless of whether it was bought in April or March.

There are, however, stringent conditions:

- Exclusions: This benefit is not available for land. Buildings and computers, however, are eligible.

- No Double Benefit: Once a 100% deduction is claimed under Section 35, the taxpayer is prohibited from claiming depreciation on the same asset under Section 32 for any previous year or the current year.

- Revenue vs. Capital: Revenue expenses for R&D (salaries, materials) are also 100% deductible.

For deep-tech startups, this provision serves as a massive accelerator for early-stage growth, as it reduces taxable income to zero for significant periods while the firm builds its intellectual property.

The Evidence Audit: Proving "Put to Use" in the Digital Age

As the 180-day rule pivots on the exact date an asset is placed in service, the Income Tax Department has become increasingly sophisticated in auditing technology claims. Merely possessing an invoice dated September 28 is no longer sufficient; taxpayers must be prepared to prove that the MacBook was operational before the October 3 cutoff.

Terminal-Based Forensic Evidence

MacOS maintains several timestamped files that act as a digital "birth certificate" for the device's operational life. Tax auditors may request, or businesses should proactively store, the following technical logs to verify their claims :

- The AppleSetupDone File: This file is created precisely when the initial user setup is completed on a new MacBook. By running in the Terminal, the system reveals the exact creation date and time.

- The Install Log: Navigating to /var/log and accessing install.log provides a granular record of when the operating system was first initialized or upgraded.

- The mSCP Audit: Advanced enterprises use the macOS Security Compliance Project (mSCP) scripts to generate audit records. These records establish what types of events occurred and when, providing an immutable trail of "use".

Physical and Administrative Documentation

In addition to digital logs, a robust tax defense strategy includes:

- Asset Assignment Letters: A document signed by the employee acknowledging receipt and commencement of work on the MacBook on a specific date.

- IT Register Entry: An entry in the company’s internal hardware inventory system showing the device serial number and the date it was "pushed" to the active network.

- Proof of Business Nexus: Evidence of work output, such as code commits to GitHub, design files saved to a server, or emails sent from the new device, dated between the purchase date and October 3.

The Impact of the 2025-26 Budget on Tech Procurement

The Union Budget for FY 2025-26 has introduced shifts in the personal and corporate tax landscape that influence hardware procurement decisions.

The Dominance of the New Tax Regime

The New Tax Regime is now the default for all individual taxpayers. While it offers lower rates, it disallows many traditional deductions like 80C. However, for those with business income (ITR-3 or ITR-4), depreciation remains a vital tool for reducing the "Gross Total Income" before the slabs are applied.

For individuals in the 30% slab, every ₹1,00,000 in depreciation saves ₹30,000 in cash tax. This makes the 180-day rule equally relevant for high-earning individual consultants as it is for large corporations.

MSME and Startup Relief

The budget has also focused on credit access for Micro and Small Enterprises (MSEs). The Credit Guarantee Fund for MSEs has been expanded, providing collateral-free loans to help startups finance high-value hardware like Mac Pro setups or server stacks. This allows startups to leverage "other people's money" to buy the hardware and then use the government's tax shield (depreciation) to pay off the interest on those loans.

Refurbished Hardware: The Secondary Market Strategy

A secondary "hack" involves the procurement of refurbished MacBooks. Under Indian law, used or refurbished goods are generally taxed at the same 18% GST rate unless they fall under specific margin schemes for second-hand dealers.

From a depreciation standpoint, used assets follow the same 40% rate as new ones, provided they are new to the business. However, "Additional Depreciation" (the 20% Bosch bonus) is strictly prohibited for second-hand plant and machinery. For an entity not engaged in manufacturing (where the 20% bonus is not applicable anyway), buying a high-performance refurbished MacBook on October 1 can be an exceptionally efficient move: a lower capital outlay combined with the full 40% first-year depreciation shield.

Conclusion: Orchestrating the Hardware Cycle

The procurement of technology in India is a multi-dimensional fiscal operation that extends far beyond the point of sale. The 180-day rule acts as the primary governor of this process, creating a definitive deadline of October 3 for those seeking to maximize their first-year tax savings. By understanding the interaction between the Income Tax Act’s block-of-assets system and the Companies Act’s useful-life reporting, businesses can better manage their earnings and cash reserves.

