TDS on Provision: Rules for Audit Fees & 194J

By Filing Buddy . 26 Mar 26

Why TDS on Provision Matters

Many businesses assume TDS applies only when payment is made. No invoice, no payment, no deduction, that’s the common thinking. But a Supreme Court ruling challenged that assumption. In Palam Gas Service v. CIT (2017), the Court clarified that disallowance under Section 40(a)(ia) can apply whether an expense is paid or payable if applicable TDS was not deducted.

This matters because businesses routinely record year-end provisions for audit fees and professional services before the actual invoice arrives. A typical entry may look like this:

Audit Fees A/c Dr

To Provision for Audit Fees

Many finance teams wait for the invoice before deducting TDS, assuming the compliance trigger hasn’t occurred yet. In this guide, we’ll explain when TDS on provision becomes applicable, how Section 194J applies to audit fees, and what businesses should review before closing their books to avoid hidden compliance risks.

Understanding TDS on Provision

Accounting rules and tax rules don’t always move at the same speed.

From an accounting standpoint, businesses recognize expenses when the liability arises, not when the bill is received. This ensures financial statements show the true cost of running the business during that financial year.

To achieve this, companies create provisions for expected expenses such as audit fees, consultancy payments, or legal retainers. While this practice is standard in financial reporting, it can raise important questions under the TDS provisions of the Income Tax Act.

What Is TDS on Provision

A provision is an accounting entry used to record an expense that has already been incurred but has not yet been invoiced or paid.

For example, at the end of the financial year, a company might estimate the statutory audit fee and pass the following entry:

Audit Fees A/c Dr

To Provision for Audit Fees

This entry ensures the expense appears in the correct financial year even if the auditor sends the invoice later.

However, under the Income Tax Act, TDS must generally be deducted at the earlier of:

- Credit of the amount to the payee’s account

- Payment of the amount

This is where the complexity begins. When the credit is made to a provision account instead of directly to the vendor, businesses often assume that the TDS obligation has not yet arisen.

Tax authorities, however, look beyond the name of the account. They examine whether the provision effectively represents a credit to a specific service provider.

