India Tax Reforms 2026: Key Changes Guide

By Filing Buddy . 01 Apr 26

India’s Fiscal and Regulatory Overhaul for Tax Year 2026-27

The legislative landscape of India is undergoing a profound structural shift as the nation transitions from a multi-decade accretion of laws to a streamlined, digital-first regulatory framework. Effective from 1 April 2026, the replacement of the Income Tax Act of 1961 with the Income Tax Act of 2025 represents a landmark development aimed at enhancing transparency, equity, and economic efficiency. This report provides an exhaustive analysis of the five primary compliance changes active as of 1 April 2026, encompassing direct taxation, indirect taxation, and corporate governance. By synthesizing research data with practical implications, the analysis illustrates how these reforms impact salaried individuals, small business owners, and corporate directors in plain language.

The Structural Evolution of Direct Taxation: The Income Tax Act 2025

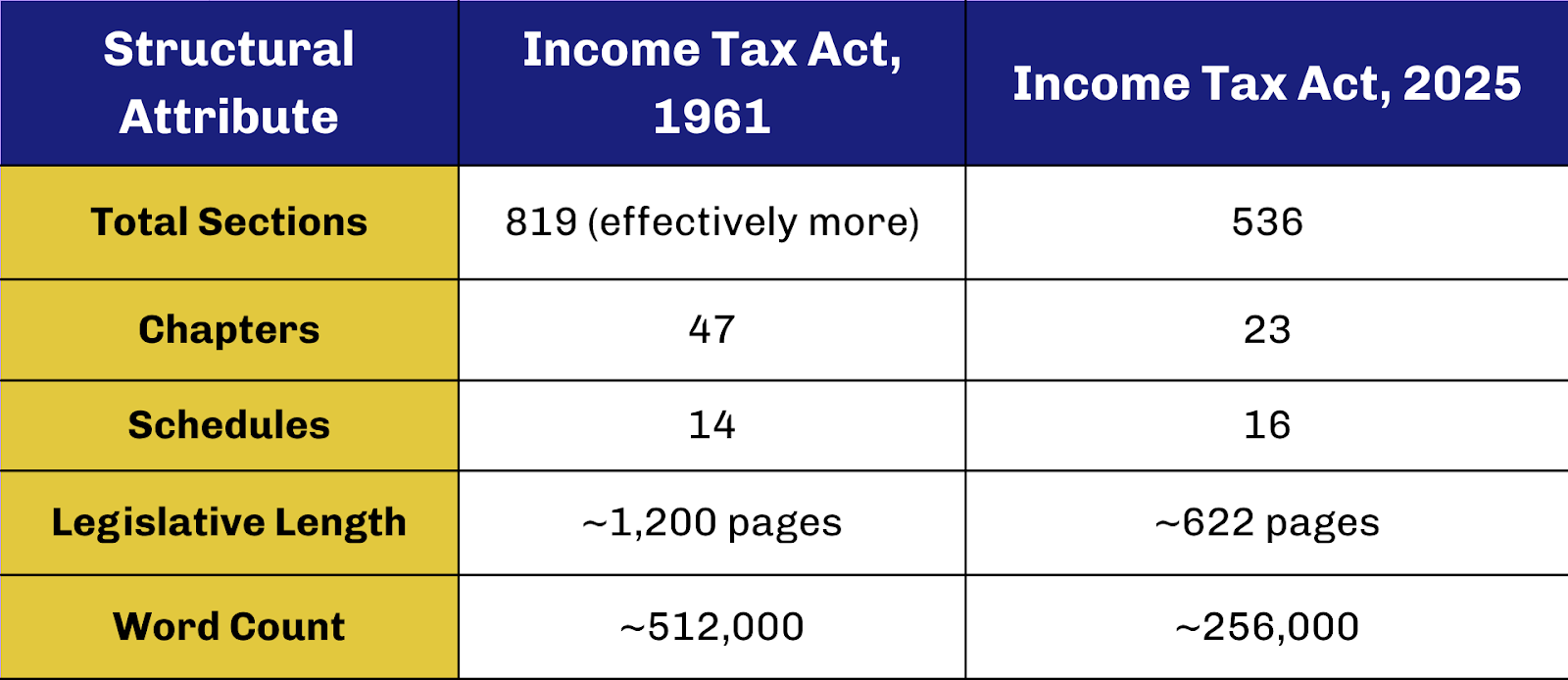

The transition from the Income Tax Act of 1961 to the Income Tax Act of 2025 is not merely an administrative update but a complete "reprogramming" of India's direct tax architecture. For over sixty years, the 1961 Act functioned as a complex map that had been modified nearly 65 times through various Finance Acts, leading to over 4,000 individual amendments. This accumulation resulted in a fragmented statute characterized by dense language, excessive cross-referencing, and redundant provisions that often hindered voluntary compliance.

