Minimum Alternate Tax (MAT): Meaning, Applicability & Calculation Explained

What is Minimum Alternate Tax in India?

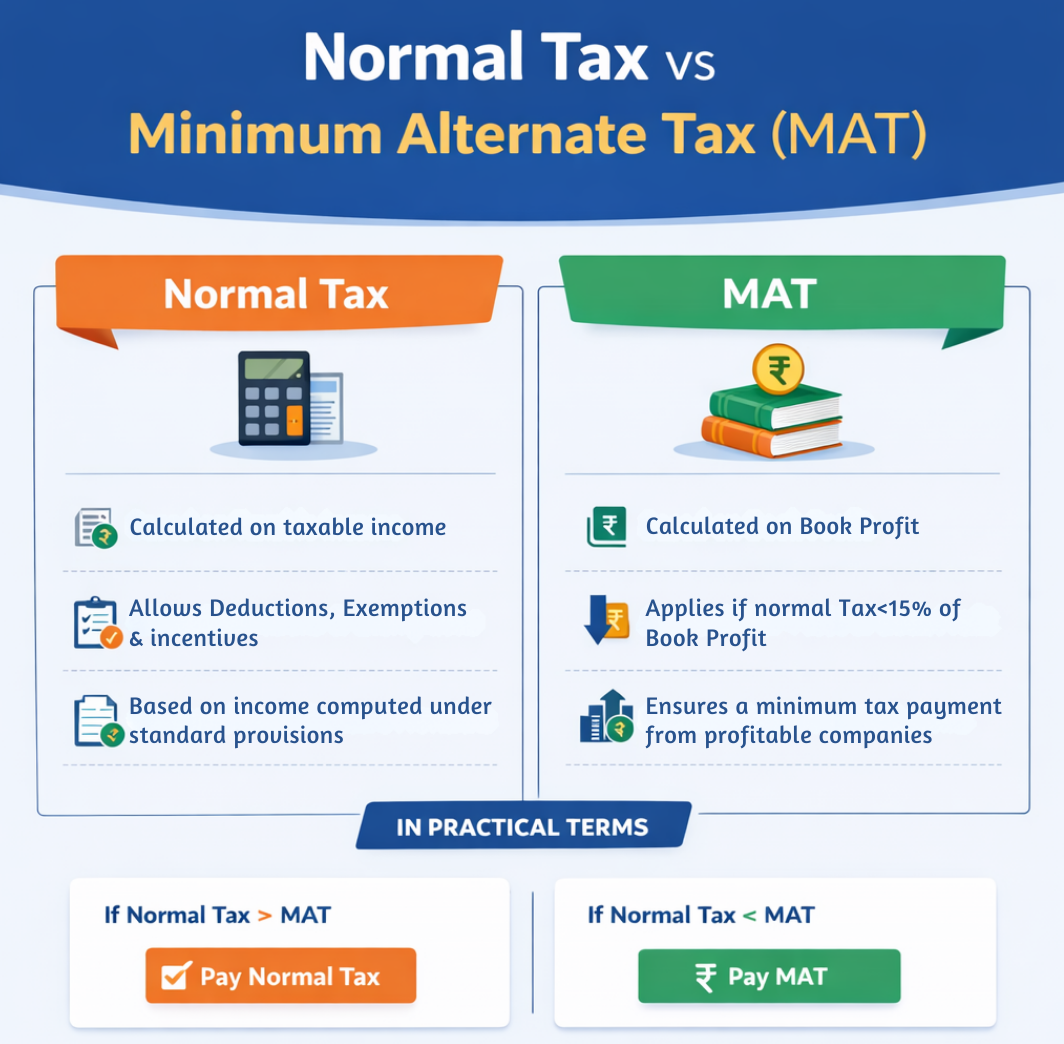

Minimum Alternate Tax (MAT) is a provision under Indian income tax law that ensures certain companies pay a minimum level of tax, even if deductions and exemptions significantly reduce their taxable income.

In simple terms, minimum alternate tax applies when the tax payable under normal income tax provisions is lower than a prescribed percentage of the company’s book profit. In such cases, the company must pay MAT instead of the lower normal tax amount.

Key points:

- MAT applies only to companies.

- It is calculated on book profit, not taxable income.

- It is triggered when normal tax liability falls below the MAT threshold.

- It ensures a minimum tax contribution from profitable companies.

If a company shows strong profits in its financial statements but pays very little income tax due to various deductions, MAT ensures that a baseline tax is still paid.

Purpose of Minimum Alternate Tax

The purpose of Minimum Alternate Tax is to maintain fairness and balance in corporate taxation.