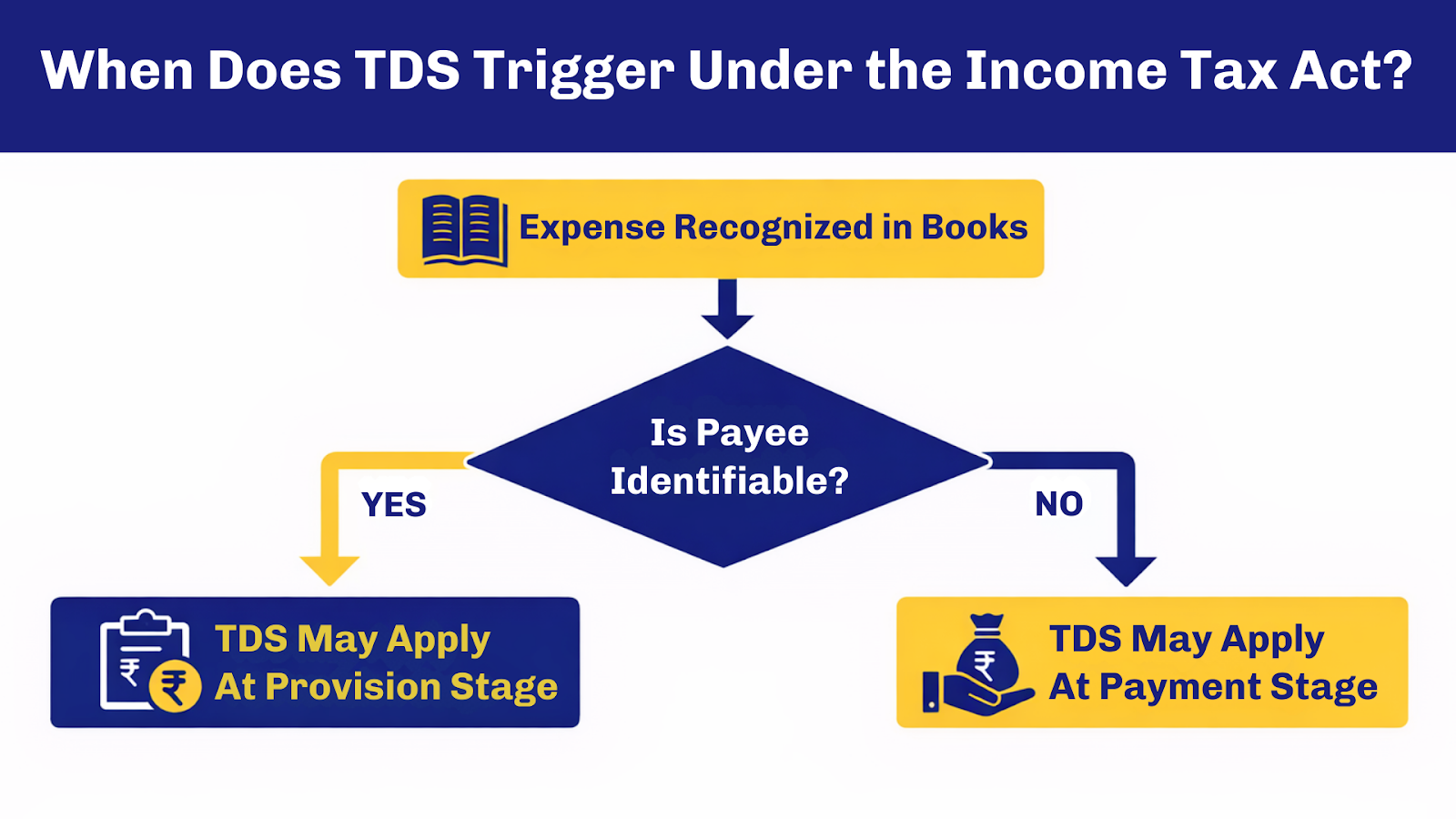

TDS on Provision for Expenses

When tax authorities review year-end provisions, they usually look at one simple factor: whether the payee is identifiable.

Two questions are typically examined:

- Is the service provider known?

- Does the provision represent a real liability to that provider?

If the answer to both questions is yes, the tax department may treat the provision as a credit to that payee, even if the invoice has not yet been issued. In such cases, TDS may need to be deducted at the time the provision is recorded.

Let’s look at two common scenarios.

Example 1: Vendor already identified

Audit Fees A/c Dr

To Provision for Audit Fees – CA Firm XYZ

Here, the company already knows who will receive the payment.

Because the payee is identifiable, tax authorities may view this entry as a constructive credit to the auditor, which could trigger TDS obligations.

Example 2: Vendor not yet identified

Professional Expenses A/c Dr

To Provision for Professional Fees

In this case, the specific service provider is not yet known. Since the payee cannot be identified, courts have sometimes held that TDS may not apply at the provisioning stage.

The practical takeaway

For finance teams, the rule of thumb is simple:

- Payee identified → TDS may apply on the provision

- Payee not identified → TDS may apply later when payment is made

This distinction becomes especially important for audit fees and professional services, which fall under Section 194J of the Income Tax Act.