The new legislation seeks to modernize the system by reducing the word count from approximately 5.12 lakh words to roughly 2.56 lakh words, effectively halving the legislative bulk. The section count has been streamlined from 819 to 536, and the structure has been reorganized into 23 chapters and 16 schedules. This reorganization prioritizes intuitive navigation, where provisions are grouped by heads of income rather than scattered functions.

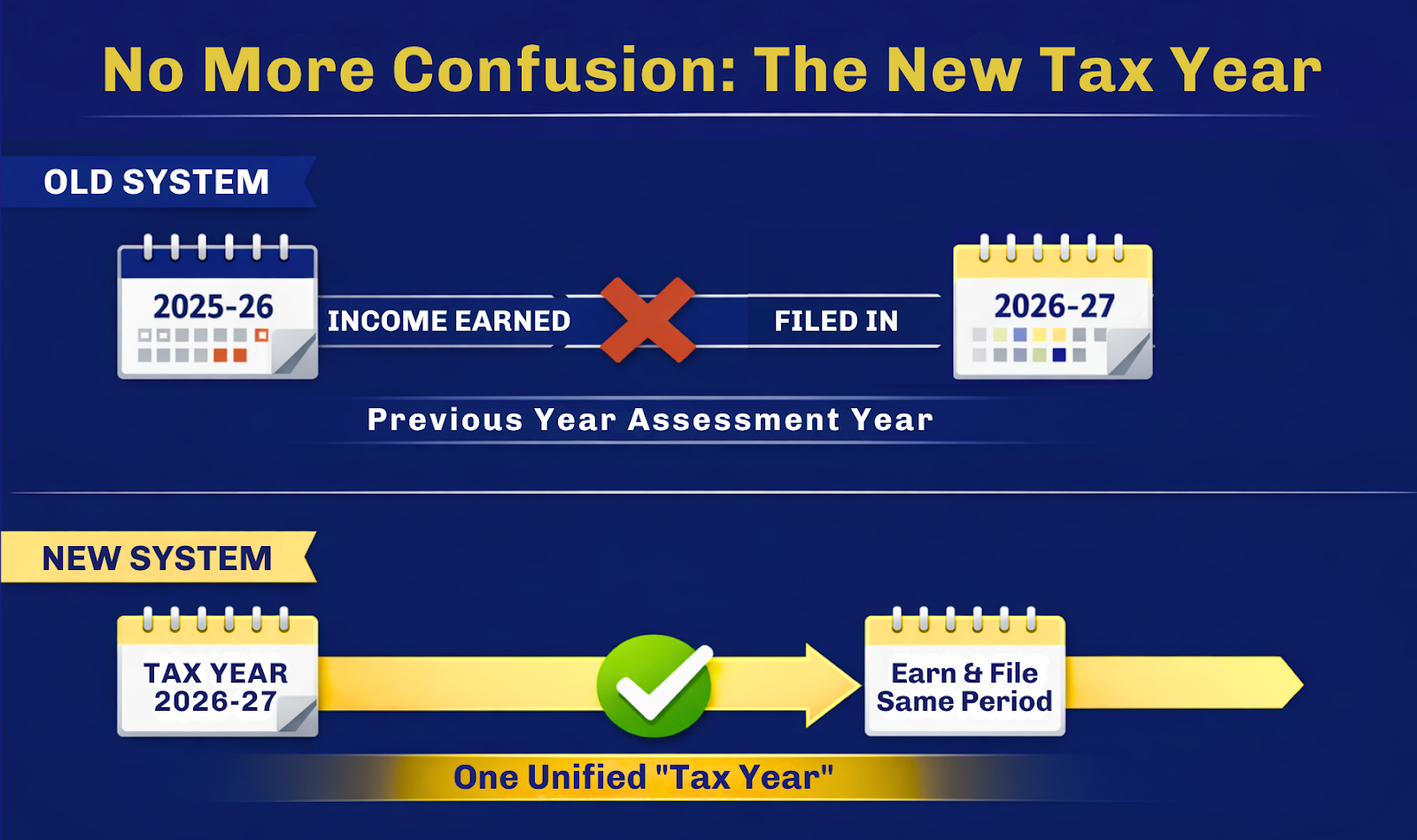

Transition to the Single Tax Year Concept

A cornerstone of the 2025 Act is the elimination of the dual-concept terminology involving the "Previous Year" and the "Assessment Year". Under the 1961 framework, the "Previous Year" referred to the financial year in which income was earned, while the "Assessment Year" was the subsequent year in which that income was evaluated for tax purposes. This distinction frequently caused confusion for lay taxpayers when filing returns or responding to legal notices.

The Income Tax Act, 2025 introduces the "Tax Year" concept, a single 12-month period running from 1 April to 31 March. This alignment ensures that the period for earning income is identical to the period for its reporting and taxation. For a taxpayer like an individual employee, filing for the "Tax Year 2026-27" now refers clearly to the income earned during that specific period, removing the cognitive hurdle of shifting to a future assessment year.

Simplification of Language and Removal of Redundancies

The redrafting process was anchored in the principle of textual simplification. Archaic legal jargon and complex conditional phrases, such as "notwithstanding anything contained," have been replaced with more direct language like "irrespective of anything contained". Furthermore, the Act has explicitly removed approximately 1,200 provisos and 900 explanations that previously added layers of exceptions to the core law.

To further aid clarity, the legislation incorporates 57 illustrative tables and various formulae to explain complex concepts such as salary perquisites, presumptive taxation, and TDS rates. This shift toward a "Trust First" approach is designed to foster a culture of voluntary compliance by making the law accessible to the average citizen rather than being the exclusive domain of tax professionals.