Before MAT was introduced, several companies were legally reducing their taxable income to zero or near zero by claiming deductions, incentives, and exemptions under the Income Tax Act. While these claims were valid, it resulted in situations where profitable companies were not contributing proportionate tax revenue.

Minimum Alternate Tax was introduced to:

- Ensure profitable companies pay a minimum level of income tax

- Prevent excessive tax avoidance through deductions

- Safeguard government revenue

- Create parity between reported profits and tax liability

MAT does not remove deductions or incentives. It simply ensures that if those benefits reduce normal tax below a certain level, a minimum tax based on book profit is still payable.

Section 115JB of Income Tax Act Explained

Minimum Alternate Tax is governed by Section 115JB of Income Tax Act.

This section lays down the legal framework for:

- MAT applicability

- The prescribed MAT rate

- The method of computing book profit

- Adjustments required for MAT calculation

Under Section 115JB, if tax payable under normal provisions is less than 15% of book profit (plus surcharge and cess), the company must pay tax at 15% of book profit instead.

The concept of book profit is central to MAT. It refers to net profit shown in the Profit and Loss account prepared under the Companies Act, adjusted as specified under Section 115JB.

This framework ensures that corporate profitability and tax contribution remain aligned.

MAT Applicability: Who Needs to Pay?

Understanding MAT applicability is essential for companies claiming deductions, exemptions, or tax incentives.

Minimum Alternate Tax applies only to companies and becomes relevant when their normal tax liability falls below the MAT threshold prescribed under Section 115JB.

MAT applicability depends on:

- The legal status of the entity

- The comparison between normal tax and MAT

- Whether the company has opted for a concessional tax regime

It is not automatic for every company, it is triggered based on tax computation.

Companies Covered Under MAT

Minimum Alternate Tax applies primarily to:

- Domestic companies registered in India

- Certain foreign companies operating in India (subject to specific conditions)

MAT is relevant for companies that:

- Claim significant deductions or exemptions

- Report substantial book profit but low taxable income

- Fall under the standard corporate tax regime

Important:

MAT does not apply to individuals, Hindu Undivided Families (HUFs), partnerships, LLPs, or sole proprietorships. It applies strictly to companies as defined under the Companies Act.

When Does MAT Become Payable?

MAT becomes payable only after a comparison is made between:

- Tax calculated under normal income tax provisions

and - Tax calculated as a percentage of book profit under Section 115JB

If:

Normal Tax < MAT (15% of book profit + surcharge + cess)

Then:

The company must pay Minimum Alternate Tax.

If normal tax is higher than MAT, the company pays normal tax, and MAT does not apply for that year.

This comparison must be done every financial year before filing the income tax return.

Companies Exempt from MAT

Certain companies are not subject to MAT, depending on the tax regime they choose.

Companies that opt for specific concessional corporate tax regimes (such as those introduced under special sections of the Income Tax Act) are generally exempt from MAT provisions.

Additionally, certain categories of income governed by special taxation schemes may fall outside MAT applicability.

Before assuming exemption, companies must carefully evaluate:

- The tax regime opted for

- Eligibility conditions under that regime

- Whether Section 115JB applies

Incorrect assumptions regarding exemption can lead to underpayment of tax and compliance risks.

MAT Rate and How It Works

Minimum Alternate Tax is calculated at a prescribed percentage of a company’s book profit. It comes into play only when the tax payable under normal income tax provisions is lower than the MAT amount.

The mechanism is straightforward:

- Compute tax under normal income tax provisions.

- Compute MAT on book profit under Section 115JB.

- Compare both amounts.

- Pay the higher of the two.

MAT does not operate as an additional tax. It substitutes normal tax when the normal liability falls below the statutory minimum.

Current MAT Rate Structure

As per Section 115JB, the current minimum alternate tax rate is: 15% of book profit

Plus:

- Applicable surcharge

- 4% Health and Education Cess

This rate applies uniformly to companies covered under MAT provisions, unless they have opted for a concessional corporate tax regime where MAT does not apply.

The MAT rate remains fixed as a percentage of book profit. What changes each year is the comparison with the company’s normal tax liability.

Comparison Between Normal Tax and MAT

The key difference lies in the base used for calculation.

This comparison must be performed every year to determine the applicable tax liability.

How is Book Profit Calculated Under Section 115JB?

Under Section 115JB of the Income Tax Act, Minimum Alternate Tax is calculated on book profit rather than taxable income.

Book profit begins with net profit as per the Profit and Loss account prepared under the Companies Act. However, specific adjustments prescribed under Section 115JB must be made before arriving at the final figure.

The adjustments fall into two categories:

- Additions to net profit

- Deductions from net profit

Only adjustments explicitly listed in Section 115JB are permitted.