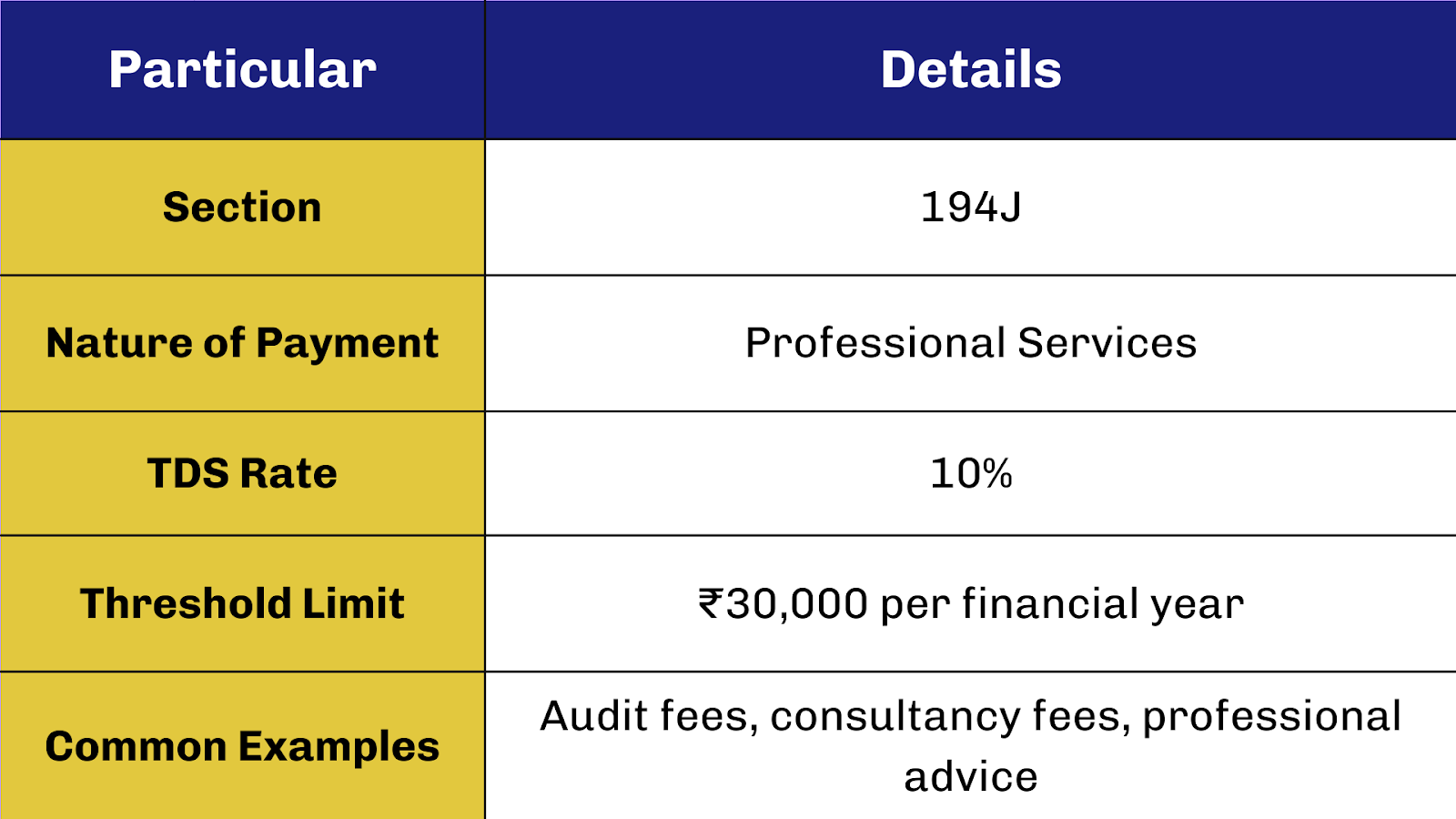

TDS on Audit Fees Rules

Audit services are classified as professional services under the Income Tax Act. Because of this classification, payments for audit work fall under Section 194J, which governs TDS on professional and technical services.

194J and Professional Payments

Section 194J applies to payments made for various professional services, including:

- Chartered accountant services

- Legal consultancy

- Technical consultancy

- Architectural services

- Interior design services

- Medical and engineering services

Since statutory audits and internal audits are performed by chartered accountants, audit fees clearly fall within the scope of this provision.

The key rules under Section 194J are summarized below:

Once payments to a professional exceed the threshold, TDS must generally be deducted at the time of credit or payment, whichever occurs earlier.

This rule is precisely why year-end provisions for professional services often come under scrutiny during tax assessments.

TDS on Professional Fees Timing

The timing rule under Section 194J sounds simple but creates practical challenges.

TDS must be deducted at the earlier of:

- Credit of the expense in the books

- Actual payment

This means that even if the payment is made months later, the TDS obligation may arise as soon as the expense is recognized.

For businesses that create year-end provisions for audit or consultancy services, this timing rule becomes critical.

The moment a provision is recorded, finance teams must evaluate whether that entry effectively represents a credit to an identifiable professional service provider.

And that question has been examined repeatedly in tax disputes involving major corporations.