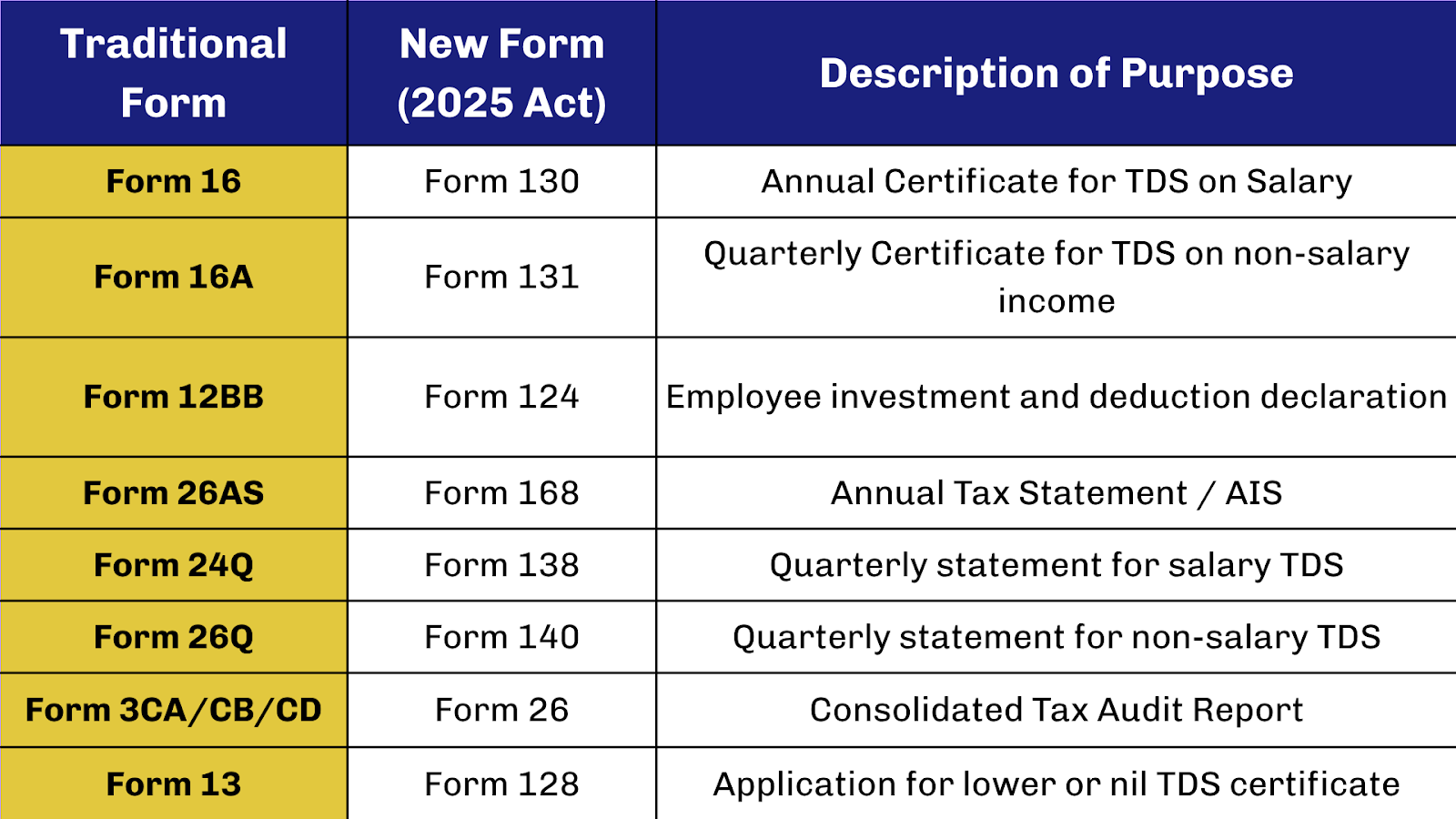

The New Compliance Form Ecosystem

The implementation of the Income Tax Act, 2025 necessitates a comprehensive renumbering of familiar compliance forms to match the new statutory sequence. While the core purpose of most forms remains intact, the numbering change requires significant updates across corporate payroll systems, tax software, and banking interfaces.

Mapping the Form Transition

The transition involves renumbering nearly 200 forms. For example, the TDS certificate for salary, formerly Form 16, is now issued as Form 130. This update is critical for employers who must revise their internal document templates and employee communication workflows for the fiscal year 2026-27.

Strategic Consolidation of Audit and Reporting

The new framework emphasizes consolidation to reduce procedural duplication. A primary example is the merging of the traditional tax audit forms (3CA, 3CB, and 3CD) into a single, unified Form 26. While the new form is comprehensive, expanding from 44 to 55 segment-wise clauses it provides a more cohesive data set for the tax authorities.

Furthermore, the Annual Tax Statement (now Form 168) has been refined to reflect a PAN-based identification system, removing Aadhaar numbers from the document to enhance privacy. For taxpayers, this form remains the central point of verification for bank interest, dividends, and capital gains, which are increasingly pre-filled in the return filing portal.

Relief for the Salaried Workforce: Allowances and Housing Benefits

Under the Income Tax Rules, 2026, the government has addressed several long-standing grievances regarding the stagnation of tax-free allowance limits. These updates acknowledge the impact of inflation over the decades and provide meaningful relief to salaried families.