Additions to Net Profit

The following amounts are added back to the net profit (if they have been debited to the Profit and Loss account):

- Income tax paid or payable, and provisions for tax

- Provisions for unascertained liabilities

- Provisions for losses of subsidiary companies

- Deferred tax and related provisions

- Dividend proposed or paid

- Amounts set aside as reserves

These additions ensure that certain accounting entries do not artificially reduce the book profit for MAT purposes.

Deductions from Net Profit

The following amounts are reduced from net profit (if they have been credited to the Profit and Loss account):

- Income exempt under specified sections

- Depreciation (excluding revaluation adjustments, as prescribed)

- Brought forward loss or unabsorbed depreciation (as per books, whichever is lower)

- Amount withdrawn from reserves (subject to conditions)

These deductions prevent double taxation and align book profit adjustments with MAT provisions.

It is important to note that the adjustments are strictly limited to those specified in Section 115JB. Incorrect additions or deductions can lead to miscalculation of MAT liability.

Formula for Calculating Minimum Alternate Tax

Once the adjusted book profit is determined, the minimum alternate tax is calculated as follows:

MAT = 15% × Book Profit + surcharge + cess

For example:

Book Profit: ₹80,00,000

MAT @ 15% = ₹12,00,000

Cess @ 4% = ₹48,000

Total MAT Payable = ₹12,48,000

After arriving at this amount, it must be compared with tax computed under normal income tax provisions.

- If MAT exceeds normal tax → MAT becomes payable.

- If normal tax exceeds MAT → Normal tax is payable.

This comparison determines the final tax liability for the year.

Accurate computation of book profit is essential, because MAT is entirely dependent on that base figure. Even minor errors in adjustments can materially impact the outcome.

MAT Credit: Adjustment and Carry Forward

One of the most important features of minimum alternate tax is that excess tax paid under MAT is not permanently lost. The law allows companies to carry forward and adjust this excess through MAT credit.

MAT credit prevents long-term double taxation and supports tax neutrality across financial years.

What is MAT Credit?

MAT credit arises when the tax paid under MAT is higher than the tax payable under normal income tax provisions for a particular financial year.

In such a case:

- The company pays MAT for that year.

- The difference between MAT and normal tax becomes MAT credit.

- This credit can be carried forward for up to 15 assessment years.

Example:

Normal Tax: ₹10,00,000

MAT Liability: ₹14,00,000

Excess Paid: ₹4,00,000

This ₹4,00,000 becomes MAT credit.

MAT credit is not a refund. It is a future tax adjustment benefit.

How to Utilise MAT Credit

MAT credit can be adjusted in future years when normal tax liability exceeds MAT liability.

Adjustment is allowed only up to the difference between:

- Normal tax payable

- MAT payable for that year

For example:

Year 3:

Normal Tax: ₹20,00,000

MAT: ₹15,00,000

Difference: ₹5,00,000

The company can utilise MAT credit up to ₹5,00,000 (subject to available credit balance).

The credit can be carried forward for 15 assessment years and must be tracked accurately.

Failure to monitor MAT credit may result in lapse of benefit.

MAT credit acts as a long-term tax equaliser, ensuring that companies paying higher tax under MAT today can optimise tax liability in profitable future years.

Compliance Requirements and Penalties

Companies subject to minimum alternate tax must ensure accurate reporting and timely payment. Since MAT relies on book profit derived from financial statements, discrepancies are easily identifiable during assessment.

Errors in computation, non-disclosure, or delayed payment can trigger interest and penalties.

Reporting MAT in Income Tax Return

MAT liability must be correctly disclosed in the company’s Income Tax Return (ITR).

Key compliance requirements include:

- Compute tax under both normal provisions and MAT provisions.

- Report book profit as per Section 115JB in the designated ITR schedule.

- Obtain a Chartered Accountant’s certification in Form 29B, confirming the correct computation of book profit.

- Pay advance tax considering MAT liability, if applicable.

Form 29B is mandatory for companies liable under MAT. It certifies that the book profit has been computed according to Section 115JB requirements.

Failure to report MAT correctly can result in notices or reassessment proceedings.

Interest and Penalty Provisions

If MAT is not paid correctly or on time, the following consequences may apply:

- Interest under Section 234B for default in payment of advance tax.

- Interest under Section 234C for deferment of advance tax instalments.

- Penalty for under-reporting or misreporting income.

- Additional scrutiny during assessment proceedings.

Since MAT is calculated on book profit derived from financial statements, discrepancies between reported profits and tax filings are easily traceable.

Timely calculation, accurate reporting, and proper certification are essential to ensure smooth compliance under the Minimum Alternate Tax framework.

Common Mistakes and Practical Tips for Businesses

Minimum Alternate Tax often creates confusion because it operates alongside normal tax provisions. Even minor errors in book profit adjustments or tax comparisons can impact liability and MAT credit.