Identifiable Payee Changes Everything

When courts evaluate disputes related to TDS on provisions, one factor repeatedly determines the outcome: whether the payee was identifiable when the provision was created.

When TDS on Provision Applies

A notable illustration appears in proceedings involving Accenture Services Pvt Ltd. Tax authorities reviewed the company’s year-end provisions for vendor payments and questioned whether TDS should have been deducted at the time those provisions were recorded.

The tribunal observed that if the recipient of the income is clearly identifiable, and the provision reflects a liability toward that specific party, TDS obligations may arise even if the invoice has not yet been issued.

This principle has shaped how tax authorities analyze provisions today.

Finance teams often evaluate provisions using a simple framework:

The takeaway for businesses is subtle but important.

A provision that looks routine in accounting terms can still trigger TDS compliance expectations if it clearly relates to a specific vendor or service provider.

And this issue is not limited to smaller companies; even multinational corporations have faced scrutiny on this point.

Lessons from Large Corporations

Year-end provisions are a normal part of financial reporting. Large companies often record hundreds of such entries while closing their books.

However, these provisions sometimes become focal points during tax assessments.

TDS on Professional Fees Timing

In proceedings involving IBM India Pvt Ltd, tax authorities examined provisions recorded for vendor payments, including professional services.

The department argued that if the company had already identified the vendors who would receive the payment, then the liability effectively existed at the time the accounting entry was recorded. As a result, the obligation to deduct TDS could arise even before the actual payment was made.

Cases like this highlight an important lesson: TDS compliance should not be evaluated only at the payment stage.

Businesses that regularly work with:

- Auditors

- Consultants

- Legal advisors

- Technical specialists

Often, create provisions for these services during financial closing. Once the liability toward these professionals becomes identifiable, those entries may fall within the scope of Section 194J.

That is why experienced finance teams review all professional service provisions carefully before finalizing year-end accounts.

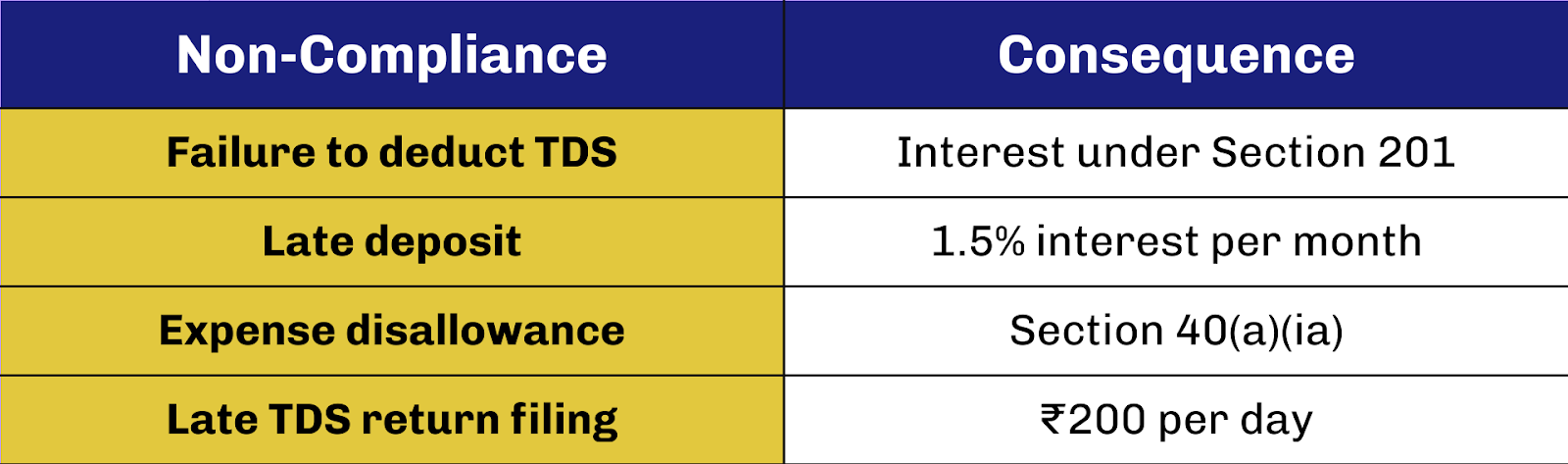

Consequences of Missing TDS

Many businesses assume that if the vendor ultimately pays tax on the income, the payer’s responsibility disappears.