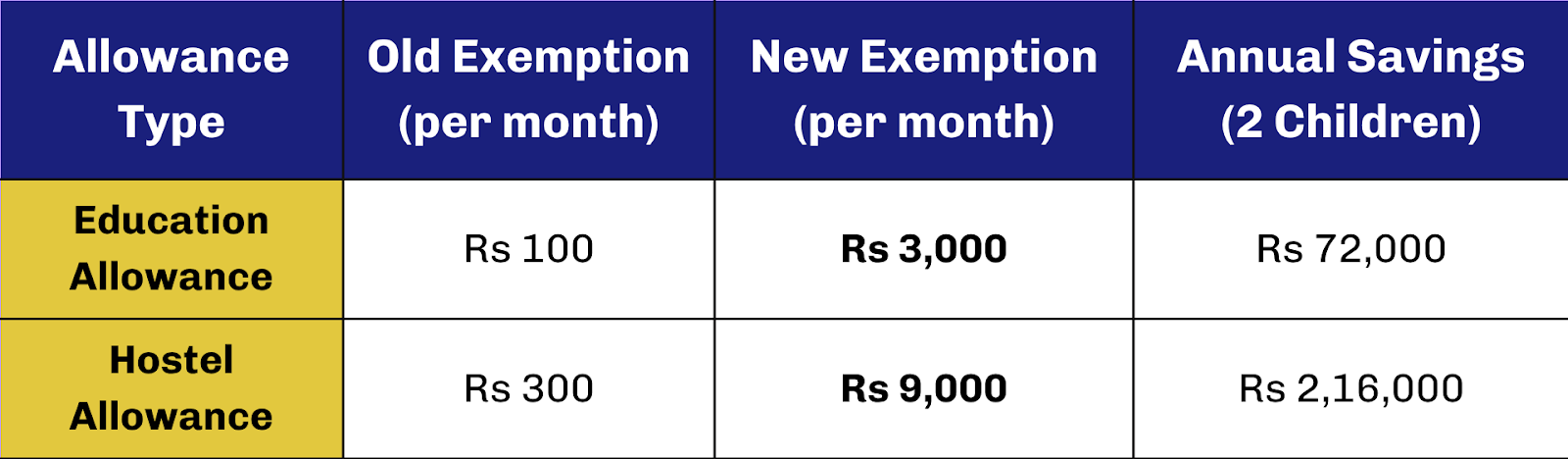

Radical Increases in Education and Hostel Exemptions

The exemption limits for children's education and hostel allowances had remained unchanged for decades at nominal levels of Rs 100 and Rs 300 per month respectively. These limits were widely considered archaic and did not reflect the actual costs of schooling in modern India.

Effective 1 April 2026, the Children's Education Allowance exemption has been increased 30-fold to Rs 3,000 per month per child. Similarly, the Hostel Expenditure Allowance has been raised to Rs 9,000 per month per child. These exemptions are available for up to two children and are claimed under the Old Tax Regime.

Expansion of Metro Category for HRA Benefits

The House Rent Allowance (HRA) framework has been modernized to include a broader list of cities eligible for the higher 50% basic salary exemption. Previously, only Mumbai, Delhi, Kolkata, and Chennai qualified for this higher tier, while all other urban centers were capped at 40%.

Reflecting the rapid urbanization of the technology and industrial sectors, four additional cities have been added to the 50% exemption list:

- Bengaluru

- Pune

- Hyderabad

- Ahmedabad

This expansion allows millions of employees in these cities to claim higher HRA deductions, provided they opt for the Old Tax Regime. The HRA exemption is calculated as the minimum of three values:

- Actual HRA received.

- Rent paid minus 10% of salary.

- 50% (for 8 specified cities) or 40% (for others) of salary.

Enhanced Transparency in Rental Claims

While the benefits have increased, so has the requirement for transparency. Under the new Form 124 (formerly 12BB), employees are now mandatory required to disclose their "relationship with the landlord". This measure is designed to curb the practice of claiming HRA through fabricated rent receipts to close relatives without actual movement of funds. If the total annual rent exceeds Rs 1 lakh, providing the landlord’s PAN remains a mandatory requirement for cross-verification.

Indirect Tax Reforms: Optimizing Liquidity and Export Competitiveness

The 2026-27 transition brings critical relief to businesses operating under the Goods and Services Tax (GST) regime, specifically addressing "Inverted Duty Structures" and small-scale export barriers.