The integration of the Bosch precedent provides a powerful incentive for software developers to treat their MacBooks as production machinery, potentially shielding 60% of the cost in year one. Meanwhile, the strategic choice between GST Input Tax Credit and capitalization ensures that the 18% tax component is recovered in the most liquid form possible. Ultimately, for the modern professional or tech enterprise, the decision to "Buy that Mac now" is a calculated move to convert a necessary expenditure into a strategic tax asset, fueling future innovation through optimized fiscal discipline.

FAQ:

1. What is the 180-day depreciation rule in India?

The 180-day rule under Section 32 of the Income Tax Act states that if an asset is used for 180 days or more in a financial year, full depreciation is allowed. If used for less than 180 days, only 50% of the normal depreciation rate can be claimed.

2. What is the depreciation rate for computers and laptops in India?

Computers, laptops, and related technology equipment qualify for a 40% depreciation rate under the Income Tax Act. This higher rate reflects the rapid technological obsolescence of digital assets.

3. What happens if an asset is used for less than 180 days?

If a capital asset is used for less than 180 days in a financial year, the taxpayer can claim only half of the eligible depreciation rate in that year. The remaining depreciation continues in subsequent years.

4. What is the cutoff date for the 180-day rule?

Since the financial year ends on 31 March, the practical cutoff date is around 3 October. Assets purchased and put to use after this date typically qualify for only 50% depreciation in the first year.

5. Does the invoice date determine depreciation eligibility?

No. Depreciation eligibility depends on the date the asset is “put to use,” not the invoice date. Businesses must ensure the equipment is operational before the 180-day cutoff.

6. Can software companies claim additional depreciation?

Yes. Software development companies may qualify for additional depreciation of 20% if their activities are considered manufacturing or production under judicial precedents like the Bosch ruling.

7. Can freelancers claim depreciation on laptops?

Freelancers can claim depreciation if they follow the regular taxation method. However, professionals opting for Section 44ADA presumptive taxation cannot separately claim depreciation, as expenses are already assumed within the 50% deemed deduction.

8. Can businesses claim GST ITC and depreciation on the same asset?

No. Under Section 16(3) of the CGST Act, businesses cannot claim Input Tax Credit and depreciation on the GST component of the same asset simultaneously.

9. What is the GST rate on laptops and computers in India?

Laptops and computers are taxed at 18% GST under HSN Code 8471. Registered businesses can usually claim this amount as Input Tax Credit if the asset is used for business purposes.

10. Do companies maintain separate depreciation records for tax and accounting?

Yes. Companies typically maintain two depreciation schedules:

One for the Income Tax Act (tax reporting)

Another for the Companies Act (financial statements).

11. How is depreciation calculated under the Companies Act?

Under the Companies Act, depreciation is calculated based on the useful life of the asset, often using Straight Line Method (SLM) or Written Down Value (WDV). For computers, the typical useful life is three years.

12. Can refurbished computers be depreciated?

Yes. Refurbished or second-hand computers can be depreciated at the same rate of 40% if they are new to the business. However, additional depreciation is generally not allowed on second-hand machinery.

13. What proof is required to show an asset is “put to use”?

Businesses should maintain documentation such as installation logs, IT asset registers, employee assignment letters, network activation records, or operational emails to prove the asset was actively used.

14. Can research companies claim 100% deduction on technology purchases?

Yes. Under Section 35 of the Income Tax Act, businesses engaged in scientific research may claim 100% deduction on capital expenditure, including computers used for research activities.

15. Why is depreciation important for businesses?

Depreciation helps businesses reduce taxable income, reflect the declining value of assets, and improve cash flow planning by spreading the cost of equipment over multiple years.

Contact Us

An expert will call you within 24 hours. No payment required to get started.

Related Post

How should a start-up complete ITR filing

Business entities must file their ITR annually to comply with the tax laws of their respective countries. It helps the government assess and collect the appropriate amount of income tax from taxpayers and ensures proper accountability of financial activities.

. 3 Mins.png)

5 step checklist for GST compliance in Indian Startups

Learn about how GST works. The basics of GST along with its compliances. Uncover what your business needs to keep in mind concerning GST rules and GST compliance.

. 3 min read.png)

₹20 Lakhs and Beyond: Understanding GST for Freelancers in India

Are you a freelancer or aspiring to be one? In this blog, uncover the basics of freelancing and requirements involving GST. Learn about all the exemptions, obligations, and compliances of GST for freelancers in india.

. 5 min read