However, tax law treats these obligations separately.

Financial Impact of TDS Defaults

In Hindustan Coca-Cola Beverage Pvt Ltd v. CIT, the Supreme Court clarified that if the recipient has already paid tax on the income, the government cannot recover the same TDS amount again from the payer.

However, the ruling also confirmed that interest liability and compliance consequences may still apply.

This means missing TDS deductions can still result in several financial implications.

The expense disallowance rule can have a significant impact.

If TDS was required but not deducted, up to 30% of the expense may be disallowed, thereby increasing the business's taxable income.

For companies that incur substantial audit or consultancy fees, this can materially affect their tax liability.

Smart TDS on Provision Strategy

Understanding the rule is one thing. Applying it consistently during financial closing is another.

Finance Teams’ Year-End Checklist

Another Supreme Court ruling, GE India Technology Centre Pvt Ltd v. CIT, clarified that TDS obligations arise only when the payment represents income chargeable to tax in India.

Although the case primarily dealt with cross-border payments, it reinforced an important principle: businesses must evaluate the nature and taxability of the payment before deciding whether TDS applies.

For professional services like audit or consultancy work, the payment is generally taxable in India. This makes provisions for such services particularly relevant for TDS review.

Many finance teams follow a practical checklist before closing their books:

- Review all provisions for professional services

- Confirm whether vendors are already identified

- Check if payments exceed the ₹30,000 threshold under Section 194J

- Deduct TDS before finalizing the financial statements

- Maintain documentation explaining how the provision was calculated

These reviews often reveal small entries that might otherwise go unnoticed, and many of those entries relate to audit fees, legal retainers, or consultancy charges.

Closing the TDS on Provision Gap

Expense provisioning is a routine accounting practice, but from a tax perspective, it can quietly create compliance obligations.

The key insight is that TDS rules are triggered by recognition of liability, not just payment of money.

Across court rulings and tax proceedings, a clear pattern emerges:

- When the payee is identifiable, provisions may trigger TDS obligations.

- Audit fees generally fall under Section 194J, attracting TDS on professional fees.

- Ignoring TDS during provisioning can lead to interest, disallowances, and compliance scrutiny.

For businesses that rely on auditors, consultants, and advisors, these rules often surface during year-end reviews or tax assessments.

Taking a proactive approach, reviewing provisions, confirming vendor identification, and evaluating Section 194J applicability, helps ensure that routine accounting entries do not turn into avoidable tax exposures.

Staying ahead of these details keeps your financial operations audit-ready and penalty-proof. Platforms like Filing Buddy help businesses manage TDS deductions, filings, and compliance checkpoints, ensuring that even complex rules around TDS on provision are handled with clarity and confidence.

FAQs

1. Is TDS applicable on provision for expenses?

TDS may apply on provisions if the payee is identifiable and the expense represents a liability toward that party. If the provision is general and the service provider is not identified, TDS may not apply immediately.

2. Do you need to deduct TDS on audit fees?

Yes. Audit fees are considered professional services under Section 194J, so TDS must be deducted at 10% if the payment exceeds ₹30,000 in a financial year.

3. When should TDS be deducted under Section 194J?

TDS under Section 194J must be deducted at the earlier of credit of the expense in the books or actual payment to the professional.

4. Is TDS required if the invoice is not received?

Possibly. If the expense is recorded in the books and the payee is identifiable, TDS may still be required even if the invoice has not been issued yet.

5. What is the TDS rate on professional fees?

The TDS rate on professional fees under Section 194J is 10%, provided the total payment to the professional exceeds ₹30,000 in a financial year.

6. Does TDS apply to year-end provisions?

TDS can apply to year-end provisions if the liability relates to a specific vendor or professional. If the provision is a general estimate without identifying the payee, TDS may not apply immediately.

7. What happens if TDS is not deducted on audit fees?

If TDS is not deducted, the payer may face interest under Section 201, late filing penalties, and expense disallowance under Section 40(a)(ia).