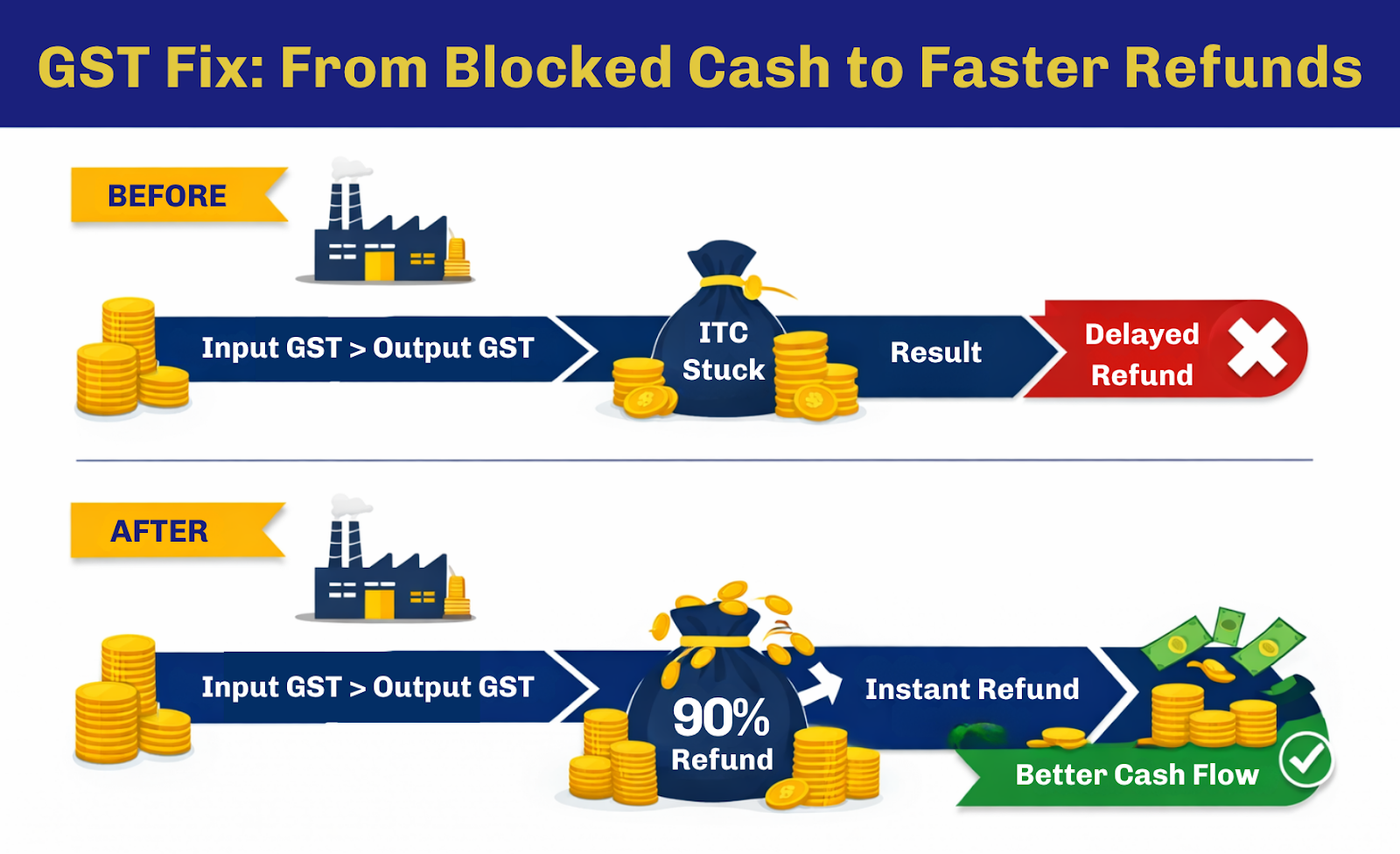

Provisional Refunds for Inverted Duty Structure (IDS)

An Inverted Duty Structure (IDS) occurs when the GST rate on raw materials (inputs) is higher than the rate on the finished product (outputs). This leads to a persistent accumulation of Input Tax Credit (ITC) that cannot be fully utilized against output tax liability, effectively blocking the working capital of the business. Industries such as textiles, footwear, and consumer goods are heavily impacted by this structure.

Prior to 1 April 2026, businesses with IDS were not eligible for "provisional refunds" (upfront release of 90% of the claim amount), a benefit reserved only for zero-rated exports. The amendment to Section 54(6) of the CGST Act now extends the provisional refund mechanism to IDS cases. This enables manufacturers to receive 90% of their refund claim provisionally while final verification is completed, providing immediate liquidity for reinvestment.

Removal of Minimum Threshold for Export Refunds

Previously, Section 54(14) of the CGST Act restricted the payment of any GST refund if the amount claimed was less than Rs 1,000 per tax head. This created a "liquidity pain" for small and micro-exporters, particularly those shipping low-value consignments via courier or postal modes, as their legitimate tax refunds remained stuck in the system indefinitely.

Effective 1 April 2026, the Rs 1,000 threshold has been removed for export refunds made with the payment of tax (IGST). This amendment ensures that every rupee of tax paid on exported goods is eligible for refund, making small Indian businesses more competitive in the global market. However, businesses must remember to file a fresh Letter of Undertaking (LUT) for FY 2026-27 on the GST portal, as the previous year's LUT expired on 31 March.

Corporate Amnesty: The Companies Compliance Facilitation Scheme (CCFS) 2026

To improve the accuracy of the Ministry of Corporate Affairs (MCA) registry, the government has introduced the CCFS 2026, a one-time opportunity for defaulting companies to regularize their standing.