Avoiding these errors reduces compliance risk.

Common Errors in MAT Calculation

Many companies make mistakes not because the law is unclear, but because the comparison between normal tax and MAT is overlooked.

Common errors include:

- Ignoring MAT applicability while claiming large deductions.

- Incorrect computation of book profit under Section 115JB.

- Adding or deducting items not prescribed under MAT provisions.

- Failing to compare normal tax and MAT before filing returns.

- Not tracking MAT credit separately year-wise.

- Assuming concessional regimes automatically eliminate MAT without verifying eligibility.

Since MAT is linked directly to financial statements, inconsistencies between reported profits and tax filings can trigger scrutiny.

Practical Tips to Stay Compliant

To manage MAT effectively:

- Always compute tax under both normal provisions and MAT before finalising returns.

- Maintain a clear reconciliation between taxable income and book profit.

- Keep a dedicated schedule for tracking MAT credit carry forward.

- Review Section 115JB adjustments carefully each year.

- Factor MAT into advance tax calculations to avoid interest under Sections 234B and 234C.

- Seek professional review when opting for alternative tax regimes.

Minimum Alternate Tax is manageable when approached systematically. Accurate computation, consistent tracking, and timely reporting help businesses remain compliant while preserving long-term tax efficiency.

Conclusion

Minimum Alternate Tax ensures that profitable companies contribute a minimum level of tax even when deductions significantly reduce normal tax liability.

Governed by Section 115JB of the Income Tax Act, MAT is calculated on book profit and applies only when normal tax falls below the statutory threshold. Excess MAT paid becomes MAT credit, which can be carried forward and adjusted in future years.

With accurate computation, disciplined tracking, and proper reporting, MAT becomes a structured compliance requirement rather than an unexpected tax burden.

FAQ:

1. What is Minimum Alternate Tax (MAT)?

Minimum Alternate Tax is a provision that requires certain companies to pay at least 15% of their book profit as tax if their normal income tax liability is lower.

2. What is the purpose of MAT?

MAT ensures that profitable companies cannot reduce their tax liability to negligible levels using deductions and exemptions. It guarantees a minimum tax contribution.

3. Who is liable to pay MAT in India?

MAT applies to domestic companies and certain foreign companies operating in India when their normal tax liability is lower than 15% of book profit.

4. Under which section is MAT governed?

MAT is governed by Section 115JB of the Income Tax Act.

5. What is the current MAT rate?

The current MAT rate is 15% of book profit, plus applicable surcharge and 4% Health and Education Cess.

6. How is book profit calculated for MAT?

Book profit starts with net profit as per the Profit and Loss account and is adjusted by adding or deducting items specified under Section 115JB.

7. Does MAT apply to individuals or LLPs?

No. MAT applies only to companies. LLPs are governed by Alternate Minimum Tax (AMT) provisions, not MAT.

8. When does MAT become payable?

MAT becomes payable when tax calculated under normal income tax provisions is less than 15% of book profit.

9. What is MAT credit?

MAT credit is the excess tax paid when MAT exceeds normal tax liability. It can be carried forward and adjusted against future normal tax.

10. How long can MAT credit be carried forward?

MAT credit can be carried forward for up to 15 assessment years.

11. Is MAT credit refundable?

No. MAT credit is not refundable. It can only be adjusted against future tax liability.

12. Are companies under concessional tax regimes liable for MAT?

Generally, companies opting for specified concessional corporate tax regimes are exempt from MAT, subject to eligibility conditions.

13. Is advance tax applicable on MAT?

Yes. Companies must consider MAT liability while calculating and paying advance tax installments.

14. Is Form 29B mandatory for MAT?

Yes. Companies liable under MAT must obtain a Chartered Accountant’s certificate in Form 29B certifying book profit computation.

15. What happens if MAT is not paid on time?

Delay or short payment may attract interest under Sections 234B and 234C, along with possible penalties and scrutiny during assessment.

Why choose Us?

Filing Buddy is an entity which is focused at providing legal, financial, and corporate and compliances consultancy services to business entities. Our organisation is a structure made of enthusiastics.

EXPERTISE & RELIABILITY

Trusted industry professionals ensuring compliance, accurate tax filing, and comprehensive services for your business needs.

TAILORED SOLUTIONS

Customized services to meet your specific requirements, including business incorporation, trademarks, patents, and seamless GST return filing.

TIMELY SUPPORT

Dedicated support team committed to providing prompt assistance, resolving queries, and ensuring smooth operations for your business.

COMPETITIVE ADVANTAGE

Gain a competitive edge with our comprehensive suite of services, enabling you to focus on growth while we handle your compliance and taxation needs.

.webp)

.webp)

.webp)