8. Can an expense be disallowed if TDS is not deducted?

Yes. Under Section 40(a)(ia), up to 30% of certain expenses can be disallowed if applicable TDS was not deducted or deposited.

9. Is TDS applicable on professional services?

Yes. Payments for professional services such as audit, legal advice, consultancy, and technical services are subject to TDS under Section 194J.

10. What is the threshold limit for TDS under Section 194J?

TDS under Section 194J applies when the total payment to a professional exceeds ₹30,000 in a financial year.

11. Do companies deduct TDS on statutory audit fees?

Yes. Companies must deduct TDS on statutory audit fees under Section 194J if the payment exceeds the prescribed threshold.

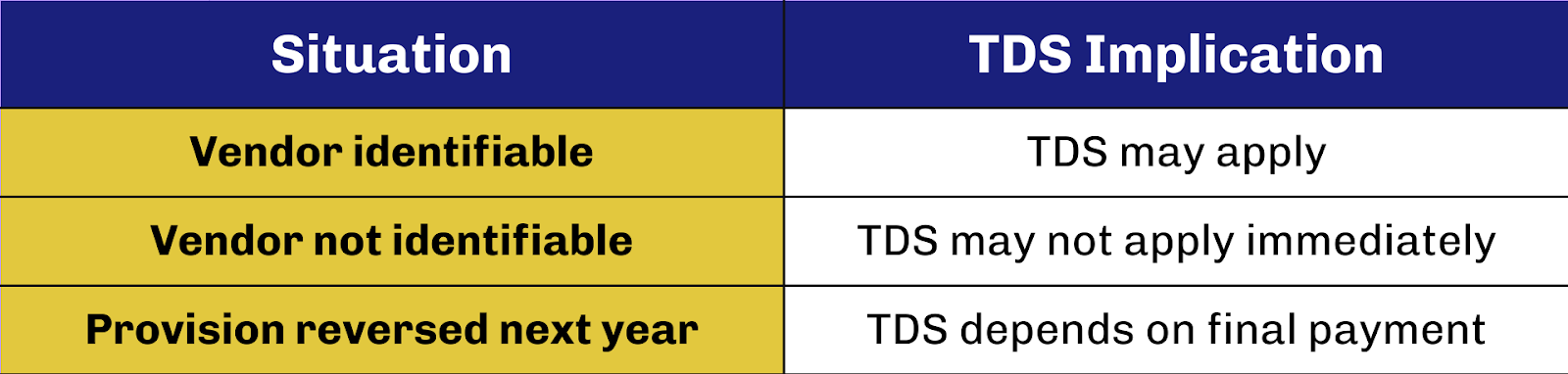

12. Is TDS required if the provision is reversed later?

If the provision was created for an identifiable vendor, TDS may still be required when the liability was first recorded, even if the provision is reversed later.

13. What is the difference between provision and payable for TDS?

A provision is an estimated expense recorded before an invoice is received, while a payable represents a confirmed liability. For TDS purposes, both may trigger deduction if the payee is identifiable.

14. Can TDS be deducted at the time of payment instead of provision?

If the provision does not identify the payee, TDS may be deducted later at payment. However, if the vendor is identifiable at the time of provisioning, TDS may be required immediately.

15. How can businesses ensure compliance with TDS on provisions?

Businesses should review year-end provisions, identify vendors, check Section 194J thresholds, deduct TDS where applicable, and maintain documentation for provisioning entries.

Contact Us

An expert will call you within 24 hours. No payment required to get started.

Related Post

How should a start-up complete ITR filing

Business entities must file their ITR annually to comply with the tax laws of their respective countries. It helps the government assess and collect the appropriate amount of income tax from taxpayers and ensures proper accountability of financial activities.

. 3 Mins.png)

5 step checklist for GST compliance in Indian Startups

Learn about how GST works. The basics of GST along with its compliances. Uncover what your business needs to keep in mind concerning GST rules and GST compliance.

. 3 min read.png)

₹20 Lakhs and Beyond: Understanding GST for Freelancers in India

Are you a freelancer or aspiring to be one? In this blog, uncover the basics of freelancing and requirements involving GST. Learn about all the exemptions, obligations, and compliances of GST for freelancers in india.

. 5 min read