The Mechanism of Relief and Additional Fee Waiver

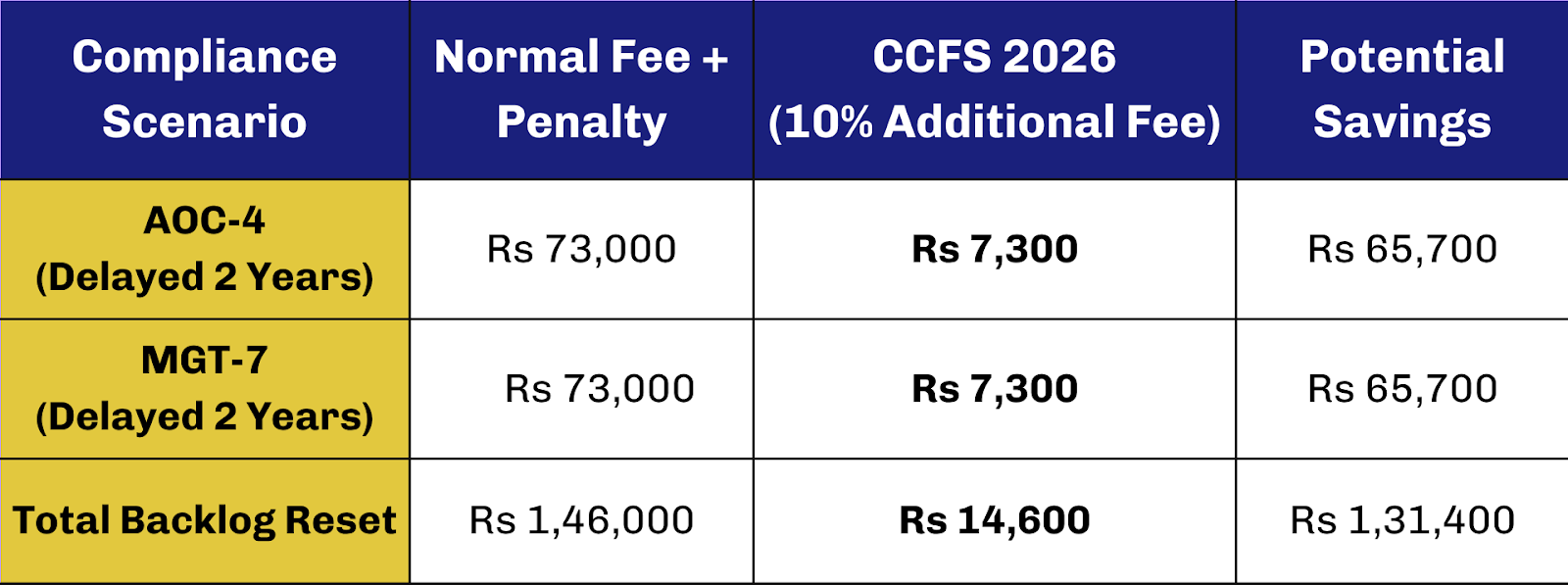

Under normal provisions of the Companies Act, 2013, a delay in filing annual returns (MGT-7) or financial statements (AOC-4) attracts an additional fee of Rs 100 per day per form with no upper limit. For small companies with several years of backlog, these fees often accumulate to lakhs of rupees, making the cost of compliance higher than the value of the company itself.

The CCFS 2026 provides a 90% discount on these additional fees. Eligible companies need only pay the normal filing fee plus 10% of the applicable additional fee.

Facilitating Exit and Dormancy

For promoters who no longer wish to operate their businesses, the scheme offers a concessional exit route. Filing Form STK-2 for "Strike-Off" (removal of company name) is available at only 25% of the standard fee (Rs 2,500 instead of Rs 10,000). Alternatively, companies that are temporarily inactive but wish to retain their corporate status can apply for "Dormant Status" via Form MSC-1 at only 50% of the normal filing fee.

Immunity Provisions

The real value of CCFS 2026 lies in its immunity benefits. If filings are completed within the three-month window (15 April to 15 July 2026), the company and its directors receive immunity from penal proceedings related to the specific delays. This is particularly relevant for restoring director eligibility, as chronic non-filing can lead to disqualification under Section 164(2).

Operational Updates: Deadlines and Digital Integration

The transition also encompasses changes to filing timelines and the formal recognition of digital payment modes within the tax framework.

Extended Deadlines for Small Businesses

In a move to stagger the compliance workload, the ITR filing deadline for non-audit business cases (ITR-3 and ITR-4) has been extended to 31 August from the previous 31 July. This gives small business owners and freelancers an extra month to reconcile their books and GST returns before filing their final income tax documents.

Digital Currency and Virtual Digital Assets (VDA)

The Income Tax Act, 2025 formally recognizes the Digital Rupee (e-Rupee) as a valid electronic payment mode. Simultaneously, the definition of Virtual Digital Assets (VDA) has been broadened to clearly include cryptocurrencies and tokenized assets, ensuring they are subject to clear reporting and tax rules.

The new law also expands the powers of tax authorities in the digital sphere. During search and seizure operations, officials are now authorized to access "Virtual Digital Space," which includes social media accounts, cloud storage, and email servers relevant to an investigation.

FAQs

1. What exactly is the "Tax Year" concept?

Think of it as "what you see is what you get." Previously, you earned money in a "Previous Year" and filed it in an "Assessment Year," which was confusing. Now, Tax Year 2026-27 simply means the period from 1 April 2026 to 31 March 2027. You earn, report, and pay for that specific window without switching labels.

2. My employer is asking for "Form 124" instead of "Form 12BB." Is this a mistake?

No, it’s correct! Under the new Income Tax Act 2025, many forms have been renumbered to stay organized. Form 124 is the new version of Form 12BB, where you declare your investments and rent details to your HR department.

3. I live in Bengaluru. How does the "Metro City" change affect my take-home pay?

This is great news for your wallet. Previously, Bengaluru was a "Non-Metro" for tax purposes, meaning only 40% of your basic salary was considered for HRA exemption. Now, it’s been upgraded to the 50% category (along with Pune, Hyderabad, and Ahmedabad), which could significantly lower your taxable income if you pay high rent.

4. How much tax can I save with the new Education and Hostel allowances?

The jump is huge. If you have two children in a hostel, the old exemption was a tiny Rs 9,600 per year. Under the new rules, you can claim up to Rs 2,88,000 annually (Rs 3,000/month for education and Rs 9,000/month for hostel per child).

Note: These benefits are only available if you choose the Old Tax Regime.

5. Why do I have to disclose my relationship with my landlord now?

The tax department wants to ensure that rent claims are genuine. If you are renting from a parent or relative, you must disclose it on Form 124. This doesn't mean it’s illegal, but you must ensure actual money is being transferred and your relative is reporting that rent as income.

6. I lost my old Form 16. What should I look for now?

The annual TDS certificate for salary, which used to be Form 16, is now Form 130. If you're looking for your overall tax summary (the old Form 26AS/AIS), look for Form 168.

7. I run a small startup with an "Inverted Duty Structure." How does the new GST rule help me?

If you pay 18% GST on raw materials but sell your product at 12%, your cash gets "stuck" with the government. Previously, you had to wait months for a full audit to get a refund. Now, you can get 90% of that refund almost immediately (provisional refund), which keeps your cash flow healthy.

8. My company hasn't filed annual returns for two years. What is the CCFS 2026?

It’s a "pardon" period. Usually, you’d pay a penalty of Rs 100 per day, which adds up to thousands. Under the Companies Compliance Facilitation Scheme (CCFS) 2026, you get a 90% discount on those late fees if you file between 15 April and 15 July 2026. It's a "reset button" for your company's legal standing.

9. Has the deadline for filing my personal income tax return changed?

If you are a salaried individual, the deadline usually remains 31 July. However, if you are a freelancer or a small business owner (who doesn't require a formal audit), the deadline has been extended to 31 August. This gives you an extra month to get your books in order.

10. Can I pay my taxes using the "Digital Rupee" (e-Rupee)?

Yes. The 2025 Act formally recognizes the e-Rupee as a valid payment mode. It’s treated just like cash or a bank transfer, making the process fully compatible with India's new digital currency.

Contact Us

An expert will call you within 24 hours. No payment required to get started.

Related Post

How should a start-up complete ITR filing

Business entities must file their ITR annually to comply with the tax laws of their respective countries. It helps the government assess and collect the appropriate amount of income tax from taxpayers and ensures proper accountability of financial activities.

. 3 Mins.png)

5 step checklist for GST compliance in Indian Startups

Learn about how GST works. The basics of GST along with its compliances. Uncover what your business needs to keep in mind concerning GST rules and GST compliance.

. 3 min read.png)

₹20 Lakhs and Beyond: Understanding GST for Freelancers in India

Are you a freelancer or aspiring to be one? In this blog, uncover the basics of freelancing and requirements involving GST. Learn about all the exemptions, obligations, and compliances of GST for freelancers in india.

. 5